متحرک رجحان کی پیروی کے لیے EMA-ADX کثیر سطحی منافع وصولی کی حکمت عملی

خلاصہ

یہ حکمت عملی EMA اور ADX انڈیکیٹرز پر مبنی ایک ٹرینڈ فالو ٹریڈنگ سسٹم ہے، جو متعدد سطحوں پر منافع لینے (Take Profit) اور متحرک اسٹاپ لاس (Moving Stop Loss) کے ذریعے سرمایہ کے انتظام کو بہتر بناتی ہے۔ حکمت عملی EMA اوسط کو رجحان کی سمت کے تعین کے لیے، ADX انڈیکیٹر کو رجحان کی مضبوطی کی فلٹرنگ کے لیے استعمال کرتی ہے، اور تین سطحوں پر منافع لینے کا طریقہ کار رکھتی ہے تاکہ منافع کو حصوں میں حاصل کیا جا سکے، جبکہ ATR کی مدد سے متحرک اسٹاپ پوزیشن کا تعین کر کے خطرے پر قابو پایا جاتا ہے۔

حکمت عملی کا اصول

حکمت عملی کا بنیادی منطق درج ذیل اہم حصوں پر مشتمل ہے:

- 50 پیریڈ کی EMA اوسط کو رجحان کی سمت کے تعین کے لیے استعمال کیا جاتا ہے؛ قیمت EMA کے اوپر جانے پر لانگ (Long) کھولا جاتا ہے اور نیچے جانے پر شارٹ (Short) کھولا جاتا ہے۔

- 14 پیریڈ کے ADX انڈیکیٹر کے ذریعے کمزور رجحان کو فلٹر کیا جاتا ہے؛ جب ADX>20 ہو تو رجحان کو موثر سمجھا جاتا ہے۔

- 14 پیریڈ کے ATR کی بنیاد پر متحرک اسٹاپ پوزیشن کا حساب لگایا جاتا ہے؛ لانگ آرڈر کے لیے سب سے کم قیمت سے 1 ATR کم، اور شارٹ آرڈر کے لیے سب سے زیادہ قیمت میں 1 ATR کا اضافہ کیا جاتا ہے۔

- تین سطحوں پر منافع لینے کا طریقہ کار:

- پہلی سطح: 30% پوزیشن 1 ATR پر منافع لیتی ہے۔

- دوسری سطح: 50% پوزیشن 2 ATR پر منافع لیتی ہے۔

- تیسری سطح: 20% پوزیشن 3 ATR کے متحرک منافع (Trailing Take Profit) کے ساتھ منافع لیتی ہے۔

- جب قیمت دوسری سطح کے منافع کی پوزیشن تک پہنچ جاتی ہے، تو خود بخود تمام باقی پوزیشنیں بند کر دی جاتی ہیں۔

حکمت عملی کے فوائد

- کثیر سطحی منافع لینے کا ڈیزائن نہ صرف وقت پر منافع کو محفوظ کرتا ہے بلکہ بڑے رجحان سے محروم بھی نہیں ہونے دیتا۔

- متحرک اسٹاپ لاس کا طریقہ کار مارکیٹ کے اتار چڑھاؤ کے مطابق خود کو ڈھال سکتا ہے، جس سے متحرک خطرے پر قابو پایا جا سکتا ہے۔

- ADX کی فلٹرنگ مؤثر طریقے سے اتار چڑھاؤ والی مارکیٹ میں غلط سگنلز سے بچاتی ہے۔

- EMA اور قیمت کا کراس اوور واضح داخلے کے سگنل فراہم کرتا ہے۔

- حصوں میں منافع لینے سے جذباتی اتار چڑھاؤ کم ہوتا ہے، جس سے حکمت عملی کے طویل مدتی نفاذ میں مدد ملتی ہے۔

حکمت عملی کے خطرات

- اتار چڑھاؤ والی مارکیٹ میں بار بار اندراج اور اخراج سے لاگت بڑھ سکتی ہے۔

- EMA ایک پسماندہ اشارہ (Lagging Indicator) ہے، جو تیز رفتار الٹ پلٹ پر بروقت رد عمل ظاہر نہیں کر سکتا۔

- مقررہ ADX حد (Threshold) مختلف مارکیٹ حالات میں ایڈجسٹمنٹ کی ضرورت پڑ سکتی ہے۔

- کثیر سطحی منافع لینا یک طرفہ رجحان میں جلد پوزیشن کم کرنے کا سبب بن سکتا ہے۔

کمی کے اثرات کو کم کرنے کے اقدامات:

- مختلف مارکیٹ سائیکل کے مطابق ADX حد کو متحرک طور پر ایڈجسٹ کیا جا سکتا ہے۔

- رجحان کی تصدیق کے لیے اضافی انڈیکیٹر شامل کرنے پر غور کیا جا سکتا ہے۔

- منافع لینے کے تناسب کو مزید باریک بینی سے پیرامیٹر آپٹیمائز کیا جا سکتا ہے۔

حکمت عملی کی بہتری کے امکانات

- رجحان کی تصدیق کو مضبوط بنانے کے لیے حجم (Volume) انڈیکیٹر متعارف کرانا۔

- مارکیٹ کے اتار چڑھاؤ کے مطابق ADX حد کو متحرک طور پر ایڈجسٹ کرنا۔

- منافع لینے کی سطحوں پر پوزیشن کے حصص کے تناسب کو بہتر بنانا۔

- رجحان کی مضبوطی کی درجہ بندی شامل کرنا، جس کے مطابق مختلف منافع لینے کی حکمت عملی تیار کی جائے۔

- موسمی عوامل اور مارکیٹ سائیکل کی تشخیص کو شامل کرنے پر غور کرنا۔

خلاصہ

یہ ایک مکمل ساخت اور واضح منطق پر مبنی ٹرینڈ فالو حکمت عملی ہے، جو کثیر سطحی منافع لینے اور متحرک اسٹاپ لاس کے ذریعے منافع اور خطرے میں توازن پیدا کرتی ہے۔ حکمت عملی کا مجموعی ڈیزائن مقداری ٹریڈنگ کے بنیادی اصولوں کے مطابق ہے اور اس میں توسیع پذیری اور بہتری کی گنجائش موجود ہے۔ مناسب پیرامیٹر ایڈجسٹمنٹ اور اپ گریڈ کے ذریعے، یہ حکمت عملی مختلف مارکیٹ حالات میں مستحکم کارکردگی دکھانے کی امید رکھتی ہے۔

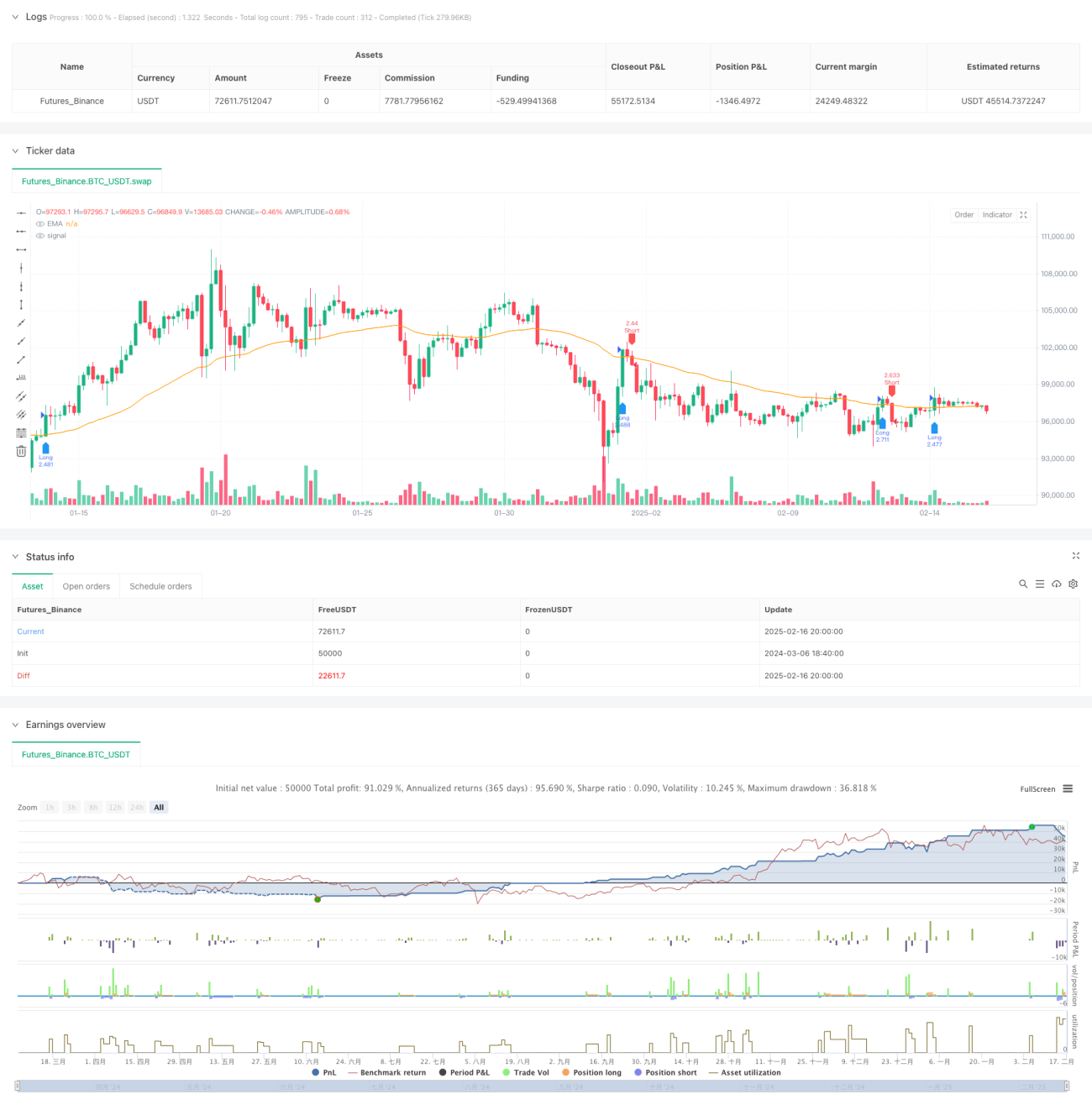

/*backtest

start: 2024-03-06 18:40:00

end: 2025-02-17 00:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("BTC Optimized Strategy v6", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=250)

// === 參數設定 ===- 1