ملٹی لیول ڈائنامک ٹرینڈ فالونگ سسٹم

جائزہ

ایک کثیر سطحی متحرک رجحان کی پیروی کا نظام ایک بہتر حکمت عملی ہے جو ساحل سمندر کے ٹریڈنگ قوانین پر مبنی ہے۔ یہ حکمت عملی درمیانی اور طویل مدتی رجحان پر قابو پانے کے لئے متعدد وقت کے دوروں کے رجحان کے اشارے کا استعمال کرتی ہے ، متحرک اسٹاپ نقصان اور پائیرمڈ بیعانہ کو جوڑتی ہے۔ نظام دو رجحانات کی پیروی کرنے والے دوروں (L1 اور L2) کو ترتیب دے کر مختلف رفتار کے رجحانات کو پکڑتا ہے ، اور متحرک طور پر داخلے ، بیعانہ اور اسٹاپ نقصان کی پوزیشن کو ایڈجسٹ کرنے کے لئے خود بخود اے ٹی آر اشارے کا استعمال کرتا ہے۔ اس کثیر سطحی ڈیزائن کی حکمت عملی سے مارکیٹ کے مختلف حالات میں استحکام برقرار رکھنے کے قابل ہوتا ہے ، جبکہ پائیرمڈ بیعانہ کے ذریعہ منافع کی صلاحیت کو زیادہ سے زیادہ بنایا جاسکتا ہے۔

حکمت عملی کا اصول

-

رجحانات کی شناخت: مختلف رفتار کے رجحانات کی شناخت کے لئے دو متحرک اوسط دوروں ((L1 اور L2) کا استعمال کریں۔ L1 تیز رفتار رجحانات کو پکڑنے کے لئے استعمال کیا جاتا ہے ، L2 آہستہ آہستہ لیکن زیادہ قابل اعتماد رجحانات کو پکڑنے کے لئے استعمال کیا جاتا ہے۔

-

انٹری سگنل: جب قیمت L1 یا L2 کی اونچائی کو توڑتی ہے تو ایک سے زیادہ سگنل پیدا ہوتا ہے۔ اگر پچھلا L1 تجارت منافع بخش ہے تو ، اگلے L1 سگنل کو اس وقت تک چھوڑ دیں جب تک کہ L2 سگنل نہ ہو۔

-

متحرک رکاوٹ: اے ٹی آر کے ضرب ((ڈیفالٹ 3 گنا) کو ابتدائی رکاوٹ فاصلے کے طور پر استعمال کریں ، جس میں پوزیشن کے وقت میں اضافے کے ساتھ رکاوٹ کی پوزیشن آہستہ آہستہ بڑھ جاتی ہے۔

-

پیراڈائزنگ: رجحان کے تسلسل کے دوران ، ہر بار جب قیمت میں 0.5 اے ٹی آر اضافہ ہوتا ہے تو ، زیادہ سے زیادہ 5 بار بڑھایا جاتا ہے۔

-

خطرے پر قابو پانا: ہر تجارت کا خطرہ اکاؤنٹ کی خالص مالیت کا 2٪ سے زیادہ نہیں ہے ، جس کا اندازہ متحرک طور پر حساب کتاب کے ذریعہ کیا جاتا ہے۔

-

باہر نکلنے کا طریقہ کار: جب قیمت 10 ویں دن کی کم سے کم ((L1) یا 20 ویں دن کی کم سے کم ((L2) سے نیچے آجائے ، یا جب متحرک اسٹاپ لائن کو متحرک کیا جائے۔

اسٹریٹجک فوائد

-

کثیر سطحی رجحانات کی گرفتاری: L1 اور L2 کے دو دوروں کے ذریعے ، فوری رجحانات کو پکڑنے کے ساتھ ساتھ طویل مدتی رجحانات کو بھی پکڑنے کے قابل ، حکمت عملی کی موافقت اور استحکام کو بہتر بناتا ہے۔

-

متحرک رسک مینجمنٹ: اے ٹی آر کو ایک اتار چڑھاؤ کے اشارے کے طور پر استعمال کرتے ہوئے ، مارکیٹ میں تبدیلیوں کو بہتر طور پر اپنانے کے لئے داخلے ، اسٹاپ نقصان اور پوزیشن میں اضافے کی پوزیشنوں میں متحرک ایڈجسٹمنٹ کا احساس ہوتا ہے۔

-

پیراڈائزنگ: جب رجحان جاری رہتا ہے تو اس میں اضافہ ہوتا ہے ، جس سے خطرے پر قابو پایا جاتا ہے اور منافع کی صلاحیت کو زیادہ سے زیادہ کیا جاتا ہے۔

-

لچکدار پیرامیٹرز کی ترتیب: ایک سے زیادہ ایڈجسٹ پیرامیٹرز حکمت عملی کو مختلف مارکیٹوں اور ٹریڈنگ شیلیوں کو اپنانے کے قابل بناتے ہیں۔

-

خودکار عملدرآمد: حکمت عملی کو مکمل طور پر خود کار طریقے سے چلایا جاسکتا ہے ، جس میں انسانی مداخلت اور جذباتی اثرات کو کم کیا جاسکتا ہے۔

اسٹریٹجک رسک

-

رجحان کی تبدیلی کا خطرہ: مضبوط رجحان مارکیٹ میں عمدہ کارکردگی کا مظاہرہ ، لیکن ہلچل والے بازار میں بار بار تجارت سے نقصان ہوسکتا ہے۔

-

سلائڈ پوائنٹس اور ٹرانزیکشن لاگت: بار بار اسٹاپ نقصان اور متحرک اسٹاپ نقصان سے اعلی ٹرانزیکشن لاگت آسکتی ہے۔

-

زیادہ بہتر بنانے کا خطرہ: بہت سے پیرامیٹرز ہیں جو تاریخی اعداد و شمار کو زیادہ سے زیادہ فٹ ہونے کا سبب بن سکتے ہیں۔

-

فنڈ مینجمنٹ کا خطرہ: اگر ابتدائی فنڈ چھوٹا ہے تو ، کئی بار ریزرو کو مؤثر طریقے سے نافذ کرنا ممکن نہیں ہے۔

-

مارکیٹ میں لیکویڈیٹی کا خطرہ: کم لیکویڈیٹی والے بازاروں میں ، یہ ممکن ہے کہ ٹریڈنگ کو اپنی مرضی کے مطابق قیمت پر انجام دینا مشکل ہو۔

حکمت عملی کی اصلاح کی سمت

-

مارکیٹ کے ماحول کے فلٹر کو متعارف کرانے: مارکیٹ کے ماحول کا فیصلہ کرنے کے لئے رجحان کی طاقت کے اشارے (جیسے ADX) کو شامل کیا جاسکتا ہے ، اور ہلکے بازاروں میں تجارت کی تعدد کو کم کیا جاسکتا ہے۔

-

پوزیشننگ کی حکمت عملی کو بہتر بنائیں: اس بات پر غور کیا جاسکتا ہے کہ رجحان کی طاقت کے مطابق پوزیشننگ کے وقفے اور تعداد کو متحرک طور پر ایڈجسٹ کیا جائے ، نہ کہ ایک مقررہ 0.5 اے ٹی آر اور 5 بار۔

-

اسٹاپ میکانیزم متعارف کروانا: طویل مدتی رجحانات میں ، منافع کو لاک کرنے کے لئے جزوی اسٹاپ سیٹ کیا جاسکتا ہے ، جیسے کہ 3x اے ٹی آر منافع حاصل کرنے پر پوزیشن کی آدھی رقم ختم کردی جائے۔

-

کثیر نسل وابستگی تجزیہ: مجموعی طور پر لاگو ہونے پر ، مجموعی طور پر رسک کمائی کا تناسب بہتر بنانے کے لئے نسلوں کے مابین وابستگی کا تجزیہ شامل کیا جاسکتا ہے۔

-

اتار چڑھاؤ فلٹر شامل کریں: غیر معمولی مارکیٹوں کا مقابلہ کرنے کے لئے انتہائی اتار چڑھاؤ کی مدت کے دوران تجارت کو روکنے یا خطرے کے پیرامیٹرز کو ایڈجسٹ کرنے کے لئے۔

-

آپٹمائزڈ ایگزٹ میکانزم: زیادہ لچکدار ایگزٹ میکانزم جیسے پیراولک SAR یا Chandelier Exit کو استعمال کرنے پر غور کیا جاسکتا ہے۔

خلاصہ کریں۔

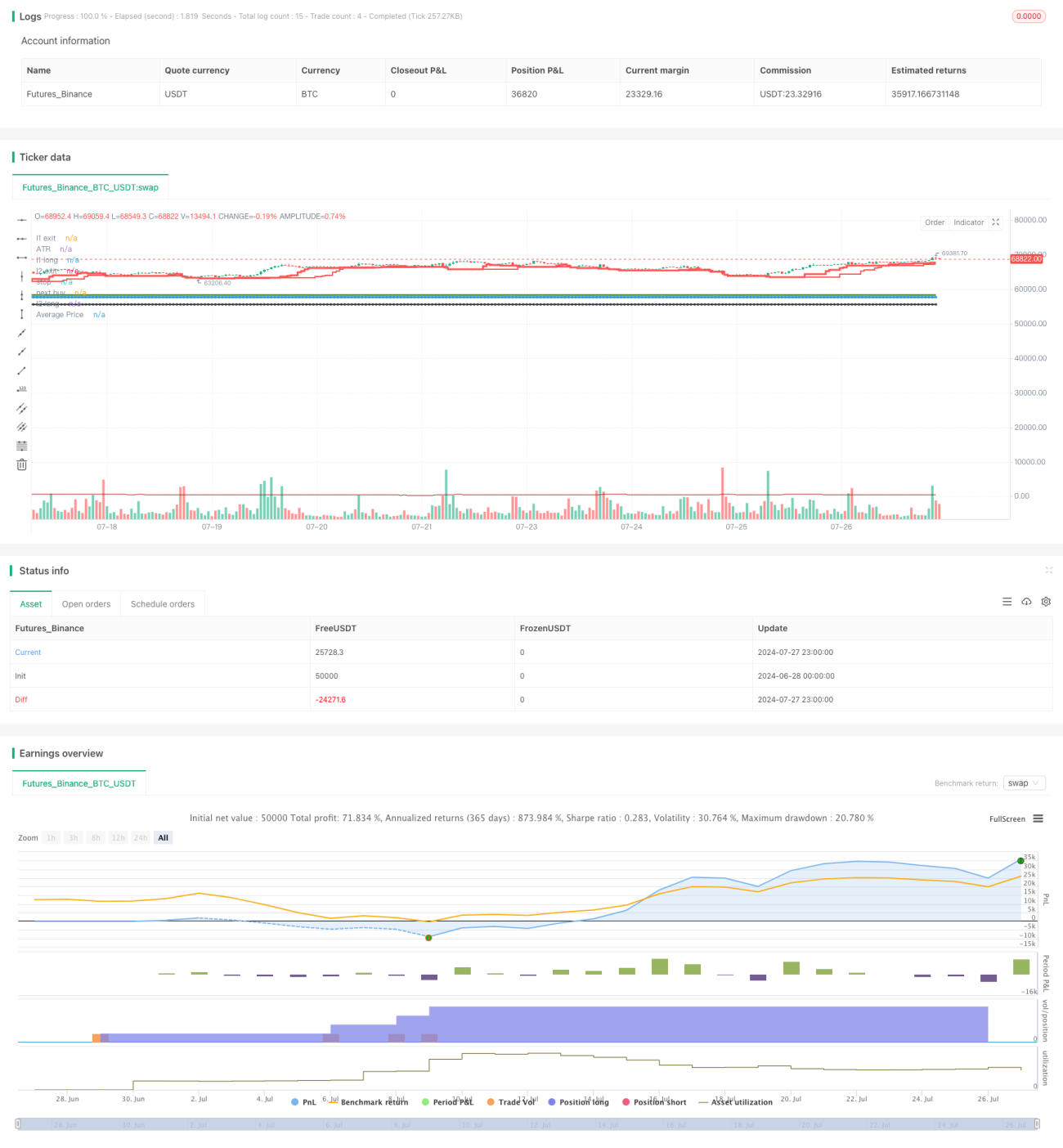

ایک کثیر سطحی متحرک رجحان کی پیروی کا نظام ایک جامع حکمت عملی ہے جو کلاسیکی ساحل سمندر کے تجارتی اصولوں اور جدید مقداری تکنیک کو جوڑتی ہے۔ اس حکمت عملی میں متعدد سطحی رجحانات کی شناخت ، متحرک رسک مینجمنٹ ، اور پرامڈریڈ بیئرنگ جیسے طریقوں کے ذریعہ ، اس حکمت عملی میں استحکام کو برقرار رکھتے ہوئے ، رجحانات پر گرفت اور منافع بخش صلاحیت میں اضافہ کیا گیا ہے۔ اگرچہ یہ ہلچل والی منڈیوں میں چیلنجوں کا سامنا ہے ، لیکن معقول پیرامیٹرز کی اصلاح اور رسک کنٹرول کے ذریعہ ، اس حکمت عملی میں مختلف مارکیٹ کے ماحول میں مستحکم کارکردگی برقرار رکھنے کا امکان ہے۔ مارکیٹ کے ماحول کے فیصلے ، بیئرنگ اور انخلاء کے طریقہ کار کو متعارف کرانے کی طرف سے مستقبل میں مزید بہتری لائی جاسکتی ہے تاکہ حکمت عملی کی غلبہ اور منافع بخش صلاحیت میں اضافہ کیا جاسکے۔

- 1