RSI اور AO کے ساتھ رجحان کی پیروی کرنے والی مقداری تجارتی حکمت عملی

خلاصہ

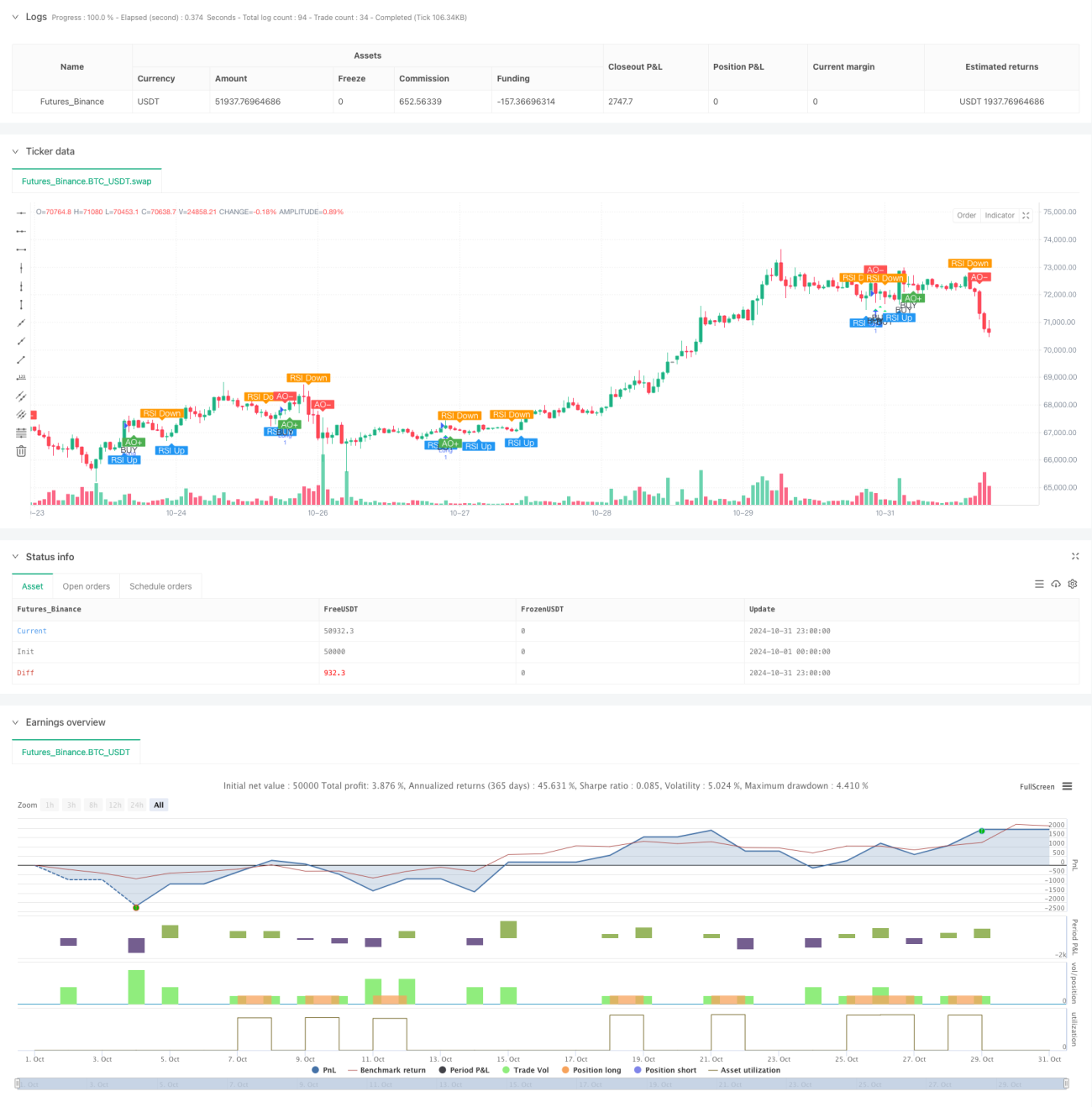

یہ حکمت عملی ایک مقداری تجارتی حکمت عملی ہے جو رشتہ دار طاقت کے اشاریے (RSI) اور رفتار آسیلیٹر (AO) کے اشتراک پر مبنی ہے۔ حکمت عملی بنیادی طور پر RSI کے 50 کی سطح سے اوپر جانے اور AO کے منفی علاقے میں ہونے کے امتزاجی اشارے کو پکڑ کر ممکنہ لمبی پوزیشنوں کی شناخت کرتی ہے۔ حکمت عملی خطرے کے انتظام کے لیے فیصدی منافع اور نقصان کو روکنے کے طریقہ کار کا استعمال کرتی ہے، اور ڈیفالٹ طور پر اکاؤنٹ کے 10% فنڈز کے ساتھ تجارت کرتی ہے۔

حکمت عملی کا اصول

حکمت عملی کا بنیادی منطق دو تکنیکی اشاریوں کے اشتراک پر مبنی ہے:

- RSI اشاریہ: قیمت کی رفتار کی نگرانی کے لیے 14 ادوار کا RSI استعمال کیا جاتا ہے، جب RSI 50 کی مرکزی لائن کو عبور کرتا ہے تو اسے价格上涨 کی رفتار کے قیام کے طور پر دیکھا جاتا ہے۔

- AO اشاریہ: 5 اور 34 ادوار کی حرکت پذیری اوسط کا موازنہ کر کے قیمت کی رفتار کا حساب لگایا جاتا ہے، جب AO منفی ہوتا ہے تو اس کا مطلب ہے کہ مارکیٹ زیادہ فروخت شدہ علاقے میں ہے۔

- داخلے کی شرط: جب RSI 50 کو عبور کرتا ہے اور AO منفی ہوتا ہے تو لمبی پوزیشن کھولی جاتی ہے، یعنی جب قیمت زیادہ فروخت شدہ علاقے میں الٹنے کا اشارہ دیتی ہے۔

- خارج ہونے کی شرط: 2% منافع اور 1% نقصان کی حد مقرر کی گئی ہے تاکہ ہر تجارت کے خطرے اور منافع کا تناسب مناسب رہے۔

حکمت عملی کے فوائد

- اعلیٰ اعتماد کے اشارے: RSI اور AO کی دوہری تصدیق سے تجارتی اشاروں کی قابل اعتمادی بڑھ جاتی ہے۔

- مکمل خطرے کا کنٹرول: مقررہ فیصدی منافع اور نقصان کی حدیں ہر تجارت کے خطرے کو مؤثر طریقے سے کنٹرول کرتی ہیں۔

- سائنسی سرمایہ کا انتظام: اکاؤنٹ کے فنڈز کے مقررہ فیصد کے ساتھ تجارت کرنے سے ضرورت سے زیادہ لیوریج سے بچا جاتا ہے۔

- واضح اور آسان منطق: حکمت عملی کے قواعد سمجھنے اور ان پر عمل کرنے میں آسان ہیں۔

- بہتر بصری اثر: چارٹ پر مختلف اشارے واضح طور پر نشان زد کیے گئے ہیں، جس سے تاجر کی شناخت اور تصدیق آسان ہو جاتی ہے۔

حکمت عملی کے خطرات

- جھوٹے بریک آؤٹ کا خطرہ: RSI کا 50 کو عبور کرنا جھوٹا بریک آؤٹ ہو سکتا ہے، اس لیے دیگر تکنیکی اشاریوں سے تصدیق کی ضرورت ہے۔

- بہت چھوٹا سٹاپ نقصان: 1% کا سٹاپ نقصان بہت چھوٹا ہو سکتا ہے اور مارکیٹ کے اتار چڑھاؤ سے آسانی سے ٹکرا سکتا ہے۔

- یک طرفہ تجارت کی پابندی: حکمت عملی صرف لمبی پوزیشن کھولتی ہے، مختصر پوزیشن نہیں، جس کی وجہ سے مندی کی مارکیٹ کے مواقع ضائع ہو سکتے ہیں۔

- سلپج کا اثر: جب مارکیٹ میں شدید اتار چڑھاؤ ہو تو سلپج کا خطرہ زیادہ ہو سکتا ہے۔

- پیرامیٹرز کی حساسیت: حکمت عملی کی تاثیر RSI اور AO کے پیرامیٹرز کی ترتیب سے بہت زیادہ متاثر ہوتی ہے۔

حکمت عملی کی اصلاح کی سمت

- اشارے کی فلٹریشن: اشاروں کی قابل اعتمادی بڑھانے کے لیے حجم کی تصدیق کا طریقہ کار شامل کرنے کی تجویز ہے۔

- متحرک سٹاپ نقصان: مقررہ سٹاپ نقصان کو ٹریلنگ سٹاپ میں تبدیل کیا جا سکتا ہے تاکہ منافع کی بہتر حفاظت ہو سکے۔

- پیرامیٹرز کی اصلاح: RSI کے دورانیے اور AO کے پیرامیٹرز کے لیے تاریخی بیک ٹیسٹنگ کی سفارش کی جاتی ہے۔

- مارکیٹ کی چھانٹی: مارکیٹ کے رجحان کا تعین کرنے کے لیے فلٹر شامل کریں، صرف اس وقت تجارت کھولیں جب بڑا رجحان اوپر کی طرف ہو۔

- پوزیشن کا انتظام: اشارے کی طاقت کے مطابق پوزیشن کھولنے کے فیصد کو متحرک طور پر ایڈجسٹ کیا جا سکتا ہے۔

خلاصہ

یہ ایک رجحان پر مبنی تجارتی حکمت عملی ہے جو RSI اور AO اشاریوں کو یکجا کرتی ہے، اور زیادہ فروخت شدہ علاقے میں الٹنے کے اشارے پکڑ کر لمبی پوزیشنیں کھولتی ہے۔ حکمت عملی کا ڈیزائن مناسب ہے اور خطرے کا کنٹرول بھی ٹھیک ہے، لیکن اس میں بہتری کی گنجائش موجود ہے۔ تاجروں کو مشورہ دیا جاتا ہے کہ اصل مارکیٹ میں استعمال کرنے سے پہلے مکمل تاریخی بیک ٹیسٹنگ کریں اور مارکیٹ کی حقیقی صورتحال کے مطابق پیرامیٹرز کو ایڈجسٹ کریں۔ یہ حکمت عملی ان تاجروں کے لیے موزوں ہے جن کی خطرہ برداشت کرنے کی صلاحیت زیادہ ہو اور تکنیکی تجزیے کی سمجھ بھی ہو۔

/*backtest

start: 2024-10-01 00:00:00

end: 2024-10-31 23:59:59

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="🐂 BUY Only - RSI Crossing 50 + AO Negative", shorttitle="🐂 AO<0 RSI+50 Strategy", overlay=true)

// ------------------------------ 1