جائزہ

یہ ایک اعلیٰ تعدد تجارتی حکمت عملی کا نظام ہے جو بولنگر بینڈز (Bollinger Bands)، مووِنگ ایوریج کنورجینس ڈائیورجینس (MACD) اور حجم کے تجزیے کو یکجا کرتا ہے۔ یہ حکمت عملی بولنگر بینڈز کے اوپری اور نچلے بینڈز سے قیمت کے بریک آؤٹ اور واپسی کی نشاندہی کرکے، MACD کی مومینٹم انڈیکیٹر اور حجم کی تصدیق کے ساتھ مل کر بازار کے الٹ جانے کے مواقع کو پکڑتی ہے۔ نظام روزانہ زیادہ سے زیادہ تجارتی لین دین کی تعداد کی حد مقرر کرتا ہے اور ایک مکمل رسک مینجمنٹ میکانزم سے لیس ہے۔

حکمت عملی کا اصول

یہ حکمت عملی بنیادی طور پر درج ذیل تین بنیادی انڈیکیٹرز کے امتزاج پر مبنی ہے:

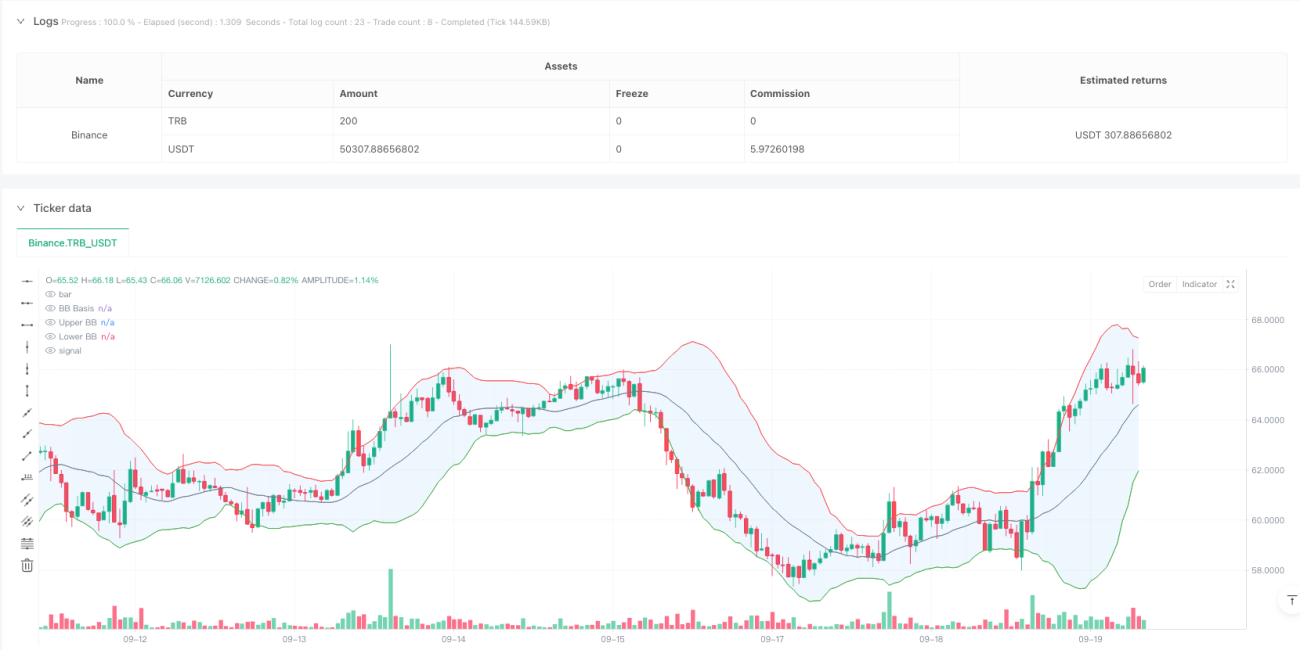

- بولنگر بینڈز انڈیکیٹر: 20 دورانیے کی سادہ مووِنگ ایوریج (SMA) کو درمیانی بینڈ کے طور پر استعمال کرتا ہے، جس میں معیاری انحراف کا ضریب 2.0 ہے تاکہ اوپری اور نچلے بینڈز کا حساب لگایا جا سکے۔ جب قیمت بولنگر بینڈز سے بریک آؤٹ کر کے واپس آتی ہے تو نظام ممکنہ تجارتی سگنل جاری کرتا ہے۔

- MACD انڈیکیٹر: معیاری پیرامیٹرز (12,26,9) استعمال کرتا ہے تاکہ قیمت کے رجحان کی مومینٹم کی تصدیق کی جا سکے۔ جب MACD لائن سگنل لائن کے اوپر ہوتی ہے تو لمبی پوزیشن (لونگ) کی تصدیق ہوتی ہے، اور جب سگنل لائن کے نیچے ہوتی ہے تو چھوٹی پوزیشن (شارٹ) کی تصدیق ہوتی ہے۔

- حجم کا تجزیہ: 20 دورانیے کی مووِنگ ایوریج کے ذریعے حجم کی تصدیق کی جاتی ہے، جس میں سگنل کے وقت حجم کم از کم اوسط سطح پر ہونا ضروری ہے تاکہ بازار کی شرکت کو یقینی بنایا جا سکے۔

حکمت عملی کے فوائد

- متعدد سگنل کی تصدیق: بولنگر بینڈز، MACD اور حجم کی تین گنا تصدیق کے ذریعے تجارتی سگنلز کی اعتبار میں نمایاں اضافہ ہوتا ہے۔

- بصری ڈیزائن: نظام بھرپور چارٹ اشارے فراہم کرتا ہے، بشمول بولنگر بینڈز کا بھرنا، سگنل کے نشانات اور پس منظر کے رنگ میں تبدیلی، جس سے تاجر تیزی سے تجارتی مواقع کی شناخت کر سکتے ہیں۔

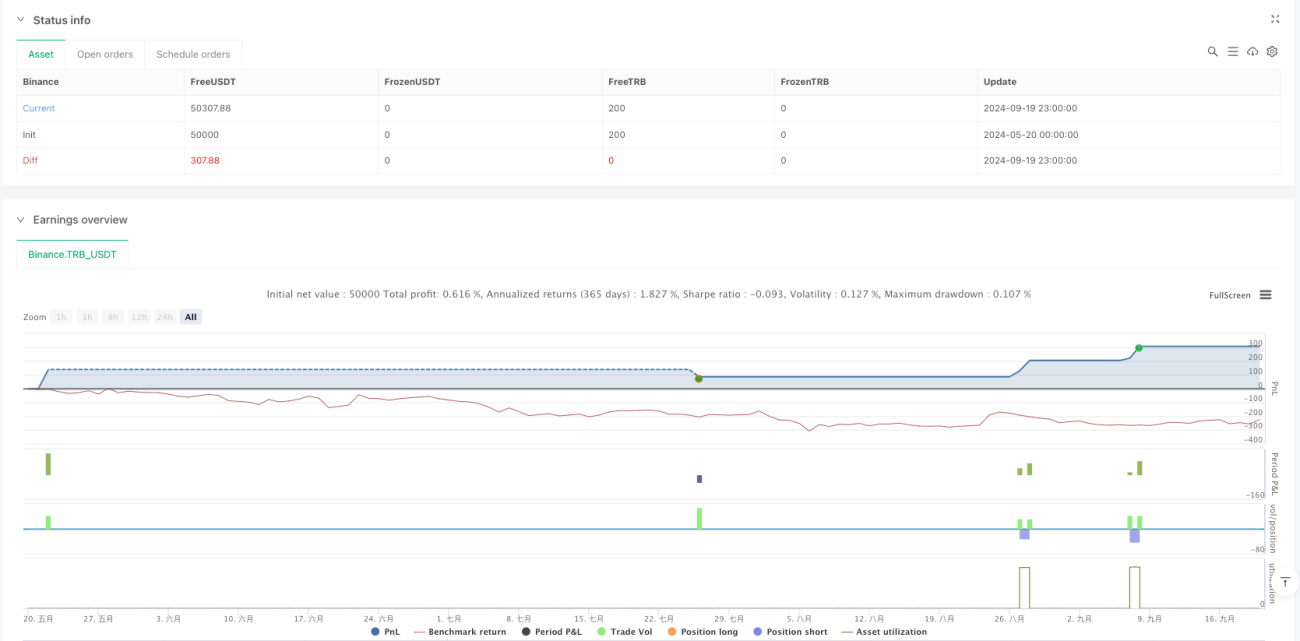

- مکمل رسک کنٹرول: مقررہ اسٹاپ لاس اور منافع کا ہدف نافذ کیا گیا ہے، اور روزانہ زیادہ سے زیادہ تجارتی لین دین کی تعداد کو محدود کیا گیا ہے، جس سے رسک کی نمائش کو مؤثر طریقے سے کنٹرول کیا جا سکتا ہے۔

- نظامی عمل: حکمت عملی داخلے اور خارج ہونے کی واضح شرائط فراہم کرتی ہے، جس سے موضوعی فیصلوں کی وجہ سے غیر یقینی صورتحال کم ہوتی ہے۔

حکمت عملی کے خطرات

- بازار کے اتار چڑھاؤ کا خطرہ: زیادہ اتار چڑھاؤ والے بازاروں میں جھوٹے بریک آؤٹ سگنلز پیدا ہو سکتے ہیں، جس سے تجارتی نقصان ہو سکتا ہے۔

- سلپیج کا خطرہ: اعلیٰ تعدد تجارتی ماحول میں سلپیج کے بڑے اخراجات کا سامنا ہو سکتا ہے، جس سے حقیقی منافع متاثر ہو سکتا ہے۔

- لیکویڈیٹی کا خطرہ: حجم کی شرط بازار میں ناکافی لیکویڈیٹی کی صورت میں تجارتی مواقع کو محدود کر سکتی ہے۔

- نظامی خطرہ: مقررہ پیرامیٹرز بازار کے حالات میں شدید تبدیلی کے مطابق ڈھلنے سے قاصر ہو سکتے ہیں۔

حکمت عملی کی بہتری کی سمتیں

- پیرامیٹرز کی متحرک اصلاح: خودکار پیرامیٹر ایڈجسٹمنٹ میکانزم متعارف کرایا جا سکتا ہے تاکہ بولنگر بینڈز اور MACD کے پیرامیٹرز بازار کے حالات کے مطابق خود بخود ایڈجسٹ ہو سکیں۔

- بازار کے دور کی شناخت: بازار کے دور کی تشخیص کا ماڈیول شامل کیا جا سکتا ہے تاکہ مختلف بازار کے ادوار میں مختلف تجارتی حکمت عملیوں کو اپنایا جا سکے۔

- رسک مینجمنٹ کی بہتری: متحرک اسٹاپ لاس میکانزم متعارف کرایا جا سکتا ہے، جس میں بازار کے اتار چڑھاؤ کی بنیاد پر اسٹاپ لاس کی پوزیشن کو ایڈجسٹ کیا جا سکے۔

- سگنل فلٹر میں اضافہ: رجحان کی طاقت کا فلٹر شامل کیا جا سکتا ہے تاکہ سائیڈ ویز مارکیٹ میں بہت زیادہ تجارتی سگنلز سے بچا جا سکے۔

خلاصہ

یہ حکمت عملی بولنگر بینڈز کے الٹ جانے کے سگنلز، MACD کے رجحان کی تصدیق اور حجم کی جانچ کے امتزاج کے ذریعے ایک مکمل تجارتی نظام تشکیل دیتی ہے۔ نظام کا بصری ڈیزائن اور سخت رسک کنٹرول اسے خاص طور پر انٹرا ڈے ٹریڈنگ کے لیے موزوں بناتا ہے۔ اگرچہ اس میں کچھ بازار خطرات موجود ہیں، لیکن مسلسل بہتری اور پیرامیٹرز کی ایڈجسٹمنٹ کے ذریعے یہ حکمت عملی مختلف بازار کے حالات میں مستحکم کارکردگی دکھانے کی امید رکھتی ہے۔

- 1