G رجحان EMA ATR ذہین تجارتی حکمت عملی

خلاصہ

یہ حکمت عملی G چینل انڈیکیٹر کا استعمال کرتے ہوئے مارکیٹ کے رجحان کی سمت کی نشاندہی کرتی ہے، اور ساتھ ہی EMA اور ATR انڈیکیٹرز کو بہتر داخلے اور خارج ہونے کے مقامات کے لیے استعمال کرتی ہے۔ حکمت عملی کا بنیادی خیال یہ ہے: جب قیمت G چینل کے اوپری بینڈ کو توڑتی ہے اور EMA سے نیچے ہو تو لانگ میں جائیں، اور جب G چینل کے نچلے بینڈ کو توڑتی ہے اور EMA سے اوپر ہو تو شارٹ میں جائیں۔ ساتھ ہی، ATR کا استعمال کرتے ہوئے متحرک اسٹاپ لاس اور ٹیک پرافٹ مقرر کیے جاتے ہیں، اسٹاپ لاس 2 گنا ATR اور ٹیک پرافٹ 4 گنا ATR ہوتا ہے۔ اس طریقے سے رجحانی مارکیٹ میں زیادہ منافع حاصل کیا جا سکتا ہے جبکہ خطرے پر سخت کنٹرول رکھا جا سکتا ہے۔

حکمت عملی کا اصول

- G چینل کے اوپری اور نچلے بینڈ کا حساب: موجودہ بند قیمت اور پچھلی زیادہ سے زیادہ/کم سے کم قیمت کا استعمال کرتے ہوئے G چینل کے اوپری اور نچلے بینڈ کا حساب لگایا جاتا ہے۔

- رجحان کی سمت کا تعین: قیمت اور G چینل کے بینڈ کے تعلق کو دیکھ کر تیزی یا مندی کے رجحان کا تعین کیا جاتا ہے۔

- EMA کا حساب: مخصوص مدت کے لیے EMA قدر کا حساب لگایا جاتا ہے۔

- ATR کا حساب: مخصوص مدت کے لیے ATR قدر کا حساب لگایا جاتا ہے۔

- خرید و فروخت کی شرائط کا تعین: جب قیمت G چینل کے اوپری بینڈ کو توڑتی ہے اور EMA سے نیچے ہو تو لانگ ٹرگر ہوتا ہے، اور جب نچلے بینڈ کو توڑتی ہے اور EMA سے اوپر ہو تو شارٹ ٹرگر ہوتا ہے۔

- اسٹاپ لاس اور ٹیک پرافٹ کا تعین: اسٹاپ لاس = کھلنے کی قیمت - 2 × ATR، ٹیک پرافٹ = کھلنے کی قیمت + 4 × ATR (لانگ کے لیے)؛ اسٹاپ لاس = کھلنے کی قیمت + 2 × ATR، ٹیک پرافٹ = کھلنے کی قیمت - 4 × ATR (شارٹ کے لیے)۔

- حکمت عملی کا ایکٹیویشن: جب خرید و فروخت کی شرائط پوری ہوں تو متعلقہ پوزیشن کھولی جاتی ہے اور اس کے مطابق اسٹاپ لاس اور ٹیک پرافٹ سیٹ کیے جاتے ہیں۔

حکمت عملی کے فوائد

- رجحان کی پیروی: حکمت عملی G چینل کا استعمال کرتے ہوئے مارکیٹ کے رجحان کو مؤثر طریقے سے پکڑتی ہے، جو رجحانی حالات کے لیے موزوں ہے۔

- متحرک اسٹاپ لاس اور ٹیک پرافٹ: ATR کا استعمال کرتے ہوئے اسٹاپ لاس اور ٹیک پرافٹ کو متحرک طور پر ایڈجسٹ کیا جاتا ہے، جو مارکیٹ کے اتار چڑھاؤ کو بہتر طور پر اپنانے میں مدد دیتا ہے۔

- رسک کنٹرول: اسٹاپ لاس کو 2 گنا ATR پر مقرر کر کے ہر تجارت کے خطرے کو سختی سے کنٹرول کیا جاتا ہے۔

- سادہ اور آسان: حکمت عملی کی منطق واضح اور سادہ ہے، زیادہ تر سرمایہ کاروں کے استعمال کے لیے موزوں ہے۔

حکمت عملی کے خطرات

- اتار چڑھاؤ والی مارکیٹ: اتار چڑھاؤ والی مارکیٹ میں بار بار تجارتی سگنلز نقصان کو بڑھا سکتے ہیں۔

- پیرامیٹر کی اصلاح: مختلف مصنوعات اور ادوار کے لیے مختلف پیرامیٹرز کی ضرورت ہو سکتی ہے، اندھا دھند استعمال خطرے کا سبب بن سکتا ہے۔

- بلیک سوان واقعات: انتہائی حالات میں قیمت میں شدید اتار چڑھاؤ آ سکتا ہے، جس کی وجہ سے اسٹاپ لاس مؤثر طریقے سے کام نہیں کر سکتا۔

حکمت عملی کی اصلاح کی سمت

- رجحان کی فلٹرنگ: رجحان کی فلٹرنگ کی شرائط شامل کریں، جیسے MA کراس اوور، DMI وغیرہ، تاکہ اتار چڑھاؤ والی مارکیٹ میں تجارت کم ہو سکے۔

- پیرامیٹر کی اصلاح: مختلف مصنوعات اور ادوار کے لیے پیرامیٹر کی اصلاح کریں تاکہ بہترین پیرامیٹر کا امتزاج مل سکے۔

- پوزیشن کا انتظام: مارکیٹ کے اتار چڑھاؤ کے مطابق پوزیشن کے سائز کو متحرک طور پر ایڈجسٹ کریں تاکہ سرمائے کے استعمال میں بہتری آئے۔

- مجموعہ حکمت عملی: اس حکمت عملی کو دیگر مؤثر حکمت عملیوں کے ساتھ ملا کر استحکام بڑھایا جائے۔

خلاصہ

یہ حکمت عملی G چینل، EMA، ATR جیسے انڈیکیٹرز کا استعمال کرتے ہوئے ایک سادہ اور مؤثر رجحان کی پیروی کرنے والا تجارتی نظام تشکیل دیتی ہے۔ رجحانی مارکیٹ میں یہ اچھے نتائج دے سکتی ہے، لیکن اتار چڑھاؤ والی مارکیٹ میں اس کی کارکردگی معمولی ہوتی ہے۔ آگے چل کر رجحان کی فلٹرنگ، پیرامیٹر کی اصلاح، پوزیشن مینجمنٹ، اور مجموعہ حکمت عملی جیسے شعبوں میں حکمت عملی کو بہتر بنایا جا سکتا ہے، تاکہ حکمت عملی کی مضبوطی اور منافع بخشی میں مزید اضافہ ہو سکے۔

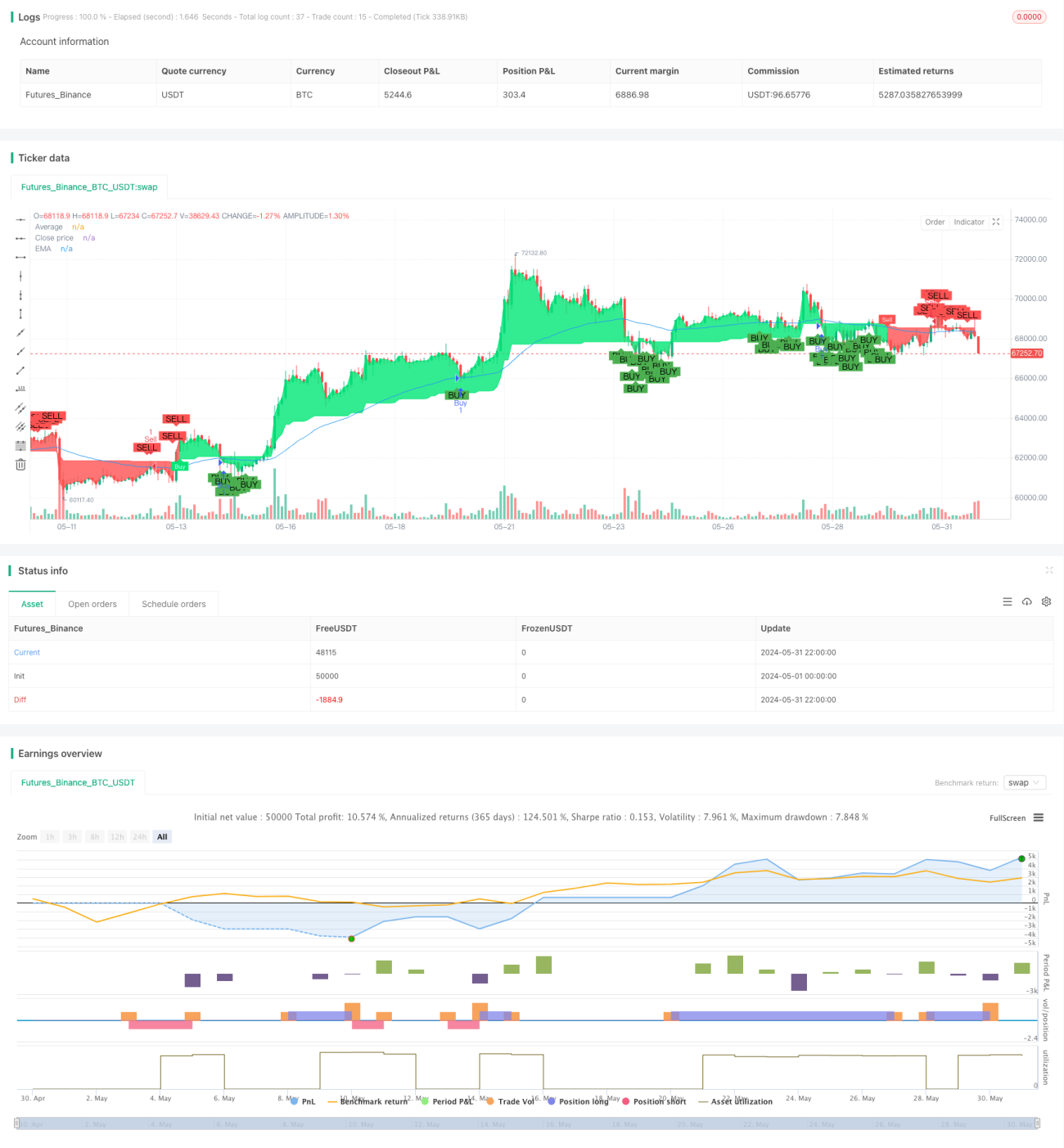

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Full credit to AlexGrover: https://www.tradingview.com/script/fIvlS64B-G-Channels-Efficient-Calculation-Of-Upper-Lower-Extremities/

strategy ("G-Channel Trend Detection with EMA Strategy and ATR", shorttitle="G-Trend EMA ATR Strategy", overlay=true)

- 1