مقداری تجارت کے سگنلز کی پیروی اور متنوع اخراج کی حکمت عملیوں کے بہتری کا نظام

جائزہ

یہ حکمت عملی LuxAlgo® سگنلز اور اوورلے انڈیکیٹرز پر مبنی ایک مقداری تجارتی نظام ہے۔ یہ بنیادی طور پر کسٹم الرٹ کی شرائط کو پکڑ کر لمبی پوزیشنیں کھولتا ہے اور متعدد ایگزٹ سگنلز کے ذریعے پوزیشنوں کا انتظام کرتا ہے۔ یہ نظام ماڈیولر ڈیزائن پر مبنی ہے جو مختلف ایگزٹ شرائط کے مجموعے کو سپورٹ کرتا ہے، بشمول ذہین ٹریلنگ سٹاپ لاس، رجحان کی تبدیلی کی تصدیق، اور روایتی فیصد پر مبنی سٹاپ لاس۔ اس کے علاوہ، یہ نظام موجودہ پوزیشنوں میں اضافہ (ایڈان) کرنے کی بھی اجازت دیتا ہے، جو سرمایہ کے انتظام میں زیادہ لچک فراہم کرتا ہے۔

حکمت عملی کا اصول

حکمت عملی کا بنیادی منطق درج ذیل اہم حصوں پر مشتمل ہے:

- اندراج سگنل سسٹم: کسٹم LuxAlgo® الرٹ شرائط کے ذریعے لمبی پوزیشن کے اندراج کے سگنل کو متحرک کرتا ہے۔

- اضافہ کا انتظام: اختیاری طور پر موجودہ پوزیشنوں میں اضافہ کرنے کی فعالیت کو فعال کیا جا سکتا ہے۔

- کثیر سطحی ایگزٹ میکانزم:

- ذہین ٹریلنگ سٹاپ لاس: قیمت اور ذہین ٹریلنگ لائن کے درمیان تعلق کی نگرانی

- رجحان کی تصدیق پر ایگزٹ: بنیادی اور بہتر (ایڈوانسڈ) شارٹ کنفرمیشن سگنلز شامل ہیں

- بلٹ ان ایگزٹ سگنلز: انڈیکیٹر کے مختلف ایگزٹ شرائط کا استعمال

- روایتی سٹاپ لاس: فیصد پر مبنی مقررہ سٹاپ لاس کی حمایت

- ٹائم ونڈو کا انتظام: بیک ٹیسٹنگ کے لئے لچکدار تاریخ کی حدود طے کرنے کی سہولت۔

حکمت عملی کے فوائد

- نظامی رسک مینجمنٹ: کثیر سطحی ایگزٹ میکانزم کے ذریعے مندی کے خطرے کو مؤثر طریقے سے کنٹرول کرنا۔

- لچکدار پوزیشن مینجمنٹ: مختلف اضافہ اور کمی کی حکمت عملیوں کی حمایت، بازار کی صورتحال کے مطابق متحرک ایڈجسٹمنٹ۔

- اعلیٰ حسب ضرورت: صارفین مختلف ایگزٹ شرائط کو آزادانہ طور پر جوڑ سکتے ہیں اور ذاتی تجارتی نظام تشکیل دے سکتے ہیں۔

- ماڈیولر ڈیزائن: ہر فعالیت کا ماڈیول نسبتاً آزاد ہے، جس سے دیکھ بھال اور بہتری آسان ہوتی ہے۔

- مکمل بیک ٹیسٹنگ سپورٹ: تفصیلی بیک ٹیسٹنگ پیرامیٹرز کی ترتیب فراہم کرتا ہے، تاریخی ڈیٹا کی تصدیق کی اجازت دیتا ہے۔

حکمت عملی کے خطرات

- سگنل پر انحصار کا خطرہ: حکمت عملی LuxAlgo® انڈیکیٹر کے سگنل کے معیار پر بہت زیادہ انحصار کرتی ہے۔

- بازار کے ماحول کے مطابق ڈھلنے کا خطرہ: مختلف بازار کے ماحول میں حکمت عملی کی کارکردگی میں بڑا فرق ہو سکتا ہے۔

- پیرامیٹر کی حساسیت کا خطرہ: متعدد ایگزٹ شرائط کا مجموعہ قبل از وقت ایگزٹ یا مواقع سے محروم ہونے کا سبب بن سکتا ہے۔

- لیکویڈیٹی کا خطرہ: ناکافی لیکویڈیٹی کی صورت میں، اندراج اور خارج ہونے کے عمل متاثر ہو سکتے ہیں۔

- تکنیکی نفاذ کا خطرہ: انڈیکیٹر اور حکمت عملی کے مستحکم آپریشن کو یقینی بنانا، تکنیکی خرابیوں سے بچنا ضروری ہے۔

حکمت عملی کی بہتری کے امکانات

- سگنل سسٹم کی بہتری:

- مزید تکنیکی انڈیکیٹرز کو سگنل کی تصدیق کے لئے شامل کرنا

- انکولی سگنل حد (تھریشولڈ) ایڈجسٹمنٹ میکانزم تیار کرنا

- خطرے کے کنٹرول میں اضافہ:

- والیٹیلیٹی کے مطابق ڈھلنے والے سٹاپ لاس میکانزم کا اضافہ

- متحرک پوزیشن سائزنگ سسٹم تیار کرنا

- کارکردگی کی بہتری:

- حساب کی کارکردگی کو بہتر بنانا، وسائل کی کھپت کو کم کرنا

- سگنل پروسیسنگ منطق کو بہتر بنانا، تاخیر کو کم کرنا

- فعالیت میں توسیع:

- مزید مارکیٹ ماحول کے تجزیے کے اوزار شامل کرنا

- زیادہ لچکدار پیرامیٹر آپٹیمائزیشن فریم ورک تیار کرنا

خلاصہ

یہ حکمت عملی LuxAlgo® کے اعلیٰ معیار کے سگنلز اور کثیر سطحی رسک مینجمنٹ سسٹم کو ملا کر مقداری تجارت کے لئے ایک مکمل حل فراہم کرتی ہے۔ اس کا ماڈیولر ڈیزائن اور لچکدار ترتیب کے اختیارات اسے بہترین موافقت اور توسیع پذیری فراہم کرتے ہیں۔ اگرچہ کچھ موروثی خطرات موجود ہیں، لیکن مسلسل بہتری اور تطہیر کے ذریعے حکمت عملی کی مجموعی کارکردگی میں مزید بہتری کی گنجائش ہے۔ مشورہ ہے کہ صارفین عملی استعمال میں بازار کے ماحول کی تبدیلیوں پر نظر رکھیں، مناسب وقت پر پیرامیٹرز کو ایڈجسٹ کریں، اور خطرے کی مسلسل نگرانی جاری رکھیں۔

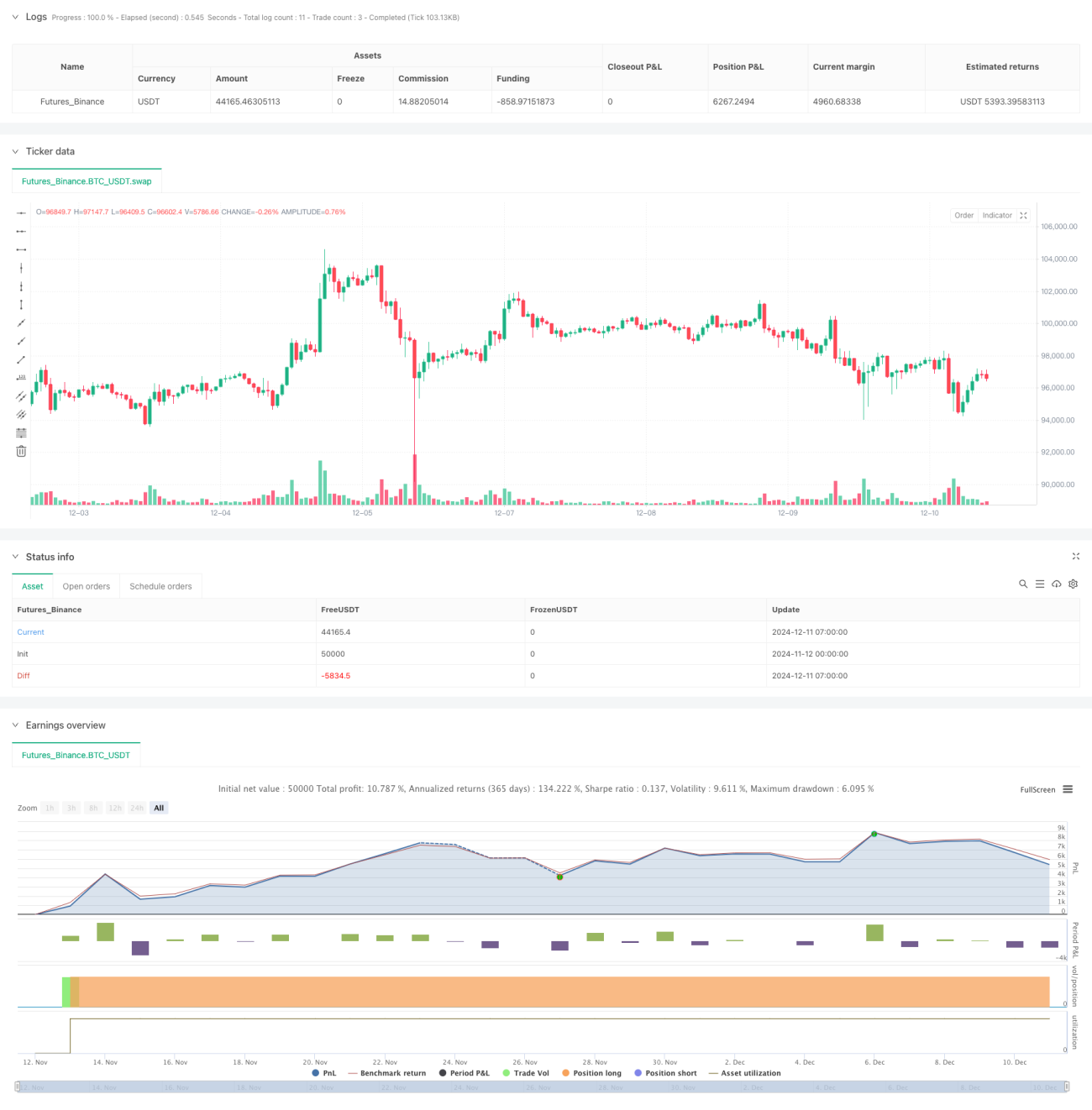

/*backtest

start: 2024-11-12 00:00:00

end: 2024-12-11 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Chart0bserver

// This strategy is NOT from the LuxAlgo® developers. We created this to compliment their hard work. No association with LuxAlgo® is intended nor implied.

- 1