خاکہ

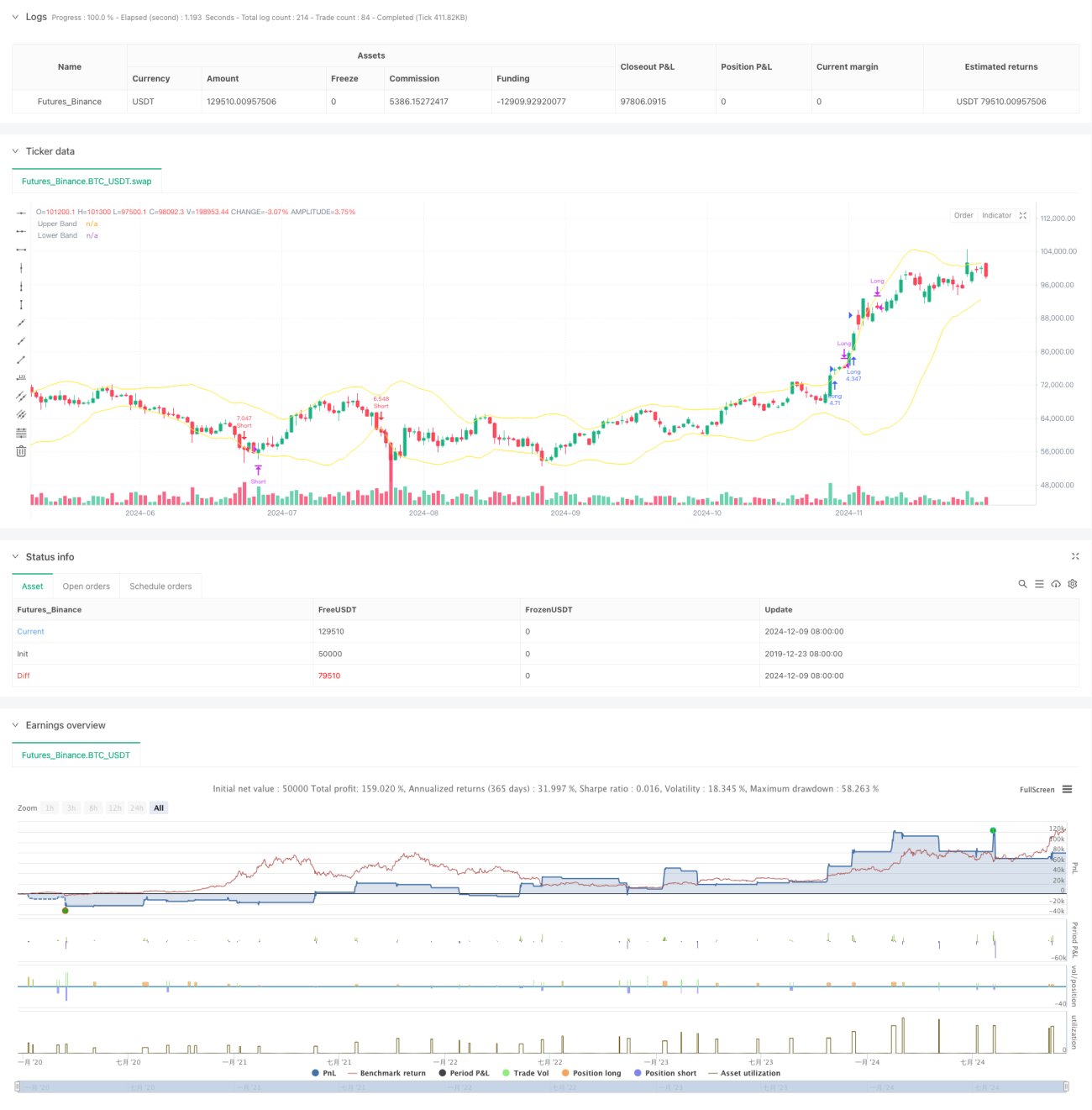

یہ حکمت عملی ایک چار گھنٹے کی سطح کا مقداری تجارتی نظام ہے جو بولنگر بینڈ کے اشاروں پر مبنی ہے، جس میں رجحان کی بریک آؤٹ اور اوسط کی واپسی کے تجارتی تصورات کو یکجا کیا گیا ہے۔ حکمت عملی بولنگر بینڈ کے اوپری اور نچلے بینڈ سے بریک آؤٹ کے ذریعے بازار کی رفتار کو پکڑتی ہے، جبکہ قیمت کے اوسط کی طرف واپس آنے کی خاصیت سے منافع حاصل کرتی ہے اور سٹاپ نقصان کے ذریعے خطرے کو کنٹرول کرتی ہے۔ حکمت عملی میں 3 گنا لیوریج استعمال کیا گیا ہے، جو منافع کو یقینی بنانے کے ساتھ ساتھ خطرے کے کنٹرول کو بھی مدنظر رکھتا ہے۔

حکمت عملی کا اصول

حکمت عملی کا بنیادی منطق درج ذیل اہم عناصر پر مبنی ہے:

- بولنگر بینڈ کے وسطی بینڈ کے طور پر 20 ادوار کی موونگ اوسط کا استعمال، اور 2 معیاری انحراف کے ساتھ اتار چڑھاؤ کی حد مقرر کرنا

- پوزیشن کھولنے کا اشارہ: جب K لائن کی باڈی (کھلنے اور بند ہونے کی قیمتوں کا اوسط) اوپری بینڈ کو توڑے تو لمبی پوزیشن کھولیں، اور جب نچلے بینڈ کو توڑے تو چھوٹی پوزیشن کھولیں

- پوزیشن بند کرنے کا اشارہ: لمبی پوزیشن کے دوران، اگر لگاتار دو K لائنوں کی بند اور کھلنے کی قیمتیں دونوں اوپری بینڈ سے نیچے ہوں اور بند کی قیمت کھلنے کی قیمت سے کم ہو تو پوزیشن بند کریں؛ چھوٹی پوزیشن کے لیے الٹ منطق استعمال کریں

- خطرے کا کنٹرول: پوزیشن کھولتے وقت موجودہ K لائن کی بلند ترین/پست ترین قیمت پر سٹاپ نقصان مقرر کریں تاکہ ہر تجارت میں نقصان قابل کنٹرول ہو

حکمت عملی کے فوائد

- تجارتی منطق واضح: رجحان اور واپسی دونوں تجارتی طریقوں کو یکجا کرتی ہے، جو مختلف بازار کے حالات میں اچھی کارکردگی دکھا سکتی ہے

- خطرے کا کنٹرول مکمل: K لائن کے اتار چڑھاؤ پر مبنی متحرک سٹاپ نقصان مقرر کیا گیا ہے، جو مؤثر طریقے سے پل بیک کو کنٹرول کر سکتا ہے

- جھوٹے اشاروں کی فلٹرنگ: صرف بند کی قیمت پر انحصار کرنے کے بجائے K لائن کی باڈی کی پوزیشن کو دیکھ کر بریک آؤٹ کی تصدیق کرتی ہے، جس سے جھوٹے بریک آؤٹ سے ہونے والے نقصان میں کمی آتی ہے

- سرمایہ کا مناسب انتظام: اکاؤنٹ کی ایکویٹی کی بنیاد پر پوزیشن کے سائز کو متحرک طور پر ایڈجسٹ کرتی ہے، جو منافع کو یقینی بنانے کے ساتھ ساتھ خطرے کو بھی کنٹرول کرتی ہے

حکمت عملی کے خطرات

- منڈی میں اتار چڑھاؤ کا خطرہ: افقی رینج والی منڈی میں بار بار جھوٹے بریک آؤٹ کے اشارے آ سکتے ہیں، جس کے نتیجے میں مسلسل سٹاپ نقصان ہو سکتا ہے

- لیوریج کا خطرہ: 3 گنا لیوریج کا استعمال شدید اتار چڑھاؤ کے دوران بڑے نقصان کا سبب بن سکتا ہے

- سٹاپ نقصان کی ترتیب کا خطرہ: K لائن کی بلند ترین/پست ترین قیمت پر سٹاپ نقصان مقرر کرنا بہت زیادہ نرم ہو سکتا ہے، جس سے ہر تجارت میں نقصان بڑھ سکتا ہے

- وقت کے دورانیے پر انحصار: چار گھنٹے کی سطح بعض بازاروں کے حالات میں بہت سست ردعمل ظاہر کر سکتی ہے، جس سے موقع ہاتھ سے نکل سکتا ہے

حکمت عملی کی بہتری کی سمت

- رجحان فلٹر کا اضافہ: طویل دورانیے کے رجحان کے تعین کے اشارے شامل کیے جا سکتے ہیں تاکہ بنیادی رجحان کی سمت میں تجارت کی جا سکے

- سٹاپ نقصان کی اسکیم کو بہتر بنانا: ATR یا بولنگر بینڈ کی چوڑائی کا استعمال کرتے ہوئے سٹاپ نقصان کے فاصلے کو متحرک طور پر ایڈجسٹ کرنے پر غور کریں

- پوزیشن کے انتظام میں اضافہ: اتار چڑھاؤ یا رجحان کی شدت کے مطابق لیوریج کے تناسب کو متحرک طور پر ایڈجسٹ کریں

- بازار کے ماحول کا تعین شامل کرنا: بازار کی موجودہ حالت کی شناخت کے لیے حجم یا اتار چڑھاؤ کے اشارے متعارف کروائیں، اور منتخب طور پر پوزیشن کھولیں

خلاصہ

یہ ایک حکمت عملی ہے جو بولنگر بینڈ کے رجحان کی پیروی اور اوسط کی واپسی کی خصوصیات کو یکجا کرتی ہے۔ سخت پوزیشن کھولنے اور بند کرنے کی شرائط اور خطرے کے کنٹرول کے اقدامات کے ذریعے، یہ رجحان اور منڈی کے اتار چڑھاؤ دونوں میں مستحکم منافع حاصل کرنے کا ہدف رکھتی ہے۔ حکمت عملی کا بنیادی فائدہ اس کی واضح تجارتی منطق اور مکمل خطرے کے کنٹرول کا نظام ہے، لیکن استحکام اور منافع کی صلاحیت کو مزید بڑھانے کے لیے لیوریج کے استعمال اور بازار کے ماحول کے تعین جیسی بہتریوں پر توجہ دینے کی ضرورت ہے۔

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Bollinger 4H Follow", overlay=true, initial_capital=300, commission_type=strategy.commission.percent, commission_value=0.04)

// StartYear = input(2022,"Backtest Start Year")

// StartMonth = input(1,"Backtest Start Month") - 1