متعدد توازن قیمت کے رجحان کی پیروی اور الٹی تجارتی حکمت عملی

حکمت عملی کا خلاصہ

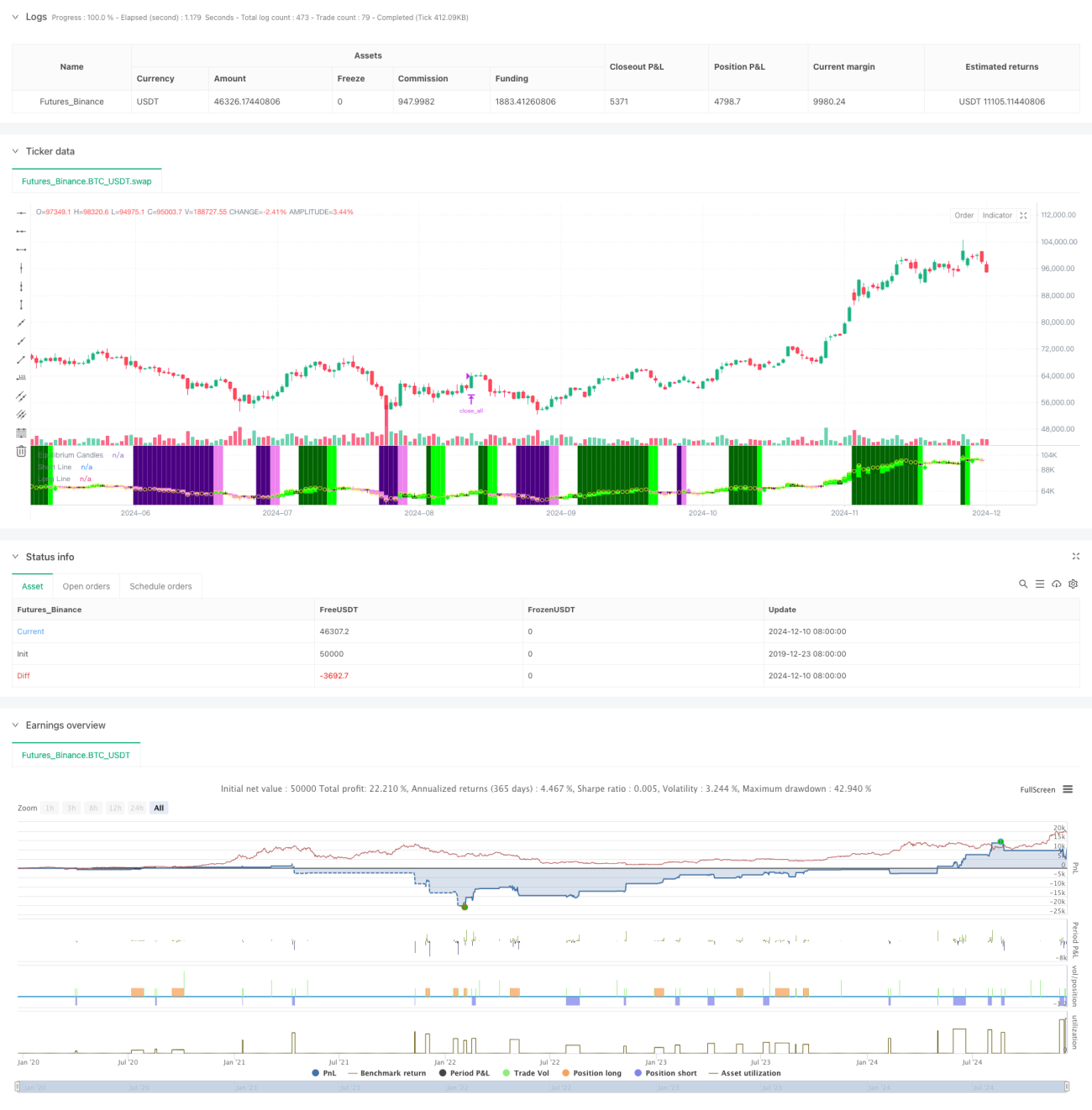

یہ حکمت عملی قیمت کے توازن کے نقطہ پر مبنی ایک رجحان کی پیروی اور ریورسل ٹریڈنگ سسٹم ہے۔ یہ پچھلی X کندوں کی اونچائی اور نیچائی کے درمیانی نقطہ کا حساب لگا کر توازن کی قیمت کا تعین کرتی ہے، اور اختتامی قیمت کے توازن کی قیمت کے مقابلے میں پوزیشن کی بنیاد پر رجحان کی سمت کا فیصلہ کرتی ہے۔ جب قیمت توازن کی قیمت کے ایک طرف متعین کندوں کی تعداد تک مسلسل برقرار رہتی ہے، تو نظام رجحان کو تسلیم کرتا ہے۔ پہلی واپسی پر (قیمت توازن کی قیمت کو توڑتی ہے) نظام داخلے کا موقع تلاش کرتا ہے۔ یہ حکمت عملی ترتیبات کے مطابق رجحان کی پیروی یا ریورسل ٹریڈنگ موڈ کا انتخاب کر سکتی ہے۔

حکمت عملی کا اصول

- توازن کی قیمت کا حساب: پچھلی X کندوں کی سب سے اونچی اور سب سے نیچی قیمت کے درمیانی نقطہ کو توازن کی قیمت کے طور پر استعمال کیا جاتا ہے، جو اکیلے توازن چارٹ کی بیس لائن کے حساب کے طریقہ کار سے ملتا ہے۔

- رجحان کا فیصلہ: جب قیمت توازن کی قیمت کے ایک ہی طرف مسلسل X کندوں (بطور ڈیفالٹ 7) تک رہتی ہے، تو رجحان قائم سمجھا جاتا ہے۔

- داخلے کا سگنل: رجحان قائم ہونے کے بعد پہلی واپسی (قیمت کا توازن کی قیمت کو توڑنا) پر داخلے کا سگنل متحرک ہوتا ہے۔

- نقصان روکنے اور منافع لینے کا تعین: ATR کے 60% کوانٹائل کا استعمال کرتے ہوئے نقصان روکنے اور منافع لینے کے فاصلے کو متحرک طور پر ایڈجسٹ کیا جاتا ہے، جو خطرے پر قابو پانے میں لچک فراہم کرتا ہے۔

- بڑی اتار چڑھاؤ سے تحفظ: جب قیمت توازن کے نقطہ سے متعین ATR اوقات سے زیادہ ہٹ جاتی ہے، تو نظام بڑی واپسی سے بچنے کے لیے خود بخود پوزیشن بند کر دیتا ہے۔

حکمت عملی کے فوائد

- موافقت: مارکیٹ کی خصوصیات کے مطابق رجحان کی پیروی اور ریورسل ٹریڈنگ کے موڈز کے درمیان لچکدار طریقے سے سوئچ کر سکتی ہے۔

- خطرے کا مکمل کنٹرول: متحرک ATR پر مبنی نقصان روکنے کا استعمال کرتی ہے اور بڑی اتار چڑھاؤ سے تحفظ کا طریقہ کار رکھتی ہے۔

- واضح آپریشن: ٹریڈنگ سگنلز واضح ہیں اور پیچیدہ تکنیکی اشاریوں کے مجموعے پر انحصار نہیں کرتے۔

- بہتر بصری اثر: رنگین کندوں اور پس منظر کا استعمال کرتے ہوئے مارکیٹ کی حالت کا فوری بصری منظر پیش کرتی ہے۔

- خودکار نظاموں کے لیے موزوں: MT5 جیسے ٹریڈنگ پلیٹ فارمز سے آسانی سے جوڑا جا سکتا ہے تاکہ خودکار ٹریڈنگ کی جا سکے۔

حکمت عملی کے خطرات

- سائیڈ وے مارکیٹ کا خطرہ: سائیڈ وے مارکیٹ میں بار بار غلط سگنل پیدا ہو سکتے ہیں۔

- سلپج کا اثر: شدید اتار چڑھاؤ پر بڑی سلپج کا سامنا ہو سکتا ہے۔

- پیرامیٹرز کی حساسیت: بنیادی پیرامیٹرز جیسے توازن کا دورانیہ، رجحان کا فیصلہ کرنے کا دورانیہ وغیرہ کو مختلف مارکیٹوں کے لیے احتیاط سے بہتر بنایا جانا چاہیے۔

- مارکیٹ کی تبدیلی کا خطرہ: جب مارکیٹ رجحان سے سائیڈ وے میں تبدیل ہوتی ہے، تو بڑی واپسی ہو سکتی ہے۔

حکمت عملی کو بہتر بنانے کی سمتیں

- مارکیٹ کے ماحول کی شناخت: مارکیٹ کے ماحول کا تعین کرنے والا ماڈیول شامل کریں تاکہ مختلف مارکیٹ حالات میں حکمت عملی کے پیرامیٹرز کو متحرک طور پر ایڈجسٹ کیا جا سکے۔

- سگنل فلٹریشن: غلط سگنلز کو فلٹر کرنے کے لیے والیوم، اتار چڑھاؤ وغیرہ جیسے معاون اشاریوں کو شامل کرنے پر غور کریں۔

- پوزیشن مینجمنٹ: زیادہ پیچیدہ پوزیشن مینجمنٹ میکانزم متعارف کروائیں، جیسے اتار چڑھاؤ پر مبنی متحرک ایڈجسٹمنٹ۔

- متعدد ٹائم فریم: مختلف ٹائم فریموں کے سگنلز کو یکجا کر کے ٹریڈنگ کی درستگی میں اضافہ کریں۔

- ٹریڈنگ لاگت کی بہتری: مختلف ٹریڈنگ مصنوعات کی لاگت کی خصوصیات کے مطابق داخلے اور اخراج کے اوقات کو بہتر بنائیں۔

خلاصہ

یہ ایک معقول طریقے سے ڈیزائن کیا گیا رجحان ٹریڈنگ سسٹم ہے جو توازن کی قیمت کے بنیادی تصور کے ذریعے واضح ٹریڈنگ منطق فراہم کرتا ہے۔ اس حکمت عملی کی سب سے بڑی خصوصیت اس کی لچک ہے، جو نہ صرف رجحان کی پیروی کے لیے بلکہ ریورسل ٹریڈنگ کے لیے بھی استعمال کی جا سکتی ہے، اور اس میں خطرے پر قابو پانے کا مکمل طریقہ کار موجود ہے۔ اگرچہ کچھ مارکیٹ حالات میں اسے چیلنجز کا سامنا ہو سکتا ہے، لیکن مسلسل بہتری اور لچکدار ایڈجسٹمنٹ کے ذریعے، یہ حکمت عملی مختلف مارکیٹ ماحول میں مستحکم کارکردگی دکھانے کی امید رکھتی ہے۔

- 1