متعدد تکنیکی اشاروں کی رجحان کی پیروی کی حکمت عملی جو بادل چارٹ بریک آؤٹ اور اسٹاپ لاس سسٹم کے ساتھ مربوط ہے

خلاصہ

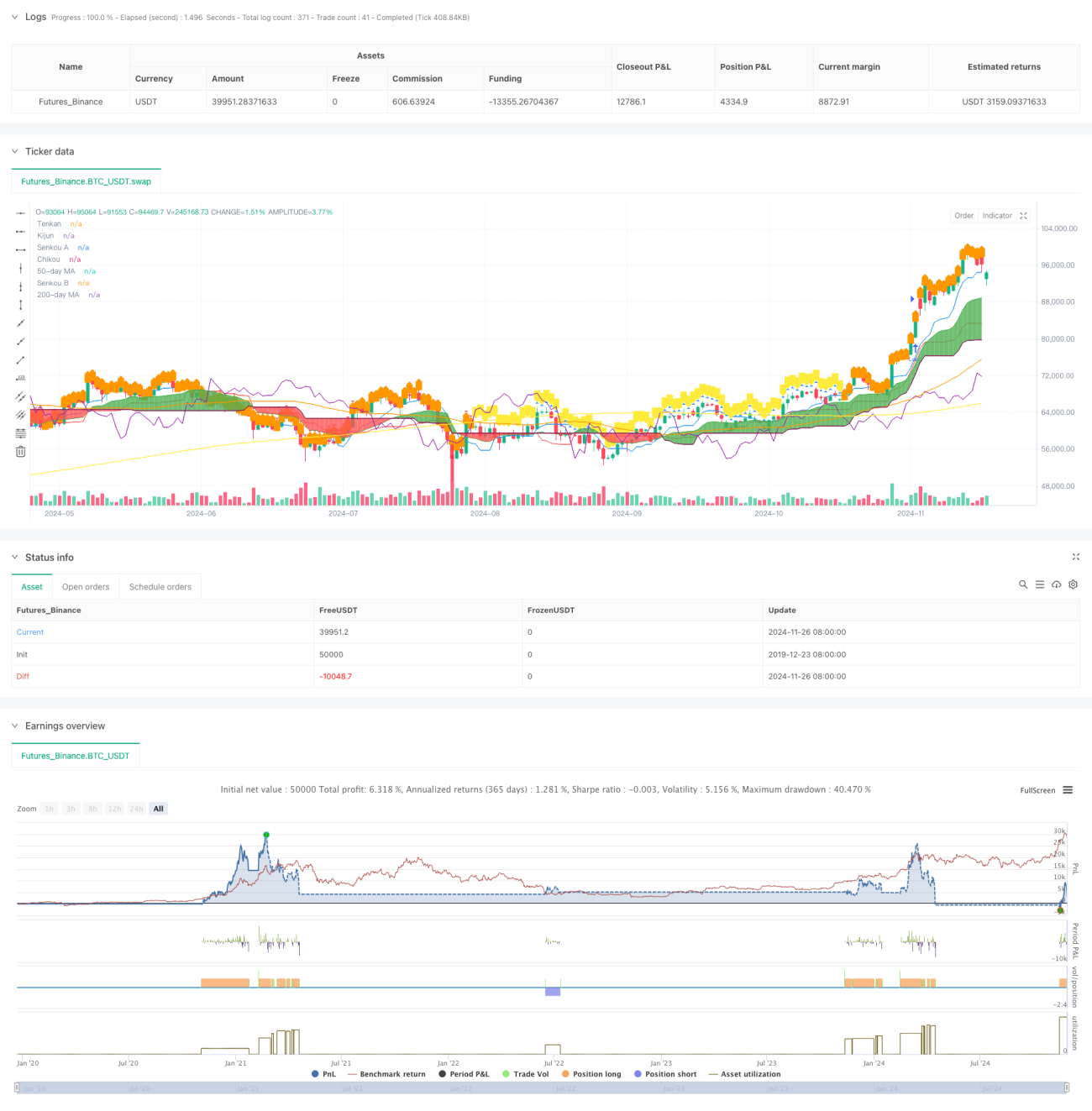

یہ حکمت عملی متعدد تکنیکی اشاروں کا ایک مکمل تجارتی نظام ہے، جو بنیادی طور پر ایشیموکو کلاؤڈ (Ichimoku Cloud) اشارے کی بنیاد پر تجارتی فیصلے کرتی ہے۔ یہ نظام ٹینکن (Tenkan) اور کیجن (Kijun) کے کراس اوور کے ذریعے داخلے کے مواقع کا تعین کرتا ہے، جبکہ ریلیٹیو سٹرینتھ انڈیکس (RSI) اور موونگ ایوریج (MA) کو معاون فلٹر کے طور پر استعمال کرتا ہے۔ حکمت عملی کلاؤڈ کے اجزاء کو متحرک نقصان روکنے کی حد (Stop Loss) کے طور پر استعمال کرتی ہے، جس سے ایک مکمل رسک کنٹرول سسٹم تشکیل پاتا ہے۔

حکمت عملی کا اصول

حکمت عملی کا بنیادی منطق درج ذیل اہم عوامل پر مبنی ہے:

- داخلے کا سگنل ٹینکن اور کیجن کے کراس اوور سے پیدا ہوتا ہے، اوپر کی طرف کراس کرنا لمبی پوزیشن کا سگنل دیتا ہے، جبکہ نیچے کی طرف کراس کرنا چھوٹی پوزیشن کا سگنل دیتا ہے۔

- قیمت کا کومو (Kumo) یعنی بادل کے حوالے سے مقام رجحان کی تصدیق کے لیے استعمال ہوتا ہے، قیمت بادل کے اوپر ہو تو لمبی پوزیشن، قیمت بادل کے نیچے ہو تو چھوٹی پوزیشن۔

- 50 دن اور 200 دن کی موونگ ایوریجز کے درمیان تعلق رجحان کے فلٹر کے طور پر کام کرتا ہے۔

- ہفتہ وار RSI انڈیکیٹر مارکیٹ کی طاقت کی تصدیق اور جھوٹے سگنلز کو فلٹر کرنے کے لیے استعمال ہوتا ہے۔

- کلاؤڈ کے اوپری اور نچلے اطراف کو متحرک نقصان روکنے کی حد کے طور پر استعمال کیا جاتا ہے، جس سے رسک کا متحرک انتظام ممکن ہوتا ہے۔

حکمت عملی کے فوائد

- متعدد تکنیکی اشاروں کا امتزاج زیادہ قابل اعتماد تجارتی سگنل فراہم کرتا ہے، جس سے جھوٹے سگنلز کے اثرات نمایاں طور پر کم ہو جاتے ہیں۔

- کلاؤڈ کو متحرک نقصان روکنے کی حد کے طور پر استعمال کرنے سے مارکیٹ کے اتار چڑھاؤ کے مطابق خود بخود نقصان روکنے کی حد کو ایڈجسٹ کیا جا سکتا ہے، جس سے منافع کی حفاظت بھی ہوتی ہے اور قیمت کو مناسب اتار چڑھاؤ کی گنجائش بھی ملتی ہے۔

- ہفتہ وار RSI کے فلٹر کے ذریعے ضرورت سے زیادہ خریدے گئے یا فروخت کیے گئے علاقوں میں نقصان دہ تجارت سے بچا جا سکتا ہے۔

- موونگ ایوریجز کا کراس اوور اضافی رجحان کی تصدیق فراہم کرتا ہے، جس سے تجارت کی کامیابی کی شرح بہتر ہوتی ہے۔

- یہ ایک مکمل رسک کنٹرول سسٹم ہے جس میں داخلے، پوزیشن برقرار رکھنے اور خارج ہونے کے تمام مراحل شامل ہیں۔

حکمت عملی کے خطرات

- متعدد اشاروں کے فلٹرز کی وجہ سے کچھ ممکنہ اچھے مواقع ضائع ہو سکتے ہیں۔

- ضمنی (Sideways) مارکیٹ میں بار بار جھوٹے بریک آؤٹ سگنلز پیدا ہو سکتے ہیں۔

- ایشیموکو کلاؤڈ انڈیکیٹر میں قدرے تاخیر ہوتی ہے، جو داخلے کے وقت کو متاثر کر سکتی ہے۔

- تیزی سے اتار چڑھاؤ والی مارکیٹ میں متحرک نقصان روکنے کی حد بہت زیادہ ڈھیلی ہو سکتی ہے۔

- بہت زیادہ فلٹر شرائط کی وجہ سے تجارتی مواقع کم ہو سکتے ہیں، جس سے حکمت عملی کی مجموعی منافع متاثر ہو سکتی ہے۔

حکمت عملی کی بہتری کی سمت

- اتار چڑھاؤ کے اشاریے (Volatility Indicator) کو شامل کریں تاکہ مارکیٹ کے اتار چڑھاؤ کے مطابق حکمت عملی کے پیرامیٹرز کو ایڈجسٹ کیا جا سکے۔

- ایشیموکو کلاؤڈ کے پیرامیٹرز کو بہتر بنائیں تاکہ وہ مختلف مارکیٹ ماحول کے لیے زیادہ موزوں ہوں۔

- تجارتی حجم کا تجزیہ شامل کریں تاکہ سگنلز کی قابل اعتمادی بڑھے۔

- وقت پر مبنی فلٹر متعارف کروائیں تاکہ زیادہ اتار چڑھاؤ والے اوقات سے بچا جا سکے۔

- خودکار پیرامیٹر آپٹیمائزیشن سسٹم تیار کریں تاکہ حکمت عملی کو متحرک طور پر ایڈجسٹ کیا جا سکے۔

خلاصہ

یہ حکمت عملی متعدد تکنیکی اشاروں کو ملا کر ایک مکمل تجارتی نظام تشکیل دیتی ہے۔ یہ نہ صرف سگنلز کی پیداوار پر توجہ دیتی ہے بلکہ اس میں رسک کنٹرول کا ایک مکمل طریقہ کار بھی شامل ہے۔ متعدد فلٹر شرائط کے ذریعے تجارت کی کامیابی کی شرح کو مؤثر طریقے سے بڑھایا گیا ہے۔ اس کے علاوہ، متحرک نقصان روکنے کی حد کا ڈیزائن حکمت عملی کو ایک اچھا رسک ریوارڈ تناسب فراہم کرتا ہے۔ اگرچہ بہتری کی کچھ گنجائش موجود ہے، لیکن مجموعی طور پر یہ ایک مکمل ڈھانچہ اور واضح منطق کا حامل حکمت عملی نظام ہے۔

- 1