خلاصہ

یہ ایک کثیر سطحی تجارتی حکمت عملی ہے جو موافقت پذیر اوسط حقیقی رینج (ATR) کے حساب اور رفتار پر مبنی رجحان کی شناخت کو یکجا کرتی ہے۔ اس حکمت عملی کی سب سے نمایاں خصوصیت اس کا منفرد 7 مرحلہ منافع حاصل کرنے کا طریقہ کار ہے، جو 4 ATR پر مبنی خارجی سطحوں اور 3 مقررہ فیصدی سطحوں کو ملاتا ہے۔ یہ مخلوط نقطہ نظر تاجروں کو بازار کے اتار چڑھاؤ کے مطابق متحرک طور پر ایڈجسٹ کرنے اور تیزی اور مندی والی دونوں مارکیٹوں میں منظم طریقے سے منافع حاصل کرنے کی اجازت دیتا ہے۔ یہ حکمت عملی ATR حساب، رجحان کی شدت کی نشاندہی اور منافع کے متعدد طریقہ کار کے متحرک امتزاج کے ذریعے تاجروں کو ایک جامع تجارتی حل فراہم کرتی ہے۔

حکمت عملی کا اصول

یہ حکمت عملی درج ذیل کلیدی اجزاء کے ذریعے کام کرتی ہے:

- بہتر حقیقی رینج کا حساب: قیمت کی سب سے نمایاں حرکت کو مدنظر رکھتے ہوئے بازار کے اتار چڑھاؤ کی پیمائش کرنا۔

- رفتار عنصر کا انضمام: حالیہ قیمت کی نقل و حرکت کی بنیاد پر ATR کو ایڈجسٹ کرنا، جس سے یہ زیادہ موافقت پذیر ہو جاتا ہے۔

- موافقت پذیر ATR حساب: رفتار کے عنصر کے مطابق روایتی ATR کو ایڈجسٹ کرنا تاکہ یہ اتار چڑھاؤ کے دوران زیادہ حساس ہو۔

- رجحان کی شدت کی مقدار: پیچیدہ الگورتھم کے ذریعے رجحان کی شدت کا اندازہ لگانا۔

- سات مرحلہ منافع کا طریقہ کار: ATR پر مبنی چار خارجی سطحیں اور تین مقررہ فیصدی سطحیں شامل ہیں۔

حکمت عملی کے فوائد

- موافقت پذیری: متحرک ATR حساب کے ذریعے مختلف بازاروں کے حالات کے مطابق ڈھلنا۔

- رسک مینجمنٹ مکمل: منافع کی کثیر سطحیں منظم خطرے پر قابو پانے کا ذریعہ فراہم کرتی ہیں۔

- اعلی لچک: تیزی اور مندی دونوں مارکیٹوں میں یکساں طور پر موثر طریقے سے کام کر سکتی ہے۔

- پیرامیٹرز قابل ایڈجسٹ: مختلف تجارتی اندازوں کے مطابق ڈھالنے کے لیے متعدد ایڈجسٹ ایبل پیرامیٹرز فراہم کرتا ہے۔

- منظم عمل: واضح داخلے اور خارج ہونے کے قوانین جذباتی تجارت کو کم کرتے ہیں۔

حکمت عملی کے خطرات

- پیرامیٹرز کی حساسیت: غلط پیرامیٹر سیٹنگز زیادہ تجارت یا مواقع سے محرومی کا سبب بن سکتی ہیں۔

- بازار کے حالات پر انحصار: شدید اتار چڑھاؤ یا سائیڈ وے مارکیٹوں میں خراب کارکردگی دکھا سکتی ہے۔

- پیچیدگی کا خطرہ: منافع کے کثیر سطحی طریقہ کار عملدرآمد میں دشواری پیدا کر سکتے ہیں۔

- سلپج کا اثر: منافع کے متعدد نکات سلپج سے نمایاں طور پر متاثر ہو سکتے ہیں۔

- سرمائے کے انتظام کی ضرورت: کثیر سطحی منافع کی حکمت عملی پر عمل کرنے کے لیے کافی سرمائے کی ضرورت ہے۔

حکمت عملی کی بہتری کے راستے

- متحرک پیرامیٹر ایڈجسٹمنٹ: مارکیٹ کے حالات کے مطابق خودکار طور پر پیرامیٹرز کو ایڈجسٹ کرنا۔

- مارکیٹ ماحول کی فلٹریشن: مارکیٹ ماحول کی شناخت کا طریقہ کار شامل کرنا۔

- رسک مینجمنٹ میں اضافہ: متحرک اسٹاپ لاس طریقہ کار متعارف کرانا۔

- عملدرآمد کی بہتری: سلپج کے اثر کو کم کرنے کے لیے منافع کے طریقہ کار کو آسان بنانا۔

- بیک ٹیسٹنگ فریم ورک کی تکمیل: مزید حقیقت پسندانہ تجارتی عوامل شامل کرنا۔

خلاصہ

یہ حکمت عملی موافقت پذیر ATR اور منافع کے کثیر سطحی طریقہ کار کو ملا کر تاجروں کو ایک جامع تجارتی نظام فراہم کرتی ہے۔ اس کا فائدہ مختلف بازاروں کے حالات کے مطابق ڈھلنے کی صلاحیت اور منظم طریقے سے خطرے کا انتظام کرنے میں ہے۔ اگرچہ کچھ ممکنہ خطرات موجود ہیں، لیکن مناسب بہتری اور رسک مینجمنٹ کے ساتھ یہ حکمت عملی ایک موثر تجارتی آلہ بن سکتی ہے۔ اس کا اختراعی کثیر سطحی منافع کا طریقہ کار خاص طور پر ان تاجروں کے لیے موزوں ہے جو خطرے پر قابو رکھتے ہوئے منافع کو زیادہ سے زیادہ کرنا چاہتے ہیں۔

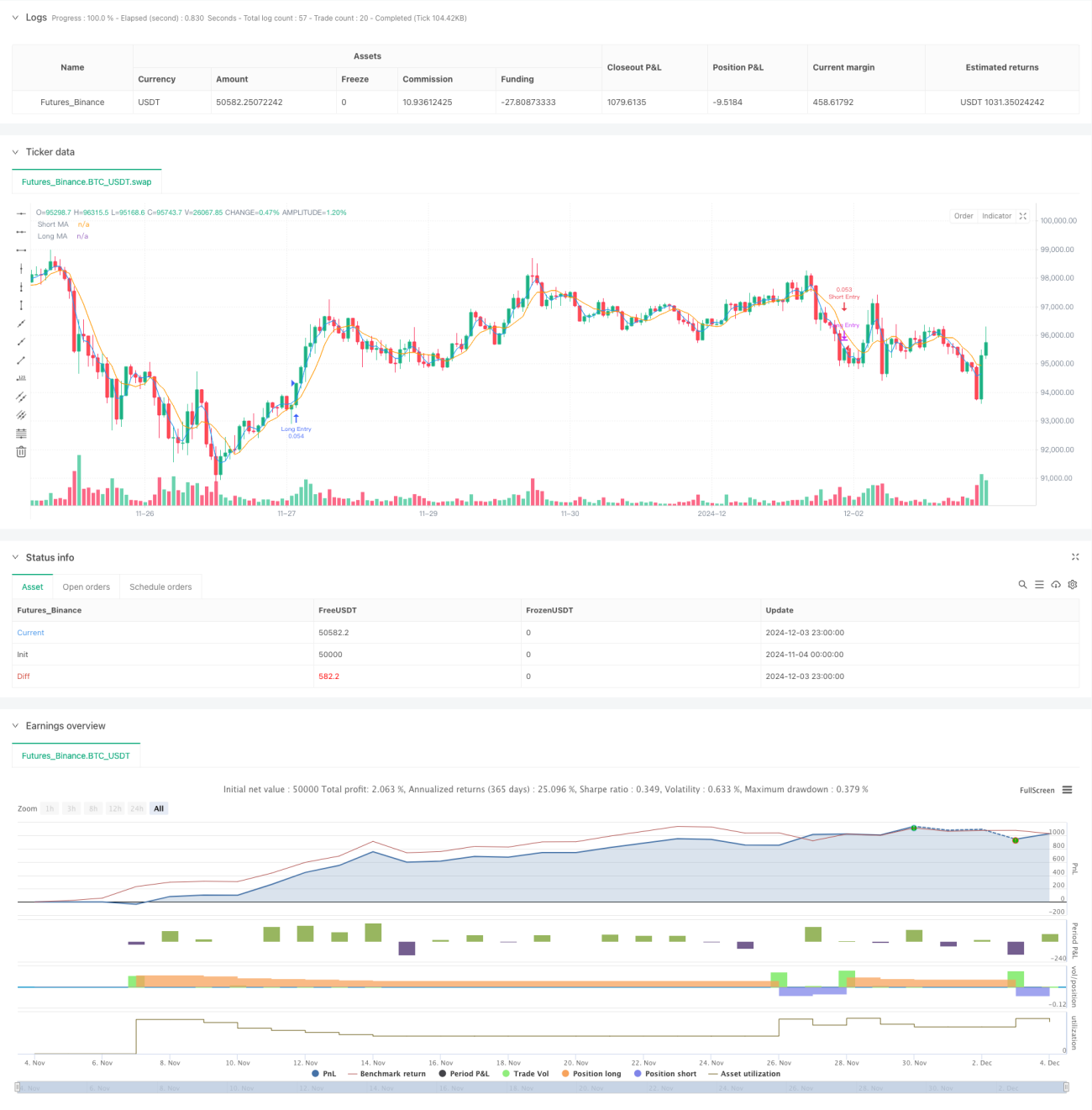

/*backtest

start: 2024-11-04 00:00:00

end: 2024-12-04 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// The SuperATR 7-Step Profit Strategy is a multi-layered trading strategy that combines adaptive ATR and momentum-based trend detection - 1