متعدد موونگ اوسط کراس اوور کے ساتھ مل کر Camarilla سپورٹ اور ریزسٹنس ٹرینڈ ٹریڈنگ سسٹم

جائزہ

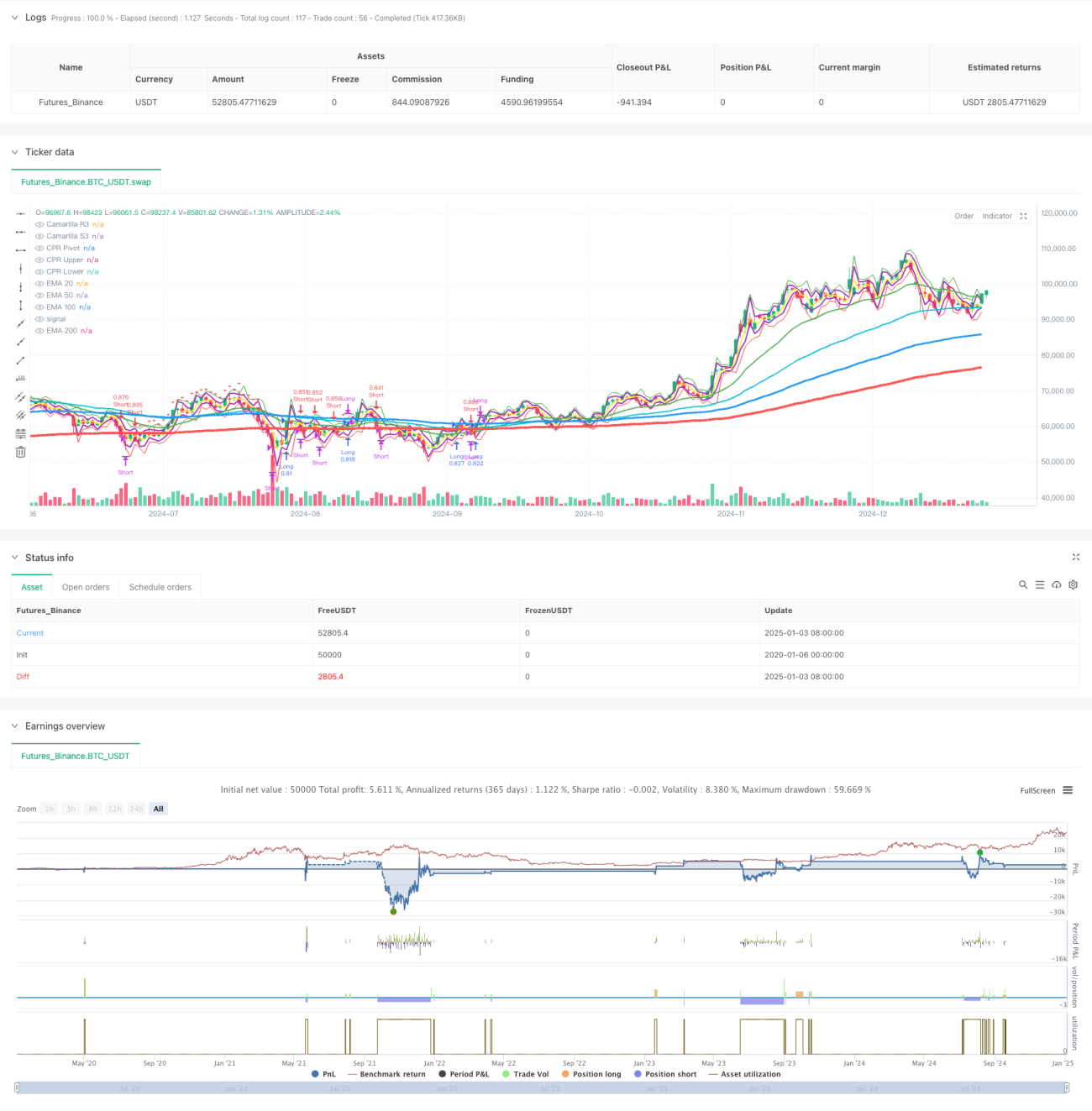

یہ حکمت عملی متعدد ایکسپونینشل موونگ اوسط (EMA)، کاماریلا سپورٹ اور ریزسٹنس لیولز، اور سینٹرل پوائنٹ رینج (CPR) پر مبنی ایک ٹرینڈ فالونگ ٹریڈنگ سسٹم ہے۔ یہ حکمت عملی قیمت اور متعدد اوسط کے رشتے کے ساتھ ساتھ اہم قیمتوں کے زون کا تجزیہ کرکے مارکیٹ کے رجحان اور ممکنہ تجارتی مواقع کی نشاندہی کرتی ہے۔ اس نظام میں سخت سرمائے کا انتظام اور رسک کنٹرول کے اقدامات شامل ہیں، بشمول فیصدی پوزیشن سائز اور متنوع خارجی طریقہ کار۔

حکمت عملی کا اصول

یہ حکمت عملی بنیادی طور پر درج ذیل اہم اجزاء پر مبنی ہے:

- ایک سے زیادہ اوسط کا نظام (EMA20/50/100/200) رجحان کی سمت اور طاقت کی تصدیق کے لیے

- کاماریلا سپورٹ اور ریزسٹنس لیولز (R3/S3) اہم قیمتی سطحوں کی نشاندہی کے لیے

- سینٹرل پوائنٹ رینج (CPR) دن کی تجارتی حد کا تعین کرنے کے لیے

- اندراج کا سگنل قیمت اور EMA200 کے کراس اوور اور EMA20 کی تصدیق پر مبنی ہے

- خارجی حکمت عملی میں دو طریقے شامل ہیں: مقررہ پوائنٹس اور فیصدی حرکت

- سرمایہ انتظامی نظام اکاؤنٹ کے سائز کے مطابق پوزیشن کے سائز کو متحرک طور پر ایڈجسٹ کرتا ہے

حکمت عملی کے فوائد

- متعدد جہتی تکنیکی اشاریوں کا امتزاج زیادہ قابل اعتماد تجارتی سگنل فراہم کرتا ہے

- لچکدار خارجی میکانزم مختلف مارکیٹ ماحول کے مطابق ڈھل جاتا ہے

- مکمل سرمایہ انتظامی نظام مؤثر طریقے سے رسک کو کنٹرول کرتا ہے

- ٹرینڈ فالونگ خصوصیات بڑی حرکتوں کو پکڑنے میں مدد دیتی ہیں

- بصری اجزاء تاجروں کو مارکیٹ کے ڈھانچے کو سمجھنے میں آسانی فراہم کرتے ہیں

حکمت عملی کے خطرات

- اوسیلیٹنگ مارکیٹ میں جھوٹے سگنل پیدا ہو سکتے ہیں

- متعدد اشاریوں کی وجہ سے تجارتی سگنل میں تاخیر ہو سکتی ہے

- مقررہ خارجی پوائنٹس زیادہ وولیٹیلیٹی والی مارکیٹ میں کم کارگر ثابت ہو سکتے ہیں

- ڈرا ڈاؤن برداشت کرنے کے لیے بڑے سرمائے کی ضرورت ہے

- تجارتی اخراجات مجموعی منافع کو متاثر کر سکتے ہیں

حکمت عملی کی بہتری کے امکانات

- وولیٹیلیٹی انڈیکیٹر متعارف کرکے اندراج اور خارجی پیرامیٹرز کو متحرک طور پر ایڈجسٹ کریں

- مارکیٹ کی حالت کی شناخت کا ماڈیول شامل کریں تاکہ مختلف مارکیٹ ماحول کے مطابق ڈھل سکے

- سرمایہ انتظامی نظام کو بہتر بنائیں اور متحرک پوزیشن مینجمنٹ شامل کریں

- سگنل کے معیار کو بہتر بنانے کے لیے تجارتی وقت کا فلٹر شامل کریں

- سگنل کی وشوسنییتا بڑھانے کے لیے والیوم تجزیہ شامل کرنے پر غور کریں

خلاصہ

یہ حکمت عملی متعدد کلاسیکی تکنیکی تجزیہ ٹولز کو یکجا کرکے ایک مکمل تجارتی نظام تشکیل دیتی ہے۔ اس نظام کی خوبی مختلف جہتوں میں مارکیٹ کا تجزیہ اور سخت رسک مینجمنٹ ہے، لیکن ساتھ ہی مارکیٹ کے مختلف ماحول کے مطابق ڈھلنے کی ضرورت کو بھی مدنظر رکھنا چاہیے۔ مسلسل بہتری اور ترمیم کے ذریعے، یہ حکمت عملی استحکام برقرار رکھتے ہوئے منافع بخشی بڑھانے کی صلاحیت رکھتی ہے۔

- 1