دو مووونگ ایوریجز کے کراس اوور پر مبنی متحرک رجحان کی پیروی کی مقداری تجارتی حکمت عملی

جائزہ

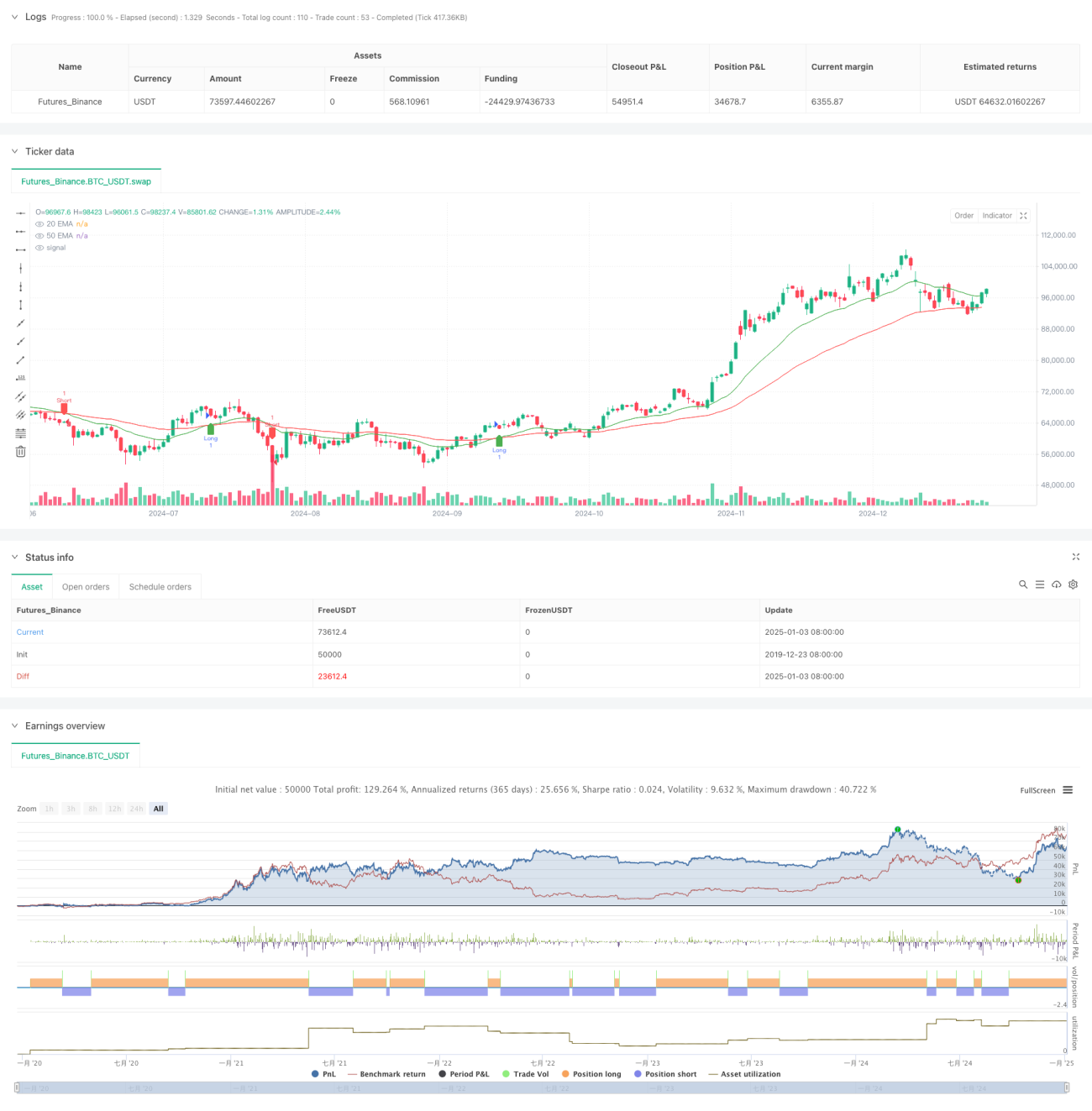

یہ حکمت عملی دو متحرک اوسطوں کے کراس اوور سگنل پر مبنی ایک متحرک رجحان کی پیروی کا نظام ہے۔ یہ مختصر مدت کے 20 دن کے ایکسپونینشل مووینگ ایوریج (EMA) اور طویل مدت کے 50 دن کے ایکسپونینشل مووینگ ایوریج (EMA) کے درمیان کراس اوور کے ذریعے مارکیٹ کے رجحان میں تبدیلی کی نشاندہی کرتا ہے اور خود بخود خرید و فروخت کے عمل کو انجام دیتا ہے۔ یہ حکمت عملی ایک پختہ تکنیکی تجزیہ کے طریقے کو استعمال کرتی ہے، جس میں رجحان کی پیروی اور متحرک پوزیشن مینجمنٹ کی خصوصیات شامل ہیں، اور یہ زیادہ اتار چڑھاؤ والے مارکیٹ ماحول کے لیے موزوں ہے۔

حکمت عملی کا اصول

حکمت عملی کا بنیادی منطق درج ذیل کلیدی عناصر پر مبنی ہے:

- 20 دن اور 50 دن کی دو مختلف ادوار کی ایکسپونینشل مووینگ ایوریج (EMA) کو رجحان کے تعین کے اشارے کے طور پر استعمال کرنا

- جب مختصر مدت کا 20 دن کا EMA طویل مدت کے 50 دن کے EMA کو اوپر سے عبور کرتا ہے تو نظام لانگ سگنل پیدا کرتا ہے

- جب مختصر مدت کا 20 دن کا EMA طویل مدت کے 50 دن کے EMA کو نیچے سے عبور کرتا ہے تو نظام شارٹ سگنل پیدا کرتا ہے

- position متغیر کے ذریعے پوزیشن کی حالت کو متحرک طور پر ٹریک کرنا، تاکہ پوزیشن مینجمنٹ کی درستگی یقینی بنائی جا سکے

- کراس اوور سگنل ظاہر ہونے پر، نظام خود بخود موجودہ پوزیشن کو بند کر کے نئی پوزیشن قائم کرتا ہے

حکمت عملی کے فوائد

- سگنل کی وضاحت: متحرک اوسط کراس اوور پر مبنی سگنل کا تعین کرنے کا طریقہ کار سادہ اور واضح ہے، جس سے جھوٹے سگنلز پیدا ہونے کا امکان کم ہے

- رسک کنٹرول کا مکمل نظام: متحرک پوزیشن مینجمنٹ میکانزم کا استعمال، جو مارکیٹ کی تبدیلیوں کا بروقت جواب دے سکتا ہے

- وسیع موافقت: یہ حکمت عملی مختلف مارکیٹ ماحول اور تجارتی اشیاء پر لاگو کی جا سکتی ہے

- اعلیٰ عمل درآمد کی کارکردگی: پروگرامیٹک ٹریڈنگ سگنل پیدا ہونے کے بعد فوری عمل درآمد کو یقینی بناتی ہے

- بیک ٹیسٹنگ کی سہولت: اس میں ایک مکمل بیک ٹیسٹنگ فریم ورک شامل ہے، جو حکمت عملی کی اصلاح اور توثیق میں آسانی فراہم کرتا ہے

حکمت عملی کے خطرات

- سائیڈ ویز مارکیٹ کا خطرہ: سائیڈ ویز یا رینج باؤنڈ مارکیٹ میں بار بار جھوٹے بریک آؤٹ سگنلز پیدا ہو سکتے ہیں

- سلپیج کا خطرہ: مارکیٹ میں شدید اتار چڑھاؤ کے دوران بڑے ٹریڈنگ سلپیج کا سامنا ہو سکتا ہے

- تاخیر کا خطرہ: EMA اشاریہ فطری طور پر کچھ تاخیر رکھتا ہے، جس کی وجہ سے داخلے کے پوائنٹس مثالی نہیں ہو سکتے

- سرمایہ کے انتظام کا خطرہ: حکمت عملی میں سٹاپ لاس اور سرمایہ کے انتظام کا کوئی طریقہ کار شامل نہیں ہے، جسے اضافی طور پر بہتر کرنے کی ضرورت ہے

- نظامی خطرہ: مارکیٹ میں شدید اتار چڑھاؤ کے دوران نظامی خطرے کا سامنا ہو سکتا ہے

حکمت عملی کی بہتری کے امکانات

- اتار چڑھاؤ کے فلٹر کا تعارف، تاکہ سائیڈ ویز مارکیٹ میں جھوٹے سگنلز کو کم کیا جا سکے

- انکولی سٹاپ لاس اور ٹیک پرافٹ میکانزم کا اضافہ، تاکہ سرمایہ کی حفاظت بہتر ہو سکے

- متحرک اوسط کی مدت کے پیرامیٹرز کو بہتر بنانا، تاکہ وہ مختلف مارکیٹ ماحول میں بہتر طور پر ڈھل سکیں

- والیوم کی تصدیق کے طریقہ کار کا اضافہ، تاکہ سگنل کی قابل اعتمادی بہتر ہو

- متحرک پوزیشن سائزنگ کا نظام متعارف کرانا، تاکہ سرمایہ کے استعمال کی کارکردگی بہتر ہو سکے

خلاصہ

یہ حکمت عملی ایک کلاسک ٹرینڈ فالونگ سسٹم کا جدید نفاذ ہے۔ پروگرامیٹک ٹریڈنگ کے ذریعے روایتی ڈبل مووینگ ایوریج کراس اوور حکمت عملی کو منظم اور معیاری بنایا گیا ہے۔ اگرچہ اس میں کچھ موروثی خطرات موجود ہیں، لیکن مسلسل بہتری اور اصلاح کے ذریعے اس حکمت عملی میں اچھے استعمال کے امکانات ہیں۔ لائیو ٹریڈنگ میں استعمال کرنے سے پہلے پیرامیٹرز کی مکمل اصلاح اور بیک ٹیسٹنگ کی توثیق کرنے کی سفارش کی جاتی ہے۔

- 1