ملٹی پیریڈ سپر ٹرینڈ ڈائنامک اہرام تجارتی حکمت عملی

جائزہ

یہ ایک کثیر سپرٹرینڈ (Supertrend) انڈیکیٹر پر مبنی پرامڈل ٹریڈنگ حکمت عملی ہے۔ یہ تین مختلف ادوار اور ضربوں کے ساتھ سپرٹرینڈ انڈیکیٹرز مرتب کر کے اعلیٰ احتمالی تجارتی مواقع کی نشاندہی کرتا ہے۔ حکمت عملی میں متحرک پرامڈل پوزیشن اضافہ (Pyramid Adding) استعمال کیا گیا ہے، جس میں زیادہ سے زیادہ تین بار داخلے کی اجازت ہے، اور منافع کو زیادہ سے زیادہ کرنے اور خطرے پر قابو پانے کے لیے متحرک سٹاپ لاس اور لچکدار اخراج کی شرائط شامل ہیں۔

حکمت عملی کا اصول

حکمت عملی میں تین مختلف پیرامیٹر سیٹس کے ساتھ سپرٹرینڈ انڈیکیٹر استعمال کیے گئے ہیں: تیز، درمیانی اور سست۔ داخلے کے اشارے ان تینوں انڈیکیٹرز کے تقاطع (Cross) اور رجحان کی سمت پر مبنی ہیں، اور تین تہوں پر مشتمل پرامڈل پوزیشن اضافہ استعمال کیا گیا ہے: پہلی تہہ میں اس وقت داخلہ لیا جاتا ہے جب تیز انڈیکیٹر نیچے کی طرف ہو، درمیانی انڈیکیٹر اوپر کی طرف ہو اور سست انڈیکیٹر نیچے کی طرف ہو؛ دوسری تہہ میں جب تیز اور درمیانی انڈیکیٹر دونوں نیچے کی طرف ہوں تو بریک آؤٹ کے ذریعے داخلہ لیا جاتا ہے؛ تیسری تہہ میں جب قیمت نئی بلند ترین سطح بنائے تو بریک آؤٹ کے ذریعے داخلہ لیا جاتا ہے۔ اخراج کے لیے متحرک سٹاپ لاس، اوسط قیمت سٹاپ لاس اور مجموعی رجحان کے الٹنے (Reversal) جیسے متعدد طریقہ کار استعمال کیے جاتے ہیں۔

حکمت عملی کے فوائد

- تصدیق کا کثیر طریقہ کار تجارت کی درستگی کو بڑھاتا ہے۔

- پرامڈل پوزیشن اضافہ رجحانی مارکیٹ میں منافع کو نمایاں طور پر بڑھا سکتا ہے۔

- متحرک سٹاپ لاس طریقہ کار نہ صرف منافع کی حفاظت کرتا ہے بلکہ رجحان کو مکمل طور پر ترقی کرنے کی گنجائش بھی دیتا ہے۔

- لچکدار اخراج کا طریقہ کار مختلف مارکیٹ کے حالات سے بہتر طور پر نمٹ سکتا ہے۔

- فیصدی پوزیشن سائز (Percentage Position Size) کا استعمال مختلف سرمایہ کے حجم کے مطابق ڈھلنے میں مدد دیتا ہے۔

حکمت عملی کے خطرات

- اتار چڑھاؤ والی مارکیٹ (Sideways Market) میں بار بار جھوٹے سگنل (False Signals) پیدا ہو سکتے ہیں۔

- پرامڈل پوزیشن اضافہ رجحان کے اچانک الٹنے پر بڑی پل بیک (Drawdown) کا سبب بن سکتا ہے۔

- کثیر انڈیکیٹرز سگنل میں تاخیر کا باعث بن سکتے ہیں۔

- پیرامیٹر کی اصلاح (Optimization) میں اوور فٹنگ (Overfitting) کا خطرہ ہوتا ہے۔

ان خطرات پر قابو پانے کے لیے سخت سرمایہ کاری کا انتظام اور بیک ٹیسٹ (Backtest) کی تصدیق تجویز کی جاتی ہے۔

حکمت عملی کی اصلاح کی سمت

- مارکیٹ کے ماحول کی فلٹرنگ (Market Environment Filter) کا اضافہ کیا جائے تاکہ مختلف اتار چڑھاؤ والے ماحول میں پیرامیٹرز کو متحرک طور پر ایڈجسٹ کیا جا سکے۔

- پوزیشن اضافے کے وقفے اور پوزیشن مختص تناسب (Position Allocation Ratio) کو بہتر بنایا جائے۔

- جھوٹے سگنلز کو فلٹر کرنے کے لیے مزید تکنیکی انڈیکیٹرز شامل کیے جائیں۔

- مارکیٹ کی تبدیلیوں کے مطابق ڈھلنے کے لیے خودکار انکولی پیرامیٹر (Adaptive Parameter) کا طریقہ کار تیار کیا جائے۔

- اخراج کے طریقہ کار کو مکمل کیا جائے، جیسے منافع کے ہدف اور وقت پر مبنی سٹاپ لاس کو شامل کیا جا سکتا ہے۔

خلاصہ

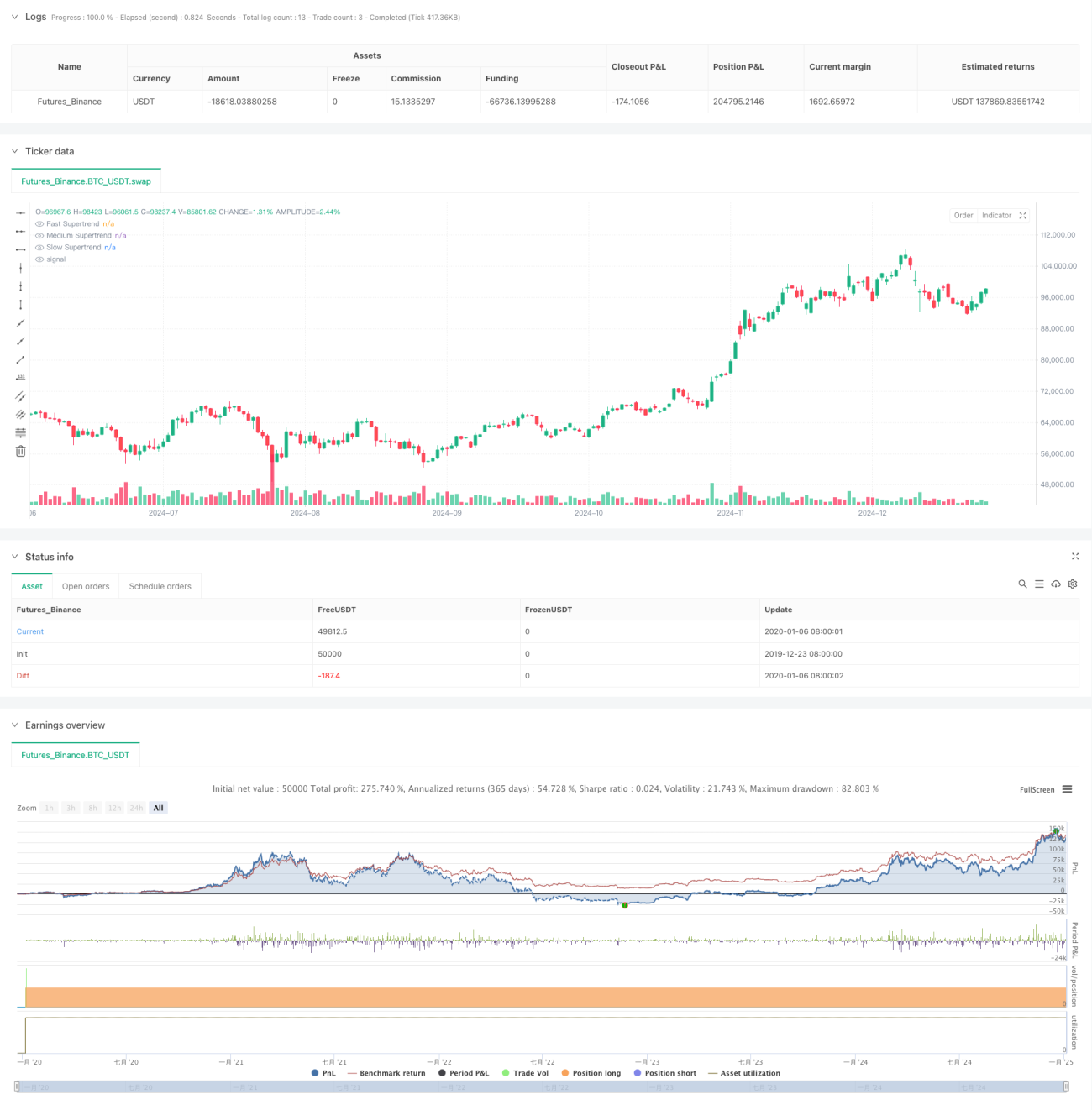

یہ حکمت عملی کثیر سپرٹرینڈ انڈیکیٹرز اور پرامڈل پوزیشن اضافے کے ذریعے رجحانی مواقع حاصل کرتی ہے، اور متحرک سٹاپ لاس اور لچکدار اخراج کے طریقہ کار کے ذریعے خطرے پر قابو پاتی ہے۔ اگرچہ اس میں کچھ حدود ہیں، لیکن مسلسل اصلاح اور سخت خطرے کے انتظام کے ساتھ، یہ حکمت عملی عملی تجارت میں اچھی کارکردگی دکھا سکتی ہے۔

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('4Vietnamese 3x Supertrend', overlay=true, max_bars_back=1000, initial_capital = 10000000000, slippage = 2, commission_type = strategy.commission.percent, commission_value = 0.013, default_qty_type=strategy.percent_of_equity, default_qty_value = 33.33, pyramiding = 3, margin_long = 0, margin_short = 0)

///////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////- 1