خلاصہ

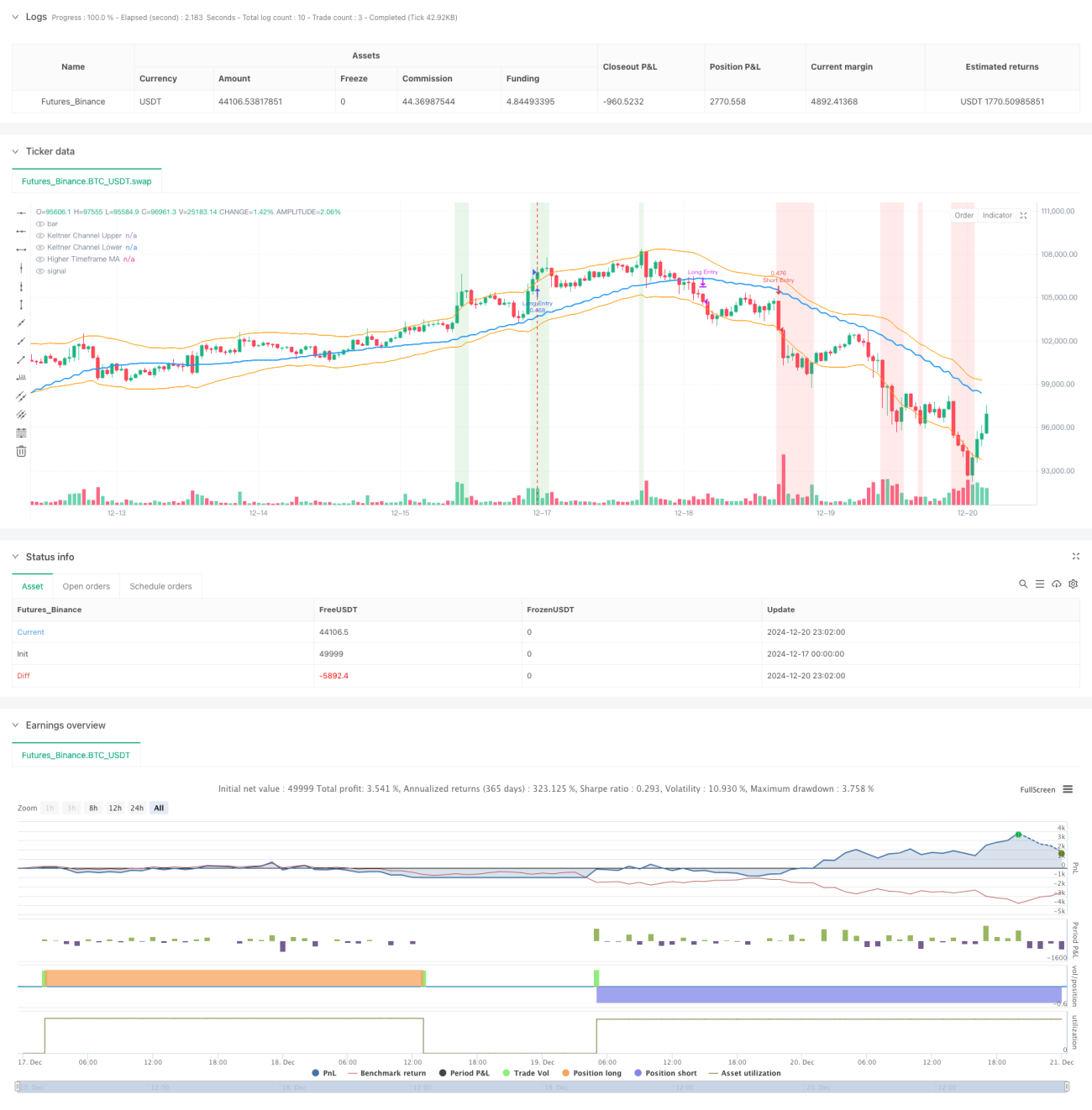

یہ حکمت عملی کیلٹنر چینل (Keltner Channel) اور متحرک سپورٹ/ریزسٹنس لیولز پر مبنی ایک پیچیدہ تجارتی نظام ہے۔ یہ متعدد ٹائم فریموں کے تجزیے کو مووِنگ ایوریج اور وولیٹیلیٹی انڈیکیٹرز کے ساتھ ملا کر ایک مکمل تجارتی فیصلہ سازی کا فریم ورک تشکیل دیتی ہے۔ حکمت عملی کا بنیادی مقصد قیمت کے اہم تکنیکی سطحوں کو توڑنے کے مواقع کی نشاندہی کرنا ہے، جبکہ مارکیٹ کے رجحان اور اتار چڑھاؤ کو مدنظر رکھتے ہوئے اعلیٰ احتمالی تجارتی مواقع حاصل کیے جاتے ہیں۔

حکمت عملی کا اصول

یہ حکمت عملی کثیر سطحی تکنیکی اشاروں کے نظام کا استعمال کرتی ہے:

- 21 ادوار کے کیلٹنر چینل کو بنیادی رجحان کے تعین کے لیے استعمال کیا جاتا ہے، جس کی چوڑائی ATR قدر سے متعین ہوتی ہے

- بائیں جانب 21 اور دائیں جانب 8 کندل استعمال کرتے ہوئے اہم سپورٹ اور ریزسٹنس لیولز کا حساب لگایا جاتا ہے

- اعلیٰ ٹائم فریم کی مووِنگ ایوریج کو رجحان فلٹر کے طور پر شامل کیا جاتا ہے

- مختصر مدت (5 ادوار) اور طویل مدت (30 ادوار) کی مووِنگ ایوریجز کو داخلے کے وقت کے تعین کے لیے استعمال کیا جاتا ہے

- اسٹاپ لاس کی پوزیشن کو متحرک طور پر ایڈجسٹ کرنے کے لیے ATR استعمال کیا جاتا ہے

حکمت عملی کے فوائد

- متعدد جہتی تکنیکی اشارے ایک دوسرے کی تصدیق کرتے ہیں، جس سے جھوٹے سگنلز میں کمی آتی ہے

- متحرک سپورٹ اور ریزسٹنس لیولز حقیقی وقت میں اپڈیٹ ہوتے ہیں، جو مارکیٹ کی تبدیلیوں کے مطابق ڈھل جاتے ہیں

- اعلیٰ ٹائم فریم کے تجزیے کے ذریعے کم درجے کے رجحانات کو فلٹر کیا جاتا ہے

- مختلف ٹائم فریموں کے مطابق اسٹاپ لاس پیرامیٹرز کو لچکدار طریقے سے ایڈجسٹ کیا جا سکتا ہے

- فیصدی بنیاد پر پوزیشن مینجمنٹ کا استعمال، جو رسک کو مؤثر طریقے سے کنٹرول کرتا ہے

حکمت عملی کے خطرات

- سائیڈ وے مارکیٹ میں بار بار تجارتی سگنلز پیدا ہو سکتے ہیں

- متعدد اشاروں کی تصدیق کی وجہ سے کچھ تجارتی مواقع ہاتھ سے نکل سکتے ہیں

- پیرامیٹر کی اصلاح میں اوور فٹنگ کا خطرہ ہے

- زیادہ اتار چڑھاؤ والے ماحول میں اسٹاپ لاس کی جگہ بہت وسیع ہو سکتی ہے

- مارکیٹ میں اچانک تبدیلی کی صورت میں سپورٹ اور ریزسٹنس لیولز ناکارہ ہو سکتے ہیں

حکمت عملی کی اصلاح کے رجحانات

- بریک آؤٹ کی صداقت کی تصدیق کے لیے حجم انڈیکیٹر کو شامل کرنا

- مارکیٹ کے اتار چڑھاؤ کے تجزیے کا ماڈیول شامل کرنا، پیرامیٹرز کو متحرک طور پر ایڈجسٹ کرنا

- سپورٹ اور ریزسٹنس لیولز کے حساب کتاب کے طریقہ کار کو بہتر بنانا، درستگی بڑھانا

- رجحان کی طاقت کا تعین شامل کرنا، داخلے کی شرائط کو مزید تفصیلی بنانا

- پوزیشن مینجمنٹ سسٹم کو مکمل کرنا، تاکہ رسک کا زیادہ باریک کنٹرول حاصل ہو سکے

خلاصہ

یہ ایک مکمل اور منطقی طور پر مضبوط مقداری تجارتی حکمت عملی ہے۔ کثیر سطحی تکنیکی اشاروں کے باہمی استعمال کے ذریعے، یہ تجارتی سگنلز کی وشوسنییتا کو یقینی بناتی ہے اور ساتھ ہی رسک کے مؤثر کنٹرول کو بھی حاصل کرتی ہے۔ حکمت عملی میں توسیع کی اچھی صلاحیت ہے، اور مسلسل اصلاح و بہتری کے ذریعے، مختلف مارکیٹ حالات میں مستحکم کارکردگی دکھانے کی امید کی جا سکتی ہے۔

/*backtest

start: 2024-12-17 00:00:00

end: 2024-12-21 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © sathcm

//@version=5

strategy("KMS", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.05, slippage=3)- 1