اوسط واپسی بولنگر بینڈ ڈالر لاگت اوسط سرمایہ کاری حکمت عملی

جائزہ

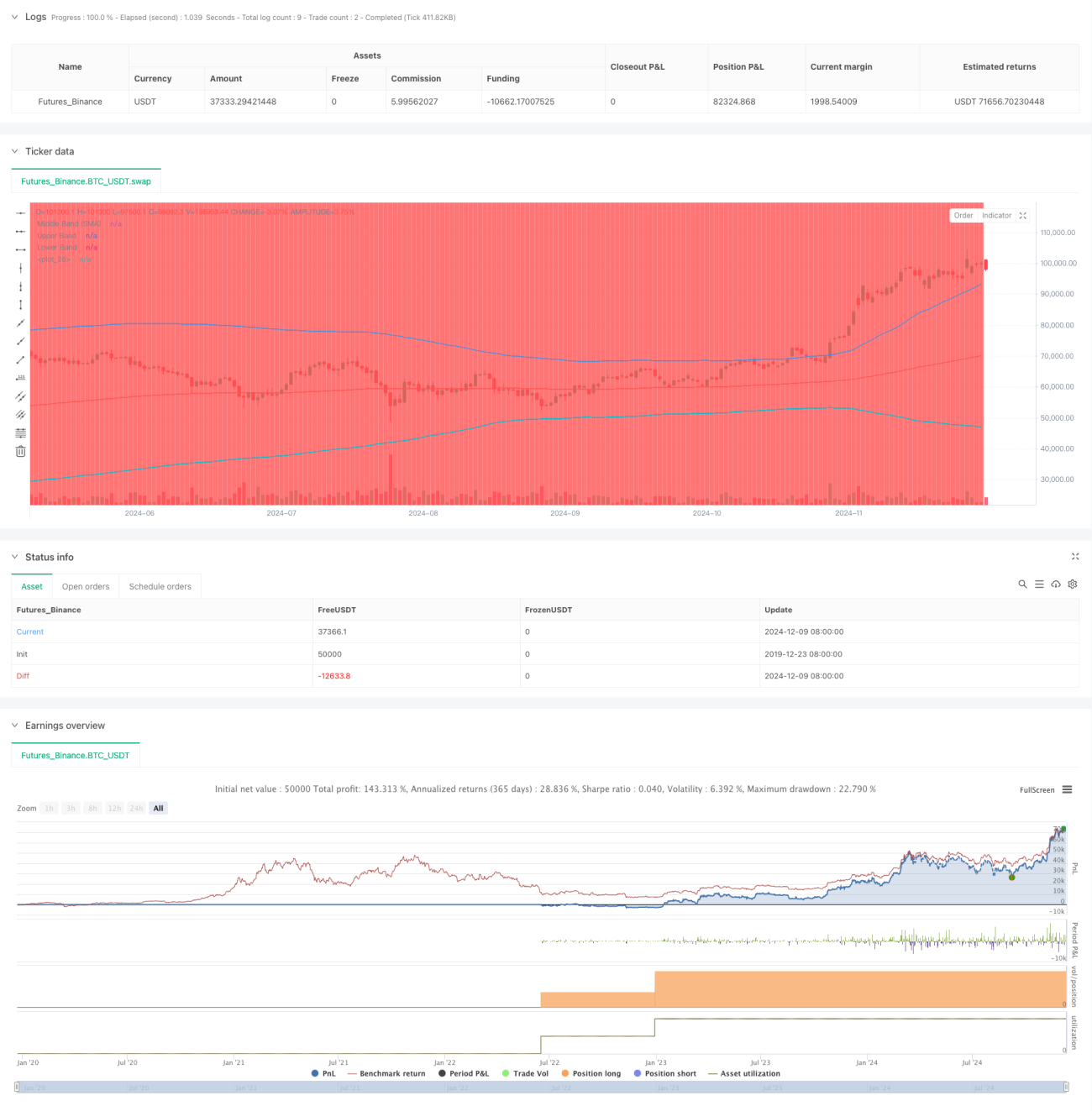

یہ حکمت عملی ڈالر لاگت اوسط (DCA) اور بولنگر بینڈز تکنیکی اشارے کو یکجا کرنے والی ایک ذہین سرمایہ کاری کی حکمت عملی ہے۔ یہ قیمت میں کمی کے دوران منظم طریقے سے پوزیشن بناتی ہے اور اوسط کی طرف واپسی (Mean Reversion) کے اصول کو استعمال کرتی ہے۔ اس حکمت عملی کا بنیادی مقصد یہ ہے کہ جب قیمت بولنگر بینڈ کے نچلے بینڈ سے نیچے آجائے تو ایک مقررہ رقم کی خریداری کی جائے، تاکہ مارکیٹ میں اصلاح کے دوران بہتر داخلے کی قیمت حاصل کی جا سکے۔

حکمت عملی کا اصول

اس حکمت عملی کا بنیادی اصول تین ستونوں پر مبنی ہے: 1) ڈالر لاگت اوسط، جس میں وقت کے ساتھ مقررہ رقم لگا کر مارکیٹ ٹائمنگ کے خطرے کو کم کیا جاتا ہے۔ 2) اوسط کی طرف واپسی کا نظریہ، جس کے مطابق قیمت آخر کار اپنی تاریخی اوسط پر واپس آجاتی ہے۔ 3) بولنگر بینڈز کا اشارہ، جو زیادہ خریدی یا زیادہ فروخت شدہ علاقوں کی نشاندہی کرتا ہے۔ جب قیمت بولنگر بینڈ کے نچلے بینڈ سے نیچے آتی ہے تو خریداری کا سگنل ملتا ہے، اور خریداری کی مقدار مقررہ سرمایہ کاری کی رقم کو موجودہ قیمت سے تقسیم کرکے متعین کی جاتی ہے۔ حکمت عملی 200-مدت کے ایکسپونینشل موونگ ایوریج کو بولنگر بینڈ کے درمیانی بینڈ کے طور پر استعمال کرتی ہے، جس میں معیاری انحراف کا ضریب 2 ہے، تاکہ اوپر اور نیچے کے بینڈز کی حد بندی کی جا سکے۔

حکمت عملی کے فوائد

- مارکیٹ ٹائمنگ کے خطرے میں کمی - منظم خریداری کے ذریعے انسانی غلطیوں کو کم کرنا

- اصلاح کے مواقع سے فائدہ اٹھانا - جب قیمت بہت زیادہ گر جائے تو خودکار خریداری کرنا

- لچکدار پیرامیٹر سیٹنگز - مختلف مارکیٹ حالات کے مطابق بولنگر بینڈز کے پیرامیٹرز اور سرمایہ کاری کی رقم کو ایڈجسٹ کرنا

- واضح اندراج اور خارج ہونے کے قوانین - تکنیکی اشاروں پر مبنی معروضی سگنلز

- خودکار عملدرآمد - انسانی مداخلت کے بغیر، جذباتی تجارت سے بچنا

حکمت عملی کے خطرات

- اوسط کی طرف واپسی کے ناکام ہونے کا خطرہ - ٹرینڈ والی مارکیٹ میں زیادہ جھوٹے سگنل پیدا ہو سکتے ہیں

- سرمائے کے انتظام کا خطرہ - مسلسل خریداری کے سگنلز کا سامنا کرنے کے لیے کافی سرمایہ رکھنا ضروری ہے

- پیرامیٹر آپٹیمائزیشن کا خطرہ - زیادہ آپٹیمائزیشن حکمت عملی کو ناکارہ بنا سکتی ہے

- مارکیٹ کے حالات پر انحصار - شدید اتار چڑھاؤ والی مارکیٹ میں کارکردگی خراب ہو سکتی ہے

ان خطرات کو سنبھالنے کے لیے سرمائے کے انتظام کے سخت قوانین اور حکمت عملی کی کارکردگی کا باقاعدہ جائزہ لینے کی سفارش کی جاتی ہے۔

حکمت عملی کی بہتری کے مواقع

- ٹرینڈ فلٹر کا اضافہ، مضبوط ٹرینڈ میں مخالف سمت میں تجارت سے بچنا

- متعدد وقتی فریموں کی تصدیق کا طریقہ کار شامل کرنا

- سرمائے کے انتظام کے نظام کو بہتر بنانا، اتار چڑھاؤ کی بنیاد پر سرمایہ کاری کی رقم کو متحرک طور پر ایڈجسٹ کرنا

- منافع حاصل کرنے کا طریقہ کار شامل کرنا، جب قیمت اوسط پر واپس آجائے تو منافع وصول کرنا

- دیگر تکنیکی اشارے کے ساتھ ملا کر سگنلز کی وشوسنییتا کو بہتر بنانا

خلاصہ

یہ ایک مضبوط حکمت عملی ہے جو تکنیکی تجزیہ کو منظم سرمایہ کاری کے طریقہ کار کے ساتھ جوڑتی ہے۔ بولنگر بینڈز کے ذریعے زیادہ فروخت شدہ مواقع کی نشاندہی کی جاتی ہے اور ڈالر لاگت اوسط کے ذریعے خطرہ کم کیا جاتا ہے۔ حکمت عملی کی کامیابی کا انحصار پیرامیٹرز کی مناسب ترتیب اور عملدرآمد کے سخت نظم و ضبط پر ہے۔ اگرچہ اس میں کچھ خطرات موجود ہیں، لیکن مسلسل بہتری اور خطرے کے انتظام کے ذریعے حکمت عملی کے استحکام کو بڑھایا جا سکتا ہے۔

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("DCA Strategy with Mean Reversion and Bollinger Band", overlay=true) // Define the strategy name and set overlay=true to display on the main chart

// Inputs for investment amount and dates- 1