جائزہ

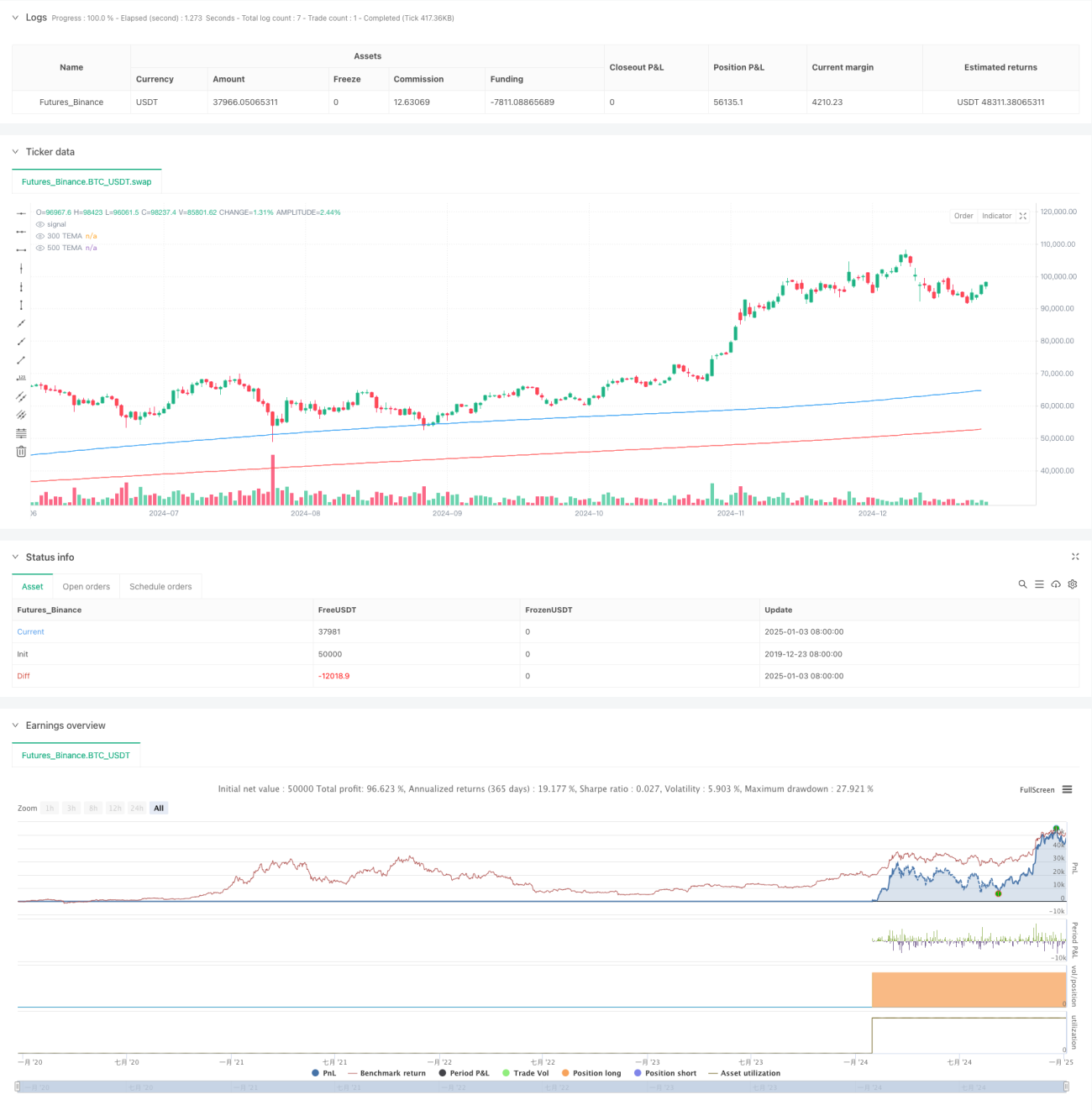

یہ حکمت عملی ایک ٹرینڈ فالو کرنے والا ٹریڈنگ سسٹم ہے جو ٹرپل ایکسپونینشل موونگ ایوریج (TEMA) پر مبنی ہے۔ یہ حکمت عملی قلیل مدتی اور طویل مدتی TEMA کے کراس اوور سگنلز کا موازنہ کرکے مارکیٹ کے رجحان کو پکڑتی ہے اور خطرے کو منظم کرنے کے لیے اتار چڑھاؤ پر مبنی اسٹاپ لاس استعمال کرتی ہے۔ یہ حکمت عملی 5 منٹ کے ٹائم فریم پر کام کرتی ہے اور 300 اور 500 ادوار کے TEMA اشاریوں کو سگنل جنریشن کی بنیاد کے طور پر استعمال کرتی ہے۔

حکمت عملی کا اصول

حکمت عملی کا بنیادی منطق درج ذیل کلیدی عناصر پر مبنی ہے:

- رجحان کی سمت شناخت کرنے کے لیے دو مختلف ادوار (300 اور 500) کے TEMA اشاریے استعمال کیے جاتے ہیں

- جب قلیل مدتی TEMA طویل مدتی TEMA کو اوپر سے کراس کرتا ہے، تو سسٹم لانگ (خرید) کا سگنل دیتا ہے

- جب قلیل مدتی TEMA طویل مدتی TEMA کو نیچے سے کراس کرتا ہے، تو سسٹم شارٹ (فروخت) کا سگنل دیتا ہے

- اسٹاپ لاس کی جگہ متعین کرنے کے لیے 10 ادوار کی بلند ترین اور پست ترین قیمتیں استعمال کی جاتی ہیں

- پوزیشن داخل ہونے کے بعد اس وقت تک رکھی جاتی ہے جب تک مخالف سگنل نہ آئے

حکمت عملی کے فوائد

- سگنل استحکام مضبوط: طویل مدت کے TEMA استعمال کرنے سے مارکیٹ کے شور کو مؤثر طریقے سے فلٹر کیا جا سکتا ہے اور جعلی سگنلز کو کم کیا جا سکتا ہے

- خطرے کا مکمل کنٹرول: اتار چڑھاؤ پر مبنی اسٹاپ لاس کے ساتھ مل کر، ایک تجارتی خطرے کو مؤثر طریقے سے کنٹرول کیا جا سکتا ہے

- رجحان کو پکڑنے کی بہتر صلاحیت: TEMA روایتی موونگ ایوریجز کے مقابلے میں رجحان پر تیز ردعمل ظاہر کرتا ہے

- مکمل تجارتی سائیکل: داخلے، اسٹاپ لاس اور منافع حاصل کرنے کی واضح شرائط شامل ہیں

- پیرامیٹرز کی اعلیٰ ایڈجسٹمنٹ: کلیدی پیرامیٹرز کو مارکیٹ کی خصوصیات کے مطابق لچکدار طریقے سے ایڈجسٹ کیا جا سکتا ہے

حکمت عملی کے خطرات

- سائیڈ ویز مارکیٹ کا خطرہ: رینج باؤنڈ مارکیٹ میں جعلی سگنلز کی وجہ سے مسلسل نقصان ہو سکتا ہے

- سلپیج کا خطرہ: 5 منٹ کے ٹائم فریم میں شدید اتار چڑھاؤ کے دوران بڑی سلپیج کا سامنا ہو سکتا ہے

- سرمائے کے انتظام کا خطرہ: مقررہ نقاط کا اسٹاپ لاس شدید اتار چڑھاؤ میں بہت زیادہ نقصان کا سبب بن سکتا ہے

- سگنل میں تاخیر: TEMA اشاریے میں فطری طور پر کچھ تاخیر ہوتی ہے، جس کی وجہ سے داخلے کا بہترین موقع ضائع ہو سکتا ہے

- پیرامیٹر کی حساسیت: مختلف مارکیٹ ماحول میں بہترین پیرامیٹرز میں بڑا فرق ہوتا ہے

حکمت عملی کی بہتری کی سمتیں

- مارکیٹ کے ماحول کی شناخت میں اضافہ: رجحان کی شدت کے اشاریے شامل کریں، مختلف مارکیٹ ماحول میں مختلف پیرامیٹرز استعمال کریں

- اسٹاپ لاس کے طریقہ کار کو بہتر بنانا: ATR پر مبنی ڈائنامک اسٹاپ لاس استعمال کرنے پر غور کریں تاکہ اسٹاپ لاس کی موافقت بڑھ سکے

- پوزیشن سائزنگ کو مکمل کریں: رجحان کی شدت کے مطابق کھلنے والی پوزیشنوں کی تعداد کو ڈائنامک طریقے سے ایڈجسٹ کریں

- انتباہی میکانزم شامل کریں: اہم قیمت کی سطحوں پر پہلے سے انتباہی سگنل جاری کریں

- والیوم انڈیکیٹر شامل کریں: سگنل کی تاثیر کی تصدیق کے لیے والیوم کے ساتھ مل کر استعمال کریں

خلاصہ

یہ حکمت عملی ایک مکمل ٹرینڈ فالونگ سسٹم ہے، جو TEMA اشاریوں کے کراس اوور کے ذریعے رجحان کو پکڑتی ہے اور ڈائنامک اسٹاپ لاس کے ساتھ خطرے کا انتظام کرتی ہے۔ یہ حکمت عملی منطقی طور پر صاف ہے، نفاذ میں آسان ہے اور عملی استعمال کے لیے موزوں ہے۔ تاہم، لائیو ٹریڈنگ میں مارکیٹ کے ماحول کی شناخت اور خطرے کے کنٹرول پر توجہ دینا ضروری ہے۔ تجویز ہے کہ بیک ٹیسٹ کی تصدیق کی بنیاد پر، اصل مارکیٹ کے حالات کے مطابق پیرامیٹرز کو بہتر بنایا جائے۔

- 1