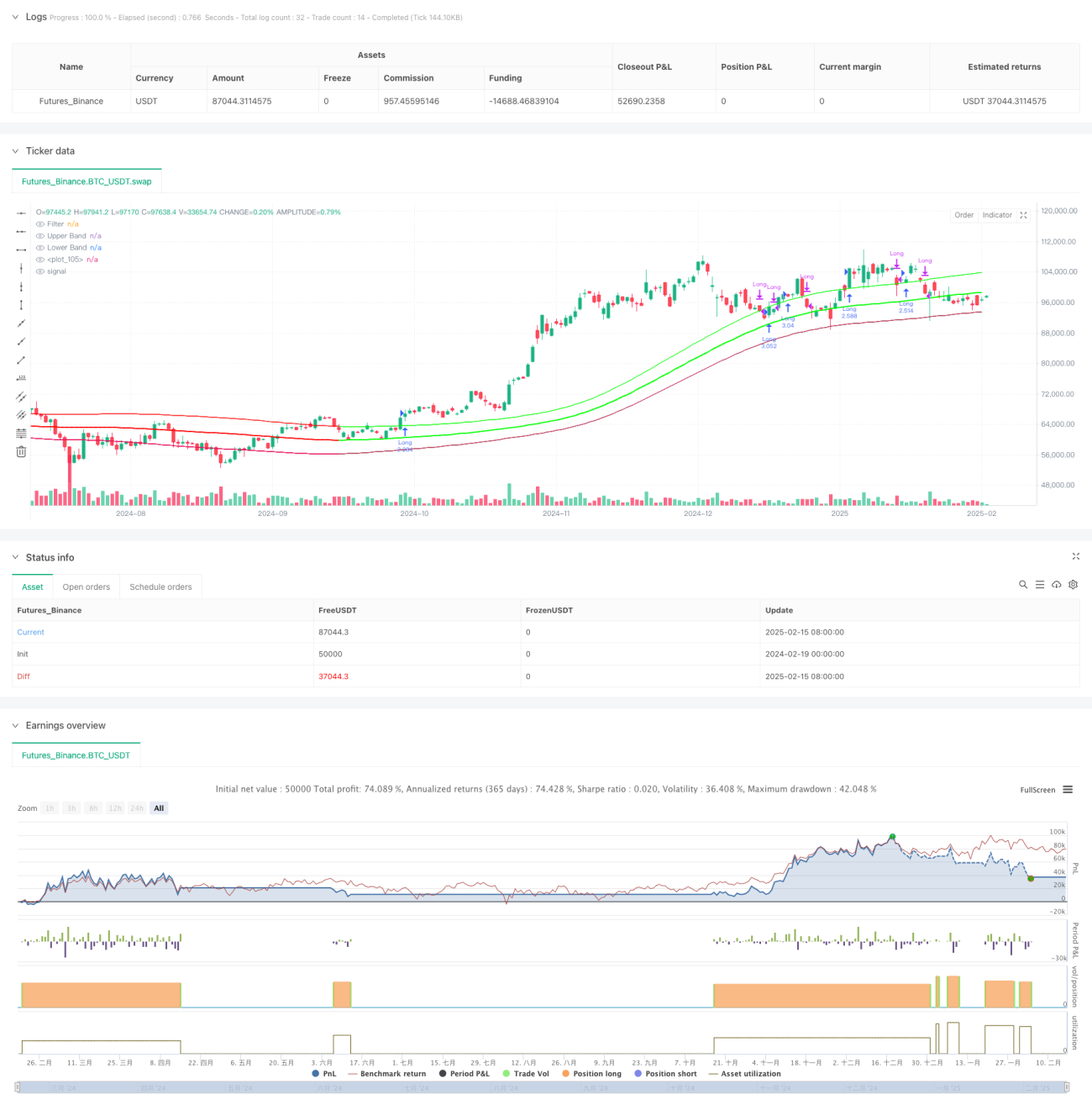

جائزہ

یہ حکمت عملی ایک گاوسی فلٹر اور StochRSI انڈیکیٹر پر مبنی رجحان کی پیروی کرنے والا تجارتی نظام ہے۔ یہ حکمت عملی گاوسی چینل کے ذریعے مارکیٹ کے رجحان کی شناخت کرتی ہے، اور StochRSI انڈیکیٹر کے زیادہ خریدنے اور زیادہ بیچنے والے زونوں کو ملا کر داخلے کے وقت کو بہتر بناتی ہے۔ یہ نظام کثیرالاسمی فٹنگ طریقہ استعمال کرتے ہوئے گاوسی چینل بناتا ہے، اوپر اور نیچے کے راستوں کی متحرک ایڈجسٹمنٹ کے ذریعے قیمت کے رجحان کی پیروی کرتا ہے، اور مارکیٹ کی حرکت کا درست سراغ لگاتا ہے۔

حکمت عملی کا اصول

حکمت عملی کا مرکز گاوسی فلٹرنگ الگورتھم پر مبنی قیمت کا چینل ہے۔ مخصوص عمل درآمد میں درج ذیل اہم مراحل شامل ہیں:

- کثیرالاسمی افعال f_filt9x کا استعمال کرتے ہوئے 9ویں درجے کا گاوسی فلٹرنگ، قطب کی اصلاح کے ذریعے فلٹرنگ اثر کو بہتر بنایا جاتا ہے۔

- HLC3 قیمت کی بنیاد پر مرکزی فلٹر لائن اور اتار چڑھاؤ کا چینل شمار کیا جاتا ہے۔

- reducedLag موڈ متعارف کر کے فلٹرنگ میں تاخیر کم کی جاتی ہے، fastResponse موڈ کے ذریعے ردعمل کی رفتار بڑھائی جاتی ہے۔

- StochRSI انڈیکیٹر کے زیادہ خریدے/زیادہ بیچے گئے زونز (80/20) کا استعمال کرتے ہوئے تجارتی سگنل طے کیے جاتے ہیں۔

- جب گاوسی چینل اوپر کی طرف ہو اور قیمت اوپری راستے کو توڑے، تو StochRSI انڈیکیٹر کے ساتھ مل کر لانگ سگنل پیدا ہوتا ہے۔

- جب قیمت اوپری راستے سے نیچے گر جائے تو پوزیشن بند کر دی جاتی ہے۔

حکمت عملی کے فوائد

- گاوسی فلٹرنگ میں شور کم کرنے کی بہترین صلاحیت ہے، جو مارکیٹ کے شور کو مؤثر طریقے سے فلٹر کر سکتی ہے۔

- کثیرالاسمی فٹنگ کے ذریعے رجحان کی ہموار پیروی حاصل کی جاتی ہے، جس سے جعلی سگنل کم ہوتے ہیں۔

- تاخیر کی اصلاح اور تیز رسپانس موڈ کو سپورٹ کرتا ہے، مارکیٹ کی خصوصیات کے مطابق لچکدار طریقے سے ایڈجسٹ کیا جا سکتا ہے۔

- StochRSI انڈیکیٹر کے ساتھ مل کر داخلے کے وقت کو بہتر بنایا جاتا ہے، جس سے تجارتی کامیابی کی شرح بڑھتی ہے۔

- متحرک چینل کی چوڑائی استعمال کی جاتی ہے، جو مارکیٹ کے اتار چڑھاؤ میں تبدیلیوں کے مطابق خودکار طریقے سے ڈھل جاتی ہے۔

حکمت عملی کے خطرات

- گاوسی فلٹرنگ میں کچھ تاخیر ہوتی ہے، جس کی وجہ سے داخلہ یا خارج ہونا بروقت نہیں ہو سکتا۔

- اتار چڑھاؤ والی مارکیٹ میں بار بار تجارتی سگنل پیدا ہو سکتے ہیں، جس سے تجارتی اخراجات بڑھ جاتے ہیں۔

- StochRSI انڈیکیٹر بعض مارکیٹ حالات میں تاخیر والے سگنل پیدا کر سکتا ہے۔

- پیرامیٹر کی اصلاح کا عمل پیچیدہ ہے، مختلف مارکیٹ ماحول میں پیرامیٹرز کو دوبارہ ایڈجسٹ کرنے کی ضرورت ہوتی ہے۔

- نظام کو کمپیوٹیشنل وسائل کی زیادہ ضرورت ہوتی ہے، حقیقی وقت میں حساب کتاب میں کچھ تاخیر ہوتی ہے۔

حکمت عملی کی اصلاح کی سمت

- خودکار پیرامیٹر اصلاح کا طریقہ کار متعارف کروایا جائے، مارکیٹ کی حالت کے مطابق پیرامیٹرز کو متحرک طور پر ایڈجسٹ کیا جائے۔

- مارکیٹ ماحول کی شناخت کا ماڈیول شامل کیا جائے، مختلف مارکیٹ حالات میں مختلف پیرامیٹر مجموعے استعمال کیے جائیں۔

- گاوسی فلٹرنگ الگورتھم کو بہتر بنایا جائے، مزید کمپیوٹیشنل تاخیر کم کی جائے۔

- مزید تکنیکی انڈیکیٹرز متعارف کروائے جائیں تاکہ کراس تصدیق ہو سکے، سگنل کی وشوسنییتا بڑھائی جائے۔

- ذہین نقصان روکنے کا طریقہ کار تیار کیا جائے، خطرے پر قابو پانے کی صلاحیت بڑھائی جائے۔

خلاصہ

یہ حکمت عملی گاوسی فلٹرنگ اور StochRSI انڈیکیٹر کے امتزاج کے ذریعے مارکیٹ کے رجحان کی مؤثر پیروی کرتی ہے۔ نظام میں شور کم کرنے اور رجحان کی شناخت کی اچھی صلاحیت ہے، لیکن اس میں کچھ تاخیر اور پیرامیٹر کی اصلاح میں دشواری بھی ہے۔ مسلسل اصلاح اور بہتری کے ذریعے، یہ حکمت عملی حقیقی تجارت میں مستحکم منافع حاصل کرنے کی امید رکھتی ہے۔

/*backtest

start: 2024-02-19 00:00:00

end: 2025-02-16 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Demo GPT - Gaussian Channel Strategy v3.0", overlay=true, commission_type=strategy.commission.percent, commission_value=0.1, slippage=0, default_qty_type=strategy.percent_of_equity, default_qty_value=250)

// ============================================- 1