متعدد ٹائم فریم ٹرینڈ فالونگ اور ATR پرافٹ ٹیک اینڈ سٹاپ لاس حکمت عملی

خلاصہ

یہ ایک ٹرینڈ فالو کرنے والی تجارتی حکمت عملی ہے جو UT Bot اور 50-دورانیہ ایکسپونینشل مووینگ ایوریج (EMA) کو یکجا کرتی ہے۔ یہ حکمت عملی بنیادی طور پر 1 منٹ کے ٹائم فریم پر مختصر مدت کی تجارت کرتی ہے، جبکہ 5 منٹ کے ٹائم فریم کی ٹرینڈ لائن کو سمت کے فلٹر کے طور پر استعمال کرتی ہے۔ حکمت عملی ATR انڈیکیٹر کے ذریعے سٹاپ لاس کی متحرک پوزیشن کا حساب لگاتی ہے، اور منافع کو بہتر بنانے کے لیے دوہرے ٹیک پرافٹ اہداف مقرر کرتی ہے۔

حکمت عملی کا اصول

حکمت عملی کا بنیادی منطق درج ذیل کلیدی اجزاء پر مبنی ہے:

- UT Bot کا استعمال کرتے ہوئے متحرک سپورٹ اور ریزسٹنس لیولز کا حساب لگانا

- 5 منٹ کے ٹائم فریم پر 50-دورانیہ EMA کے ذریعے مجموعی رجحان کی سمت کا تعین کرنا

- 21-دورانیہ EMA اور UT Bot کے سگنلز کو ملا کر داخلی نقطہ کا تعین کرنا

- ATR کے ضربوں کے ذریعے متحرک ٹریلنگ سٹاپ لاس سیٹ کرنا

- 0.5% اور 1% کے دو ٹیک پرافٹ اہداف مقرر کرنا، جن پر بالترتیب 50% پوزیشن بند کی جاتی ہے

جب قیمت UT Bot کے حساب کردہ سپورٹ/ریزسٹنس لیول کو توڑتی ہے، اور 21-دورانیہ EMA UT Bot سے کراس اوور کرتی ہے، اور اس وقت قیمت 5 منٹ کی 50-دورانیہ EMA کی صحیح سمت میں ہوتی ہے، تو تجارتی سگنل متحرک ہوتا ہے۔

حکمت عملی کے فوائد

- متعدد ٹائم فریموں کا امتزاج تجارت کی قابل اعتمادی کو بڑھاتا ہے

- متحرک ATR سٹاپ لاس مارکیٹ کے اتار چڑھاؤ کے مطابق خود بخود ایڈجسٹ ہو سکتا ہے

- دوہرے ٹیک پرافٹ اہداف منافع اور جیت کی شرح میں توازن قائم کرتے ہیں

- ہیکین آشی کینڈلز کا استعمال کچھ جھوٹے بریک آؤٹ کو فلٹر کر سکتا ہے

- تجارت کی سمت کے انتخاب میں لچک (صرف لانگ، صرف شارٹ، یا دونوں طرف تجارت)

حکمت عملی کے خطرات

- مختصر مدت کی تجارت میں اسپریڈ اور کمیشن کی زیادہ لاگت ہو سکتی ہے

- سائیڈ ویز مارکیٹ میں بار بار جھوٹے سگنل پیدا ہو سکتے ہیں

- متعدد شرائط کی پابندی کچھ ممکنہ تجارتی مواقع سے محروم کر سکتی ہے

- ATR پیرامیٹرز کو مختلف مارکیٹوں کے لیے بہتر بنانے کی ضرورت ہے

حکمت عملی کی بہتری کے لائحہ عمل

- والیوم انڈیکیٹر کو معاون تصدیق کے طور پر شامل کیا جا سکتا ہے

- مارکیٹ کے مزاج کے مزید انڈیکیٹرز متعارف کرانے پر غور کیا جا سکتا ہے

- مختلف مارکیٹوں کے اتار چڑھاؤ کی خصوصیات کے مطابق خودکار پیرامیٹرز تیار کرنا

- تجارتی وقت کی حد بندی کا فلٹر شامل کرنا

- زیادہ ذہین پوزیشن مینجمنٹ سسٹم تیار کرنا

خلاصہ

یہ حکمت عملی متعدد تکنیکی انڈیکیٹرز اور ٹائم فریموں کو یکجا کر کے ایک مکمل تجارتی نظام تشکیل دیتی ہے۔ اس میں نہ صرف داخلی اور خارجی شرائط واضح ہیں بلکہ رسک مینجمنٹ کا ایک جامع طریقہ کار بھی موجود ہے۔ اگرچہ عملی استعمال میں مخصوص مارکیٹ کے حالات کے مطابق پیرامیٹرز کو بہتر بنانے کی ضرورت ہو سکتی ہے، لیکن مجموعی فریم ورک اچھی عملیت اور توسیع پذیری رکھتا ہے۔

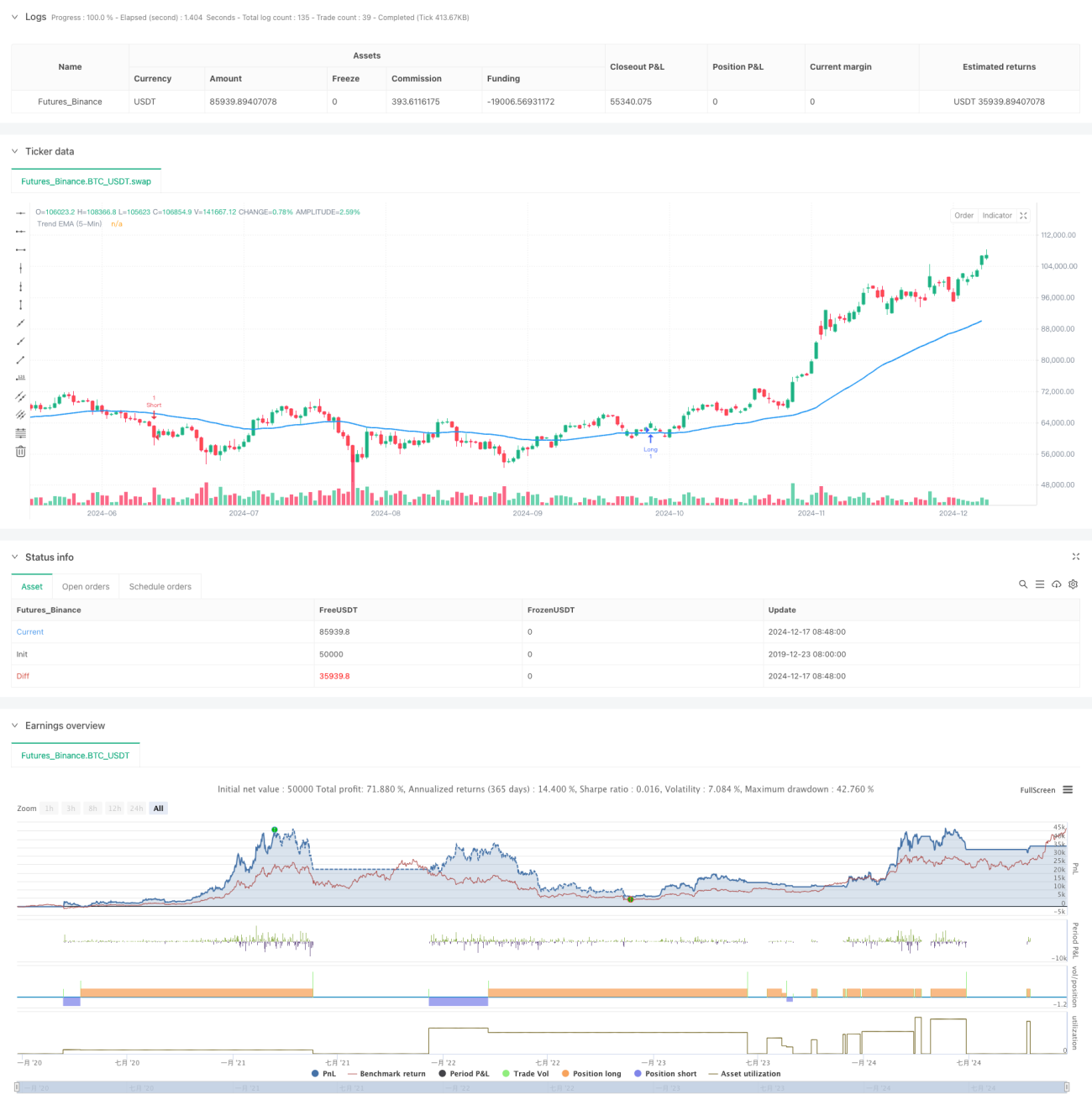

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//Created by Nasser mahmoodsani' all rights reserved

// E-mail : [email protected]

- 1