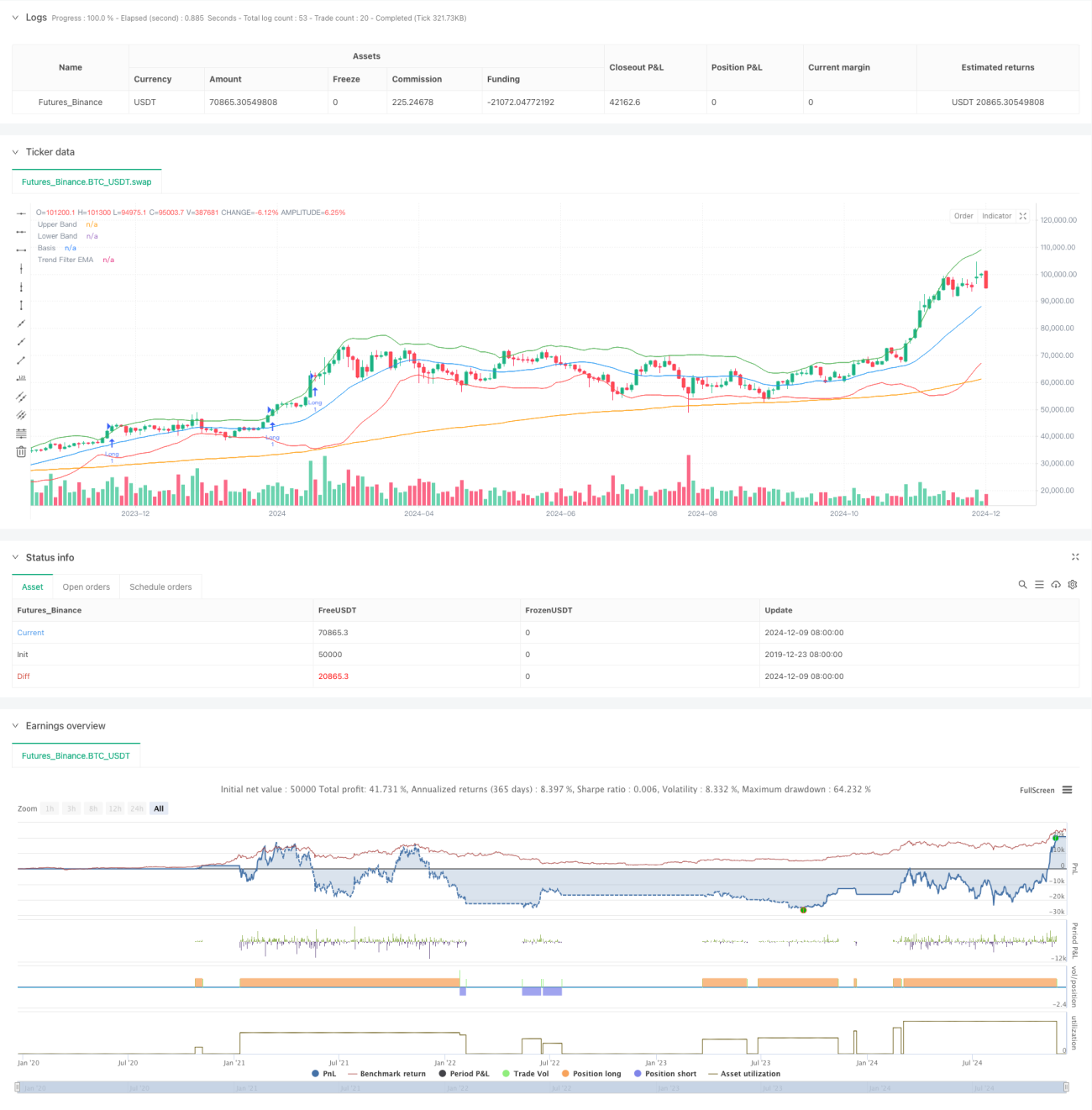

جائزہ

یہ حکمت عملی ایک اعلی درجے کی مقداری تجارتی نظام ہے جو بولنگر بینڈز، RSI اشارے اور 200 پیریڈ EMA کے رجحان فلٹر کو یکجا کرتی ہے۔ یہ نظام متعدد تکنیکی اشاروں کے ہم آہنگی کے ذریعے رجحان کی سمت میں اعلیٰ مواقع کو پکڑتا ہے اور اتار چڑھاؤ والی مارکیٹ میں جھوٹے سگنلز کو مؤثر طریقے سے فلٹر کرتا ہے۔ نظام متحرک سٹاپ لاس اور خطرے سے منافع کے تناسب پر مبنی ہدف کا استعمال کرتا ہے تاکہ مستحکم تجارتی کارکردگی حاصل کی جا سکے۔

حکمت عملی کا اصول

حکمت عملی کا بنیادی منطق تین سطحوں پر مشتمل ہے:

- بولنگر بینڈ بریک آؤٹ سگنل: بالائی اور نچلی پٹیوں کو وولٹیلیٹی چینل کے طور پر استعمال کرتے ہوئے، قیمت بالائی پٹی سے اوپر جانے پر خرید سگنل اور نچلی پٹی سے نیچے جانے پر فروخت سگنل سمجھا جاتا ہے۔

- RSI مومینٹم تصدیق: RSI 50 سے اوپر خرید مومینٹم کی تصدیق کرتا ہے اور 50 سے نیچے فروخت مومینٹم کی تصدیق کرتا ہے، بغیر رجحان کے تجارت سے بچتا ہے۔

- EMA رجحان فلٹر: 200 پیریڈ EMA مرکزی رجحان کا تعین کرنے کے لیے استعمال ہوتا ہے، اور صرف رجحان کی سمت میں پوزیشن کھولی جاتی ہے۔ قیمت EMA سے اوپر ہو تو خرید، نیچے ہو تو فروخت۔

تجارتی تصدیق کے لیے درکار شرائط:

- مسلسل دو کندل بریک آؤٹ حالت میں رہیں

- حجم 20 پیریڈ کی اوسط سے زیادہ ہو

- متحرک سٹاپ لاس ATR قدر پر مبنی ہو

- منافع کا ہدف 1.5 گنا خطرے سے منافع کے تناسب پر سیٹ ہو

حکمت عملی کے فوائد

- متعدد تکنیکی اشاروں کی مشترکہ فلٹرنگ سگنل کے معیار کو نمایاں طور پر بہتر بناتی ہے

- متحرک پوزیشن مینجمنٹ میکانزم مارکیٹ کے اتار چڑھاؤ کے مطابق خودکار طور پر ایڈجسٹ ہوتا ہے

- سخت تجارتی تصدیق کا طریقہ کار غلط سگنلز کو مؤثر طریقے سے کم کرتا ہے

- مکمل خطرے پر قابو پانے کا نظام، بشمول متحرک سٹاپ لاس اور مقررہ خطرے سے منافع کا تناسب

- لچکدار پیرامیٹر آپٹیمائزیشن کی گنجائش، مختلف مارکیٹ حالات کے مطابق ڈھل سکتی ہے

حکمت عملی کے خطرات

- پیرامیٹر کی زیادہ آپٹیمائزیشن overfitting کا سبب بن سکتی ہے

- انتہائی اتار چڑھاؤ والی مارکیٹ میں بار بار سٹاپ لاس لگ سکتا ہے

- اتار چڑھاؤ والی مارکیٹ میں مسلسل نقصان ہو سکتا ہے

- رجحان کے موڑ پر سگنل میں تاخیر ہو سکتی ہے

- تکنیکی اشاروں کے درمیان متضاد سگنل ظاہر ہو سکتے ہیں

خطرے پر قابو پانے کی تجاویز:

- سٹاپ لاس کے اصولوں پر سختی سے عمل کریں

- ہر تجارت میں خطرے کو محدود رکھیں

- باقاعدہ بیک ٹیسٹ کر کے پیرامیٹر کی کارکردگی کی تصدیق کریں

- بنیادی تجزیہ کو شامل کریں

- ضرورت سے زیادہ تجارت سے گریز کریں

حکمت عملی کی بہتری کے رجحانات

- مزید تکنیکی اشارے متعارف کروائیں تاکہ ایک دوسرے کی تصدیق ہو سکے

- خودکار پیرامیٹر آپٹیمائزیشن میکانزم تیار کریں

- مارکیٹ کے جذباتی اشارے شامل کریں

- تجارتی تصدیق کے میکانزم کو بہتر بنائیں

- زیادہ لچکدار پوزیشن مینجمنٹ سسٹم تیار کریں

بنیادی بہتری کے خیالات:

- مختلف مارکیٹ سائیکل کے مطابق پیرامیٹرز کو متحرک طور پر ایڈجسٹ کریں

- تجارتی فلٹرنگ کی شرائط میں اضافہ کریں

- خطرے سے منافع کے تناسب کی ترتیب کو بہتر بنائیں

- سٹاپ لاس میکانزم کو مکمل کریں

- زیادہ ذہین سگنل تصدیقی نظام تیار کریں

خلاصہ

یہ حکمت عملی بولنگر بینڈز، RSI اور EMA جیسے تکنیکی اشاروں کے مربوط امتزاج کے ذریعے ایک مکمل تجارتی نظام تشکیل دیتی ہے۔ یہ نظام تجارت کے معیار کو یقینی بنانے کے ساتھ ساتھ سخت خطرے پر قابو پانے اور لچکدار پیرامیٹر آپٹیمائزیشن کی گنجائش کے ذریعے مضبوط عملی اطلاق کی اہلیت ظاہر کرتا ہے۔ تجویز ہے کہ تاجر لائیو اکاؤنٹ میں پیرامیٹرز کو احتیاط سے تصدیق کریں، تجارتی اصولوں پر سختی سے عمل کریں اور حکمت عملی کی کارکردگی کو مسلسل بہتر بناتے رہیں۔

- 1