یہ حکمت عملی RSI ڈائنامک آسیلیٹر پر مبنی ایک مقداری تجارتی نظام ہے۔ RSI انڈیکیٹر پر پولینومیل فٹنگ اور ٹائم سیریز تجزیہ کر کے، RSI کی تبدیلی کی شرح کا حساب لگایا جاتا ہے تاکہ مارکیٹ کی رفتار کو پکڑا جا سکے۔ حکمت عملی QR ڈیکمپوزیشن جیسے اعلیٰ ریاضیاتی طریقوں کو سگنل پروسیسنگ کے لیے استعمال کرتی ہے اور تجارتی فیصلوں کے لیے اوسط لائنوں کے نظام کو شامل کرتی ہے۔

حکمت عملی کا اصول

حکمت عملی کا مرکز ڈیلٹا-RSI آسیلیٹر ہے، جو درج ذیل مراحل کے ذریعے کام کرتا ہے:

- پہلے روایتی RSI انڈیکیٹر کو بنیادی ڈیٹا کے طور پر شمار کیا جاتا ہے

- RSI کو ہموار کرنے اور شور کو کم کرنے کے لیے پولینومیل فٹنگ کا استعمال کیا جاتا ہے

- RSI کے وقتی مشتق کا حساب لگا کر ڈیلٹا-RSI حاصل کیا جاتا ہے، جو RSI کی تبدیلی کی شرح کو ظاہر کرتا ہے

- ڈیلٹا-RSI کا اس کی حرکت پذیری اوسط سے موازنہ کر کے تجارتی سگنل تیار کیے جاتے ہیں

- فٹنگ کے معیار کا جائزہ لینے اور فلٹر کرنے کے لیے مربع جذر کی اوسط غلطی (RMSE) استعمال کی جاتی ہے

تجارتی سگنل تین طریقوں سے پیدا کیے جا سکتے ہیں:

- صفر لائن کا کراسنگ: جب ڈیلٹا-RSI منفی سے مثبت ہو جائے تو لمبی پوزیشن لی جائے، اور مثبت سے منفی ہو جائے تو چھوٹی پوزیشن لی جائے

- سگنل لائن کا کراس: جب ڈیلٹا-RSI اپنی حرکت پذیری اوسط کو اوپر/نیچے کرے تو بالترتیب لمبی/چھوٹی پوزیشن لی جائے

- سمت میں تبدیلی: جب ڈیلٹا-RSI منفی علاقے میں بڑھنا شروع کرے تو لمبی پوزیشن لی جائے، اور جب مثبت علاقے میں گرنا شروع کرے تو چھوٹی پوزیشن لی جائے

حکمت عملی کے فوائد

- مضبوط ریاضیاتی بنیاد: QR ڈیکمپوزیشن جیسے اعلیٰ ریاضیاتی طریقوں کو سگنل پروسیسنگ کے لیے استعمال کیا جاتا ہے، نظریاتی بنیاد قابل اعتماد ہے

- سگنل کی ہمواری: پولینومیل فٹنگ مارکیٹ کے شور کو مؤثر طریقے سے فلٹر کر سکتی ہے اور سگنل کے معیار کو بہتر بنا سکتی ہے

- لچک: مختلف سگنل پیدا کرنے کے طریقے اور پیرامیٹرز کے انتخاب فراہم کیے گئے ہیں، جو مختلف مارکیٹ کے ماحول کے مطابق ڈھل سکتے ہیں

- خطرے پر قابو: اس میں RMSE فلٹرنگ کا طریقہ کار شامل ہے، جس سے زیادہ قابل اعتماد سگنلز کو منتخب کیا جا سکتا ہے

- حساب کی کارکردگی: میٹرکس آپریشنز کے لیے بہتر الگورتھم استعمال کیے گئے ہیں، جس سے عملدرآمد کی کارکردگی زیادہ ہے

حکمت عملی کے خطرات

- پیرامیٹرز کی حساسیت: متعدد اہم پیرامیٹرز کو احتیاط سے ایڈجسٹ کرنے کی ضرورت ہے، پیرامیٹرز کا غلط انتخاب حکمت عملی کی کارکردگی کو شدید متاثر کر سکتا ہے

- تاخیر: سگنل کی ہمواری کچھ تاخیر لاتی ہے، جس کی وجہ سے تیز رفتار مارکیٹ میں مواقع ضائع ہو سکتے ہیں

- جھوٹا بریک آؤٹ: اتار چڑھاؤ والی مارکیٹ میں جھوٹے سگنل پیدا ہو سکتے ہیں، جس سے تجارتی اخراجات بڑھ جاتے ہیں

- حساب کی پیچیدگی: اس میں متعدد میٹرکس آپریشنز شامل ہیں، جو زیادہ تعدد والی تجارت میں کارکردگی کی رکاوٹ بن سکتے ہیں

- زیادہ فٹنگ: پیرامیٹرز کی اصلاح کے دوران تاریخی ڈیٹا میں زیادہ فٹنگ سے بچنے کی ضرورت ہے

حکمت عملی کی اصلاح کی سمت

- خود کار پیرامیٹرز: مارکیٹ کے اتار چڑھاؤ کے مطابق RSI کی مدت اور فٹنگ کی ڈگری کو متحرک طور پر ایڈجسٹ کیا جا سکتا ہے

- متعدد وقت کے ادوار: مزید وقت کے ادوار کے سگنلز کو شامل کر کے کراس تصدیق کی جا سکتی ہے

- اتار چڑھاؤ کا فلٹر: ATR جیسے اتار چڑھاؤ کے انڈیکیٹرز کو سگنل فلٹرنگ کے لیے شامل کیا جا سکتا ہے

- مارکیٹ کی درجہ بندی: مختلف مارکیٹ کی حالتوں (رائج/اتار چڑھاؤ) کے لیے مختلف سگنل پیدا کرنے کے قوانین استعمال کیے جا سکتے ہیں

- نقصان روکنے کی اصلاح: زیادہ ذہین نقصان روکنے کے طریقہ کار شامل کیے جا سکتے ہیں، جیسے سپورٹ اور ریزسٹنس لیول پر مبنی متحرک نقصان روکنا

خلاصہ

یہ ایک مکمل ڈھانچے اور مضبوط نظریاتی بنیادوں والی مقداری تجارتی حکمت عملی ہے۔ RSI کی متحرک خصوصیات کا تجزیہ کر کے اور جدید ریاضیاتی طریقوں کو سگنل پروسیسنگ کے لیے استعمال کر کے، یہ مارکیٹ کے رجحان کو اچھی طرح پکڑ سکتی ہے۔ اگرچہ پیرامیٹرز کی حساسیت اور حساب کی پیچیدگی کے کچھ مسائل ہیں، لیکن مناسب پیرامیٹرز کے انتخاب اور اصلاح و بہتری کے ذریعے، اس حکمت عملی کی عملی قیمت ہے۔ اصل وقت کی تجارت میں خطرے پر قابو رکھنے، مناسب پوزیشن سائز مقرر کرنے، اور حکمت عملی کی کارکردگی کی مسلسل نگرانی کرنے کی سفارش کی جاتی ہے۔

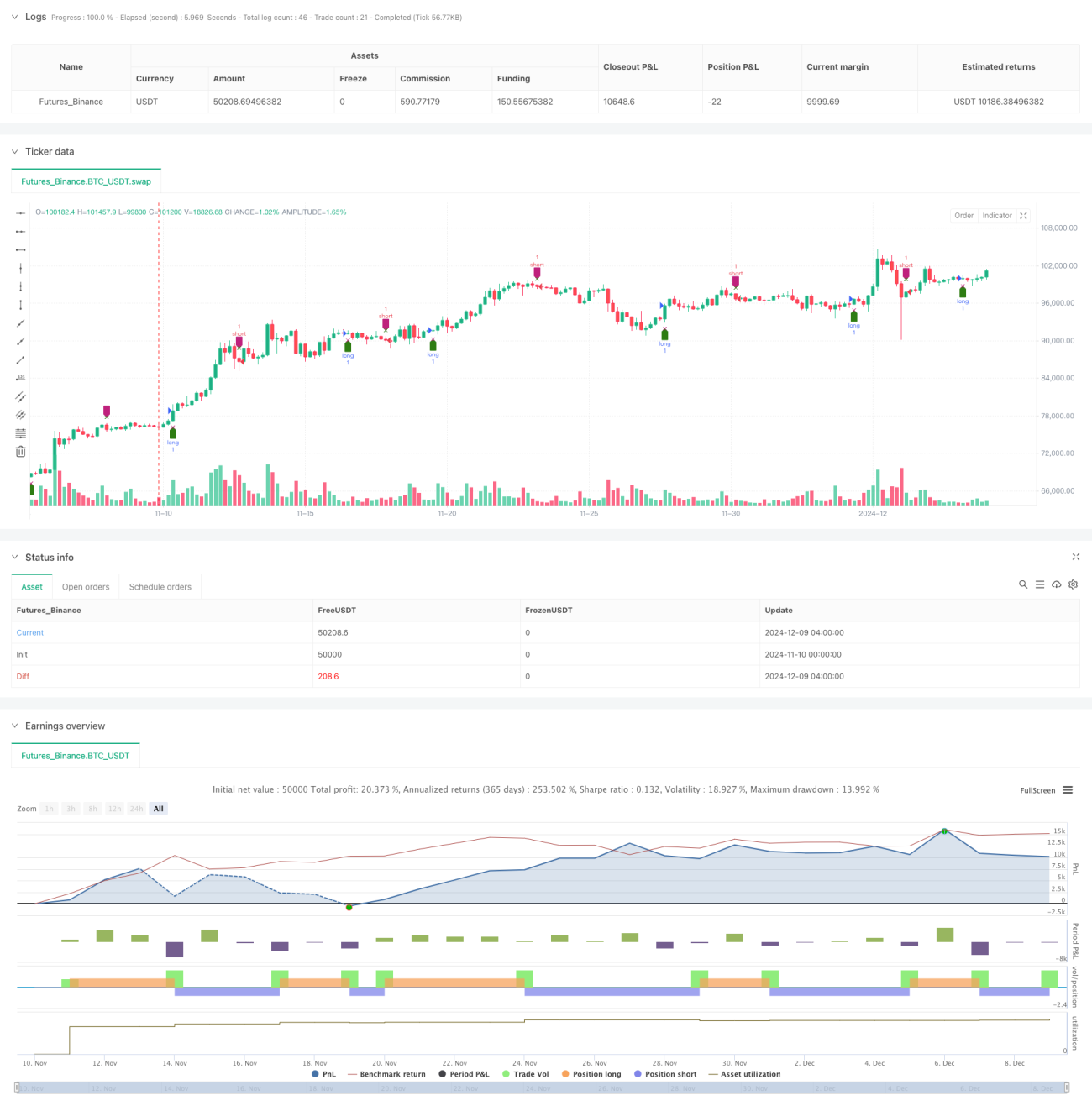

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tbiktag

//

// Delta-RSI Oscillator Strategy- 1