اعلیٰ متحرک ٹریلنگ اسٹاپ لاس اور ہدف منافع کی حکمت عملی

خلاصہ

یہ حکمت عملی ایک جدید تجارتی نظام ہے جو متحرک تعاقب کرنے والے اسٹاپ لاس، خطرہ-انعام تناسب اور RSI انتہائی قدروں سے خارج ہونے کو یکجا کرتی ہے۔ یہ حکمت عملی مارکیٹ میں مخصوص نمونوں (متوازی کینڈل اسٹک پیٹرن اور سوئی کی شکل کے کینڈل اسٹک پیٹرن) کی شناخت کرکے تجارت کرتی ہے، جبکہ ATR اور حالیہ کم ترین قیمت کا استعمال کرتے ہوئے متحرک اسٹاپ لاس مقرر کرتی ہے اور پیش طے شدہ خطرہ-انعام تناسب کی بنیاد پر منافع کے اہداف طے کرتی ہے۔ یہ نظام RSI انڈیکیٹر پر مبنی مارکیٹ کے زیادہ گرم/بہت سرد ہونے کے فیصلہ کن طریقہ کار کو بھی مربوط کرتا ہے، جو مارکیٹ کی انتہائی قدروں پر بروقت پوزیشن بند کرنے کی اجازت دیتا ہے۔

حکمت عملی کا اصول

حکمت عملی کے بنیادی منطق میں درج ذیل اہم حصے شامل ہیں:

- داخلے کا اشارہ دو نمونوں پر مبنی ہے: متوازی کینڈل اسٹک پیٹرن (بڑی سبز موم بتی کے بعد بڑی سرخ موم بتی) اور دوہری سوئی کی شکل کا کینڈل اسٹک پیٹرن۔

- متحرک تعاقب کرنے والا اسٹاپ لاس ATR ضرب کا استعمال کرتے ہوئے حالیہ N کینڈلز کی کم ترین قیمت کو ایڈجسٹ کرتا ہے، تاکہ اسٹاپ لاس مارکیٹ کے اتار چڑھاؤ کے مطابق متحرک طور پر ڈھل سکے۔

- منافع کا ہدف ایک مقررہ خطرہ-انعام تناسب کی بنیاد پر طے کیا جاتا ہے، جو ہر تجارت کے خطرے کی قدر (R) کا حساب لگا کر مقرر کیا جاتا ہے۔

- پوزیشن کا سائز مقررہ خطرے کی رقم اور ہر تجارت کے خطرے کی قدر کی بنیاد پر متحرک طور پر شمار کیا جاتا ہے۔

- RSI انتہائی قدروں سے خارج ہونے کا طریقہ کار مارکیٹ کے زیادہ گرم یا بہت سرد ہونے پر بند ہونے کا اشارہ متحرک کرتا ہے۔

حکمت عملی کے فوائد

- متحرک رسک مینجمنٹ: ATR اور حالیہ کم ترین قیمت کے امتزاج کی بدولت اسٹاپ لاس مارکیٹ کے اتار چڑھاؤ کے مطابق متحرک طور پر ایڈجسٹ ہوتا ہے۔

- درست پوزیشن کنٹرول: مقررہ خطرے کی رقم پر مبنی پوزیشن کے سائز کا حساب کتاب یقینی بناتا ہے کہ ہر تجارت پر یکساں خطرہ ہو۔

- کثیر جہتی خارج ہونے کا طریقہ کار: تعاقب کرنے والے اسٹاپ لاس، مقررہ منافع کے ہدف اور RSI انتہائی قدروں کے تین گنا خارج ہونے کے طریقہ کار کو یکجا کرتا ہے۔

- لچکدار تجارتی سمت کا انتخاب: صرف خرید، صرف فروخت یا دو طرفہ تجارت کا انتخاب ممکن ہے۔

- واضح خطرہ-انعام کی ترتیب: پیش طے شدہ خطرہ-انعام تناسب کے ذریعے ہر تجارت کے منافع کے ہدف کو واضح کیا جاتا ہے۔

حکمت عملی کے خطرات

- نمونوں کی شناخت کی درستگی کا خطرہ: متوازی کینڈل اور سوئی کی شکل کے کینڈل کی شناخت میں غلطی ہو سکتی ہے۔

- اسٹاپ لاس میں سلپج کا خطرہ: شدید اتار چڑھاؤ والی مارکیٹ میں بڑی سلپج کا سامنا ہو سکتا ہے۔

- RSI انتہائی قدروں سے قبل از وقت خارج ہونا: مضبوط رجحان والی مارکیٹ میں قبل از وقت بند ہونے کی وجہ سے مزید منافع سے محرومی ہو سکتی ہے۔

- مقررہ خطرہ-انعام تناسب کی حدود: مختلف مارکیٹ کے حالات میں بہترین خطرہ-انعام تناسب مختلف ہو سکتا ہے۔

- پیرامیٹر آپٹیمائزیشن کا اوور فٹنگ خطرہ: متعدد پیرامیٹرز کا مجموعہ زیادہ بہتر بنانے کا سبب بن سکتا ہے۔

حکمت عملی کی بہتری کی سمت

- داخلے کے اشارے کی بہتری: مزید نمونوں کی تصدیق کرنے والے انڈیکیٹرز جیسے حجم، رجحان انڈیکیٹرز وغیرہ شامل کیے جا سکتے ہیں۔

- متحرک خطرہ-انعام تناسب: مارکیٹ کے اتار چڑھاؤ کے مطابق خطرہ-انعام تناسب کو متحرک طور پر ایڈجسٹ کیا جا سکتا ہے۔

- ذہین پیرامیٹر خود موافقت: مشین لرننگ الگورتھم متعارف کر کے پیرامیٹرز کی متحرک بہتری کی جا سکتی ہے۔

- متعدد ٹائم فریم کی تصدیق: مزید ٹائم فریموں سے سگنل کی تصدیق کے طریقہ کار شامل کیے جا سکتے ہیں۔

- مارکیٹ کے حالات کی درجہ بندی: مختلف مارکیٹ کے حالات کے لیے مختلف پیرامیٹر سیٹ استعمال کیے جا سکتے ہیں۔

خلاصہ

یہ ایک اچھی طرح سے ڈیزائن کردہ تجارتی حکمت عملی ہے، جو متعدد پختہ تکنیکی تجزیہ تصورات کو یکجا کرکے ایک مکمل تجارتی نظام تشکیل دیتی ہے۔ حکمت عملی کا فائدہ اس کے جامع رسک مینجمنٹ سسٹم اور لچکدار تجارتی اصولوں میں ہے، لیکن پیرامیٹر آپٹیمائزیشن اور مارکیٹ کی موافقت کے مسائل پر بھی توجہ دینے کی ضرورت ہے۔ تجویز کردہ بہتری کی سمتوں کے ذریعے، اس حکمت عملی میں مزید بہتری کی گنجائش ہے۔

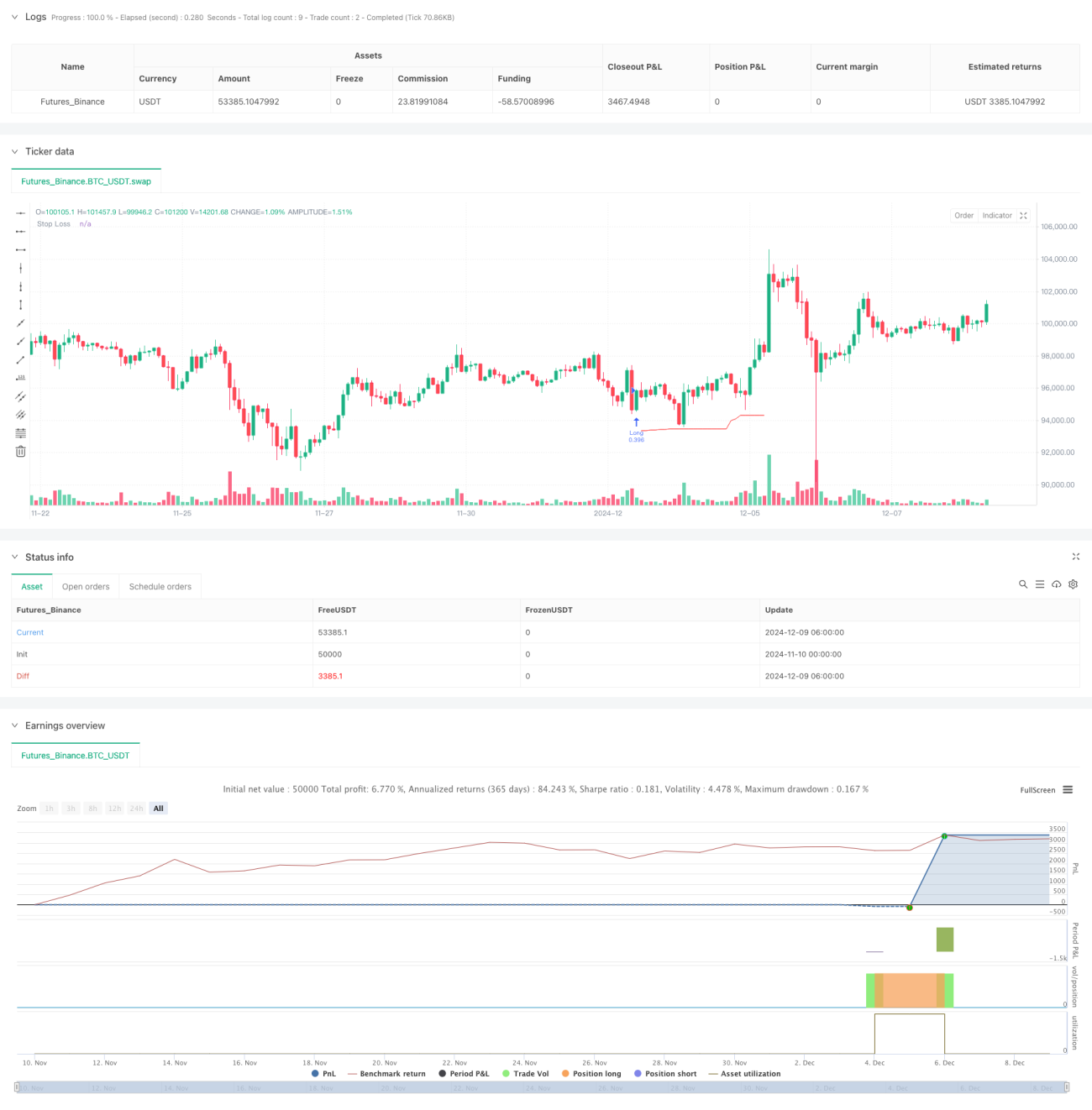

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 2h

basePeriod: 2h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © ZenAndTheArtOfTrading | www.TheArtOfTrading.com

// @version=5

strategy("Trailing stop 1", overlay=true)- 1