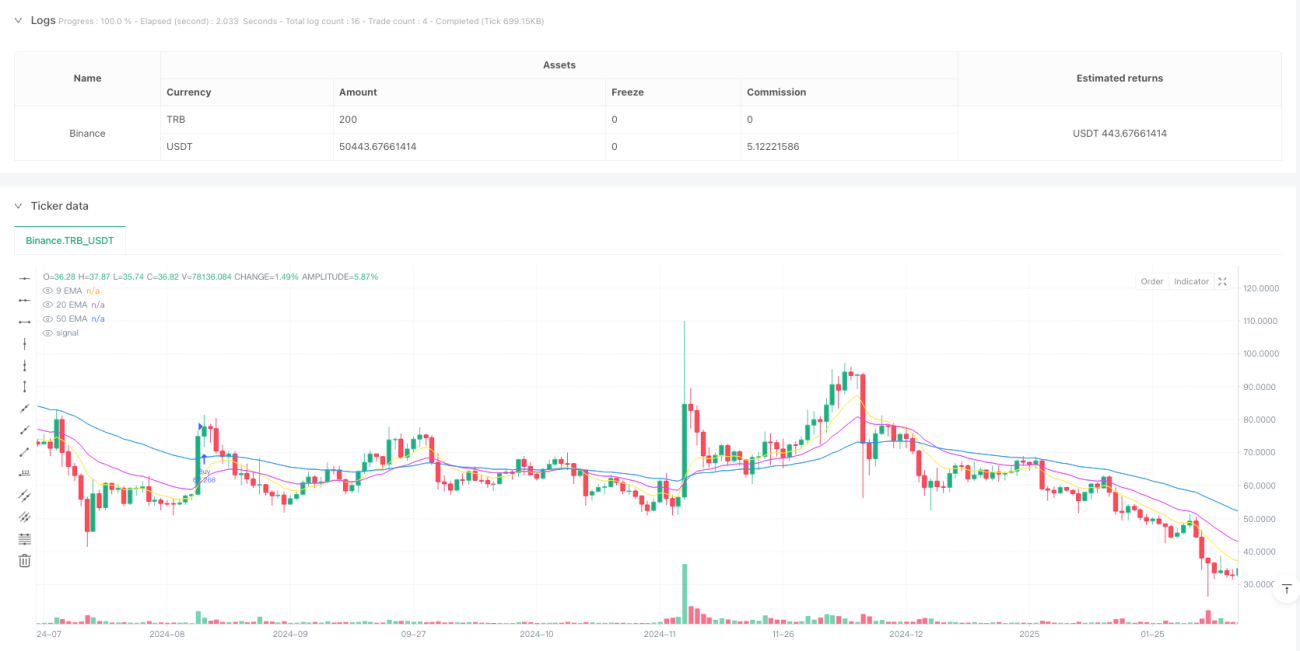

خلاصہ

یہ ایک کثیر موونگ ایوریج ٹرینڈ فالوونگ سسٹم پر مبنی کرپٹو کرنسی ٹریڈنگ حکمت عملی ہے، جس میں RSI اور ATR اشاریوں کو تجارتی فلٹرنگ اور رسک مینجمنٹ کے لیے استعمال کیا گیا ہے۔ یہ حکمت عملی بنیادی طور پر مرکزی کرپٹو کرنسیوں میں تجارت کرتی ہے اور روزانہ تجارت کی فریکوئنسی کی حد اور متحرک منافع/نقصان روک کر رسک کو کنٹرول کرتی ہے۔ حکمت عملی رجحان کی سمت کا تعین کرنے کے لیے تین ایکسپوونینشل موونگ ایوریجز (EMA) (9، 20 اور 50 ادوار) استعمال کرتی ہے، اور تجارتی فلٹرنگ کے لیے ریلیٹیو سٹرینتھ انڈیکس (RSI) اور ایوریج ٹرو رینج (ATR) کو معاون اشاریوں کے طور پر استعمال کرتی ہے۔

حکمت عملی کا اصول

حکمت عملی کے بنیادی تجارتی منطق میں درج ذیل اہم حصے شامل ہیں:

- رجحان کا تعین: رجحان کی سمت کا تعین کرنے کے لیے تین EMA (9/20/50) استعمال کیے جاتے ہیں۔ جب مختصر مدت کا EMA درمیانی مدت کے EMA کو اوپر سے کراس کرتا ہے اور قیمت طویل مدت کے EMA سے اوپر ہوتی ہے، تو اسے صعودی رجحان سمجھا جاتا ہے؛ اس کے برعکس، اسے نزولی رجحان سمجھا جاتا ہے۔

- تجارتی فلٹر: RSI (14) کو انتہائی خرید و فروخت (overbought/oversold) فلٹرنگ کے لیے استعمال کیا جاتا ہے۔ خرید سگنل کے لیے RSI 45-70 کے درمیان ہونا ضروری ہے، جبکہ فروخت سگنل کے لیے RSI 30-55 کے درمیان ہونا ضروری ہے۔

- رجحان کی مضبوطی کی تصدیق: اس بات کو یقینی بنانے کے لیے کہ رجحان کافی مضبوط ہے، قیمت اور 50 ادوار کے EMA کے درمیان فاصلہ ATR کے 1.1 گنا سے زیادہ ہونا ضروری ہے۔

- رسک مینجمنٹ: مختلف کرپٹو کرنسیوں کے اتار چڑھاؤ کی خصوصیات کے مطابق، 2.5-3.2 گنا ATR کا سٹاپ نقصان اور 3.5-5.0 گنا ATR کا منافع روک مقرر کیا جاتا ہے۔

- تجارت کی فریکوئنسی کا کنٹرول: ہر تجارتی دن میں زیادہ سے زیادہ ایک تجارت کی اجازت ہے تاکہ ضرورت سے زیادہ تجارت سے بچا جا سکے۔

حکمت عملی کے فوائد

- متحرک رسک مینجمنٹ: ATR کے ذریعے منافع اور نقصان روک کو متحرک طور پر ایڈجسٹ کیا جاتا ہے، جو کرپٹو کرنسی مارکیٹ کی تیز اتار چڑھاؤ کی خصوصیات کے مطابق ہے۔

- امتیازی سلوک: مختلف کرپٹو کرنسیوں کے اتار چڑھاؤ کے مطابق مختلف رسک پیرامیٹرز مقرر کیے گئے ہیں۔

- متعدد فلٹرنگ میکانزم: رجحان، رفتار، اور اتار چڑھاؤ کے اشاریوں کو ملا کر تجارتی معیار کو بہتر بنایا گیا ہے۔

- تجارت کی فریکوئنسی کی حد: روزانہ تجارت کی حد کے ذریعے ضرورت سے زیادہ تجارت کے خطرے کو کم کیا گیا ہے، خاص طور پر کرپٹو کرنسی مارکیٹ کی تیز اتار چڑھاؤ کی خصوصیات کے لیے موزوں ہے۔

- مناسب سرمایہ انتظام: اکاؤنٹ کے سائز اور رسک لیول کی بنیاد پر تجارتی حجم کا متحرک حساب لگایا جاتا ہے، جس سے سرمائے کی حفاظت ہوتی ہے۔

حکمت عملی کے خطرات

- رجحان تبدیل ہونے کا خطرہ: کرپٹو کرنسی مارکیٹ میں شدید اتار چڑھاؤ کے دوران بڑے نقصان کا سامنا ہو سکتا ہے۔

- سلپج کا خطرہ: ناکافی لیکویڈیٹی کی صورت میں بڑی سلپج کا سامنا ہو سکتا ہے۔

- تجارتی مواقع کی حد: روزانہ تجارت کی حد کی وجہ سے تیزی سے چلنے والی مارکیٹ میں مواقع ضائع ہو سکتے ہیں۔

- پیرامیٹر کی حساسیت: متعدد اشاریوں کے پیرامیٹرز کی سیٹنگ حکمت عملی کی کارکردگی کو متاثر کرتی ہے اور باقاعدہ اصلاح کی ضرورت ہوتی ہے۔

- مارکیٹ کے ماحول پر انحصار: حکمت عملی رجحانی مارکیٹ میں بہتر کارکردگی دکھاتی ہے، لیکن اتار چڑھاؤ والی مارکیٹ میں جھوٹے سگنل پیدا کر سکتی ہے۔

حکمت عملی کی اصلاح کے امکانات

- مارکیٹ کے اتار چڑھاؤ کے دور کا تجزیہ: کرپٹو کرنسی مارکیٹ کے مختلف اتار چڑھاؤ کے ادوار کے مطابق پیرامیٹرز کو متحرک طور پر ایڈجسٹ کیا جا سکتا ہے۔

- تجارتی وقت کی فلٹرنگ کو بہتر بنانا: عالمی اہم تجارتی سیشنز کی بنیاد پر فلٹرنگ کی شرائط شامل کی جا سکتی ہیں۔

- خارج کے میکانزم کو بہتر بنانا: متحرک سٹاپ نقصان یا مارکیٹ کے جذبات پر مبنی متحرک خارج ہونے کا طریقہ کار شامل کیا جا سکتا ہے۔

- تجارتی حجم کا انتظام: مارکیٹ کے اتار چڑھاؤ کی بنیاد پر تجارتی حجم کو متحرک طور پر ایڈجسٹ کیا جا سکتا ہے۔

- مارکیٹ کے جذبات کے اشاریوں کا اضافہ: چین پر مبنی ڈیٹا یا سوشل میڈیا کے جذباتی اشاریوں کو شامل کرکے تجارتی فلٹرنگ کو بڑھایا جا سکتا ہے۔

خلاصہ

یہ حکمت عملی متعدد تکنیکی اشاریوں کے جامع استعمال کے ذریعے ایک نسبتاً مستحکم کرپٹو کرنسی تجارتی نظام فراہم کرتی ہے۔ مختلف رسک پیرامیٹرز اور سخت تجارتی فریکوئنسی کنٹرول کے ذریعے، یہ منافع اور رسک کے درمیان بہتر توازن قائم کرتی ہے۔ حکمت عملی کا بنیادی فائدہ اس کا متحرک رسک مینجمنٹ میکانزم اور مکمل فلٹرنگ سسٹم ہے، لیکن اس کے ساتھ ساتھ کرپٹو کرنسی مارکیٹ کے خاص طور پر تیز اتار چڑھاؤ اور لیکویڈیٹی کے خطرات پر بھی توجہ دینے کی ضرورت ہے۔ مسلسل اصلاح اور بہتری کے ذریعے، یہ حکمت عملی مختلف مارکیٹ حالات میں مستحکم کارکردگی دکھانے کی صلاحیت رکھتی ہے۔

/*backtest

start: 2015-02-22 00:00:00

end: 2025-02-18 17:23:25

period: 1h

basePeriod: 1h

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © buffalobillcody

//@version=6

strategy("Backtest Last 2880 Baars Filers and Exits", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=2, backtest_fill_limits_assumption=0)- 1