جائزہ

یہ حکمت عملی ایک اسٹاکسٹک آسیلیٹر (Stochastic Oscillator) پر مبنی ملٹی ٹائم فریم بینڈ ٹریڈنگ سسٹم ہے۔ یہ موجودہ ٹائم فریم اور اعلیٰ ٹائم فریم کے اسٹاکسٹک آسیلیٹر سگنلز کو ملا کر تجارتی مواقع کی نشاندہی کرتی ہے اور متحرک اسٹاپ لاس اور ٹیک پرافٹ کے ذریعے خطرے کا انتظام کرتی ہے۔ یہ حکمت عملی زیادہ اتار چڑھاؤ والی مارکیٹوں کے لیے موزوں ہے اور قیمتوں میں قلیل مدتی اتار چڑھاؤ کو پکڑ کر منافع حاصل کرتی ہے۔

حکمت عملی کا اصول

حکمت عملی کا بنیادی منطق درج ذیل اہم عناصر پر مبنی ہے:

- دو ٹائم فریم (موجودہ اور اعلیٰ) پر اسٹاکسٹک آسیلیٹر کے سگنلز کی تصدیق کا استعمال

- زیادہ خریدے/زیادہ فروختے والے علاقوں میں کراس اوور سگنلز کی تلاش

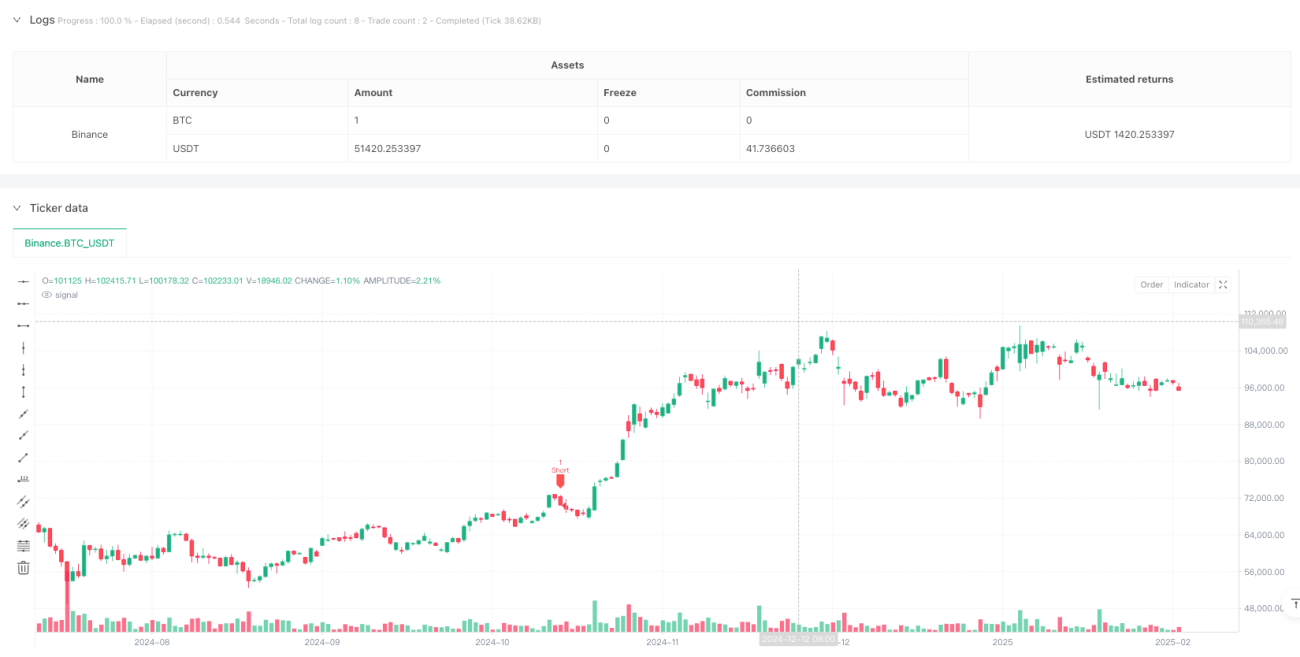

- خریداری کی شرط: موجودہ ٹائم فریم پر K لائن D لائن کو اوپر سے عبور کرے، اور K کی قیمت <20 ہو؛ اعلیٰ ٹائم فریم پر K کی قیمت <20 ہو اور K>D ہو

- فروخت کی شرط: موجودہ ٹائم فریم پر K لائن D لائن کو نیچے سے عبور کرے، اور K کی قیمت >80 ہو؛ اعلیٰ ٹائم فریم پر K کی قیمت >80 ہو اور K<D ہو

- انٹری قیمت پر مبنی متحرک اسٹاپ لاس اور ٹیک پرافٹ سسٹم، جس میں اسٹاپ لاس اور ٹیک پرافٹ کے ملٹی پلز کو ایڈجسٹ کیا جا سکتا ہے

حکمت عملی کے فوائد

- ملٹی ٹائم فریم سگنل کی تصدیق تجارت کی قابل اعتمادی کو بڑھاتی ہے اور جھوٹے سگنلز کو مؤثر طریقے سے کم کرتی ہے

- زیادہ خریدے/زیادہ فروختے والے علاقوں میں تجارت کرنے سے رجحان کے الٹ جانے کے امکانات بڑھ جاتے ہیں

- متحرک اسٹاپ لاس اور ٹیک پرافٹ سسٹم مارکیٹ کے اتار چڑھاؤ کے مطابق خود بخود ایڈجسٹ ہو سکتا ہے، جس سے سرمایہ کے انتظام میں لچک بڑھ جاتی ہے

- گرافیکل انٹرفیس تجارتی سگنلز اور اسٹاپ لاس/ٹیک پرافٹ کی پوزیشنوں کو واضح طور پر دکھاتا ہے، جس سے تاجروں کے لیے سمجھنا اور عمل کرنا آسان ہو جاتا ہے

- حکمت عملی کے پیرامیٹرز کو مختلف مارکیٹ کے حالات کے مطابق ایڈجسٹ کیا جا سکتا ہے

حکمت عملی کے خطرات

- شدید اتار چڑھاؤ والی مارکیٹوں میں اسٹاپ لاس بار بار لگ سکتے ہیں

- دوہرے ٹائم فریم کی تصدیق کی وجہ سے کچھ تجارتی مواقع ضائع ہو سکتے ہیں

- مقررہ ملٹی پل والے اسٹاپ لاس اور ٹیک پرافٹ تمام مارکیٹ کے حالات کے لیے موزوں نہیں ہو سکتے

- مضبوط رجحان میں قبل از وقت ٹیک پرافٹ لگ سکتا ہے

- منافع اور خطرے میں توازن برقرار رکھنے کے لیے پیرامیٹرز کو مناسب طریقے سے سیٹ کرنا ضروری ہے

حکمت عملی کی بہتری کے ممکنہ پہلو

- متحرک اسٹاپ لاس اور ٹیک پرافٹ میکانزم متعارف کرانا، جو مارکیٹ کے اتار چڑھاؤ کے مطابق متحرک طور پر ایڈجسٹ ہو

- رجحان فلٹر شامل کرنا، تاکہ مضبوط رجحان میں تجارتی سمت کو ایڈجسٹ کیا جا سکے

- معاون تصدیقی سگنل کے طور پر حجم کے اشاریے (Volume Indicators) کو شامل کرنا

- زیادہ ذہین پوزیشن مینجمنٹ سسٹم تیار کرنا

- داخلی وقت کو بہتر بنانے کے لیے مارکیٹ کے جذباتی اشاریے (Market Sentiment Indicators) کو شامل کرنے پر غور کرنا

خلاصہ

یہ ایک مکمل تجارتی نظام ہے جس میں تکنیکی تجزیہ اور خطرے کا انتظام یکجا کیا گیا ہے۔ ملٹی ٹائم فریم سگنل کی تصدیق اور متحرک اسٹاپ لاس/ٹیک پرافٹ کے ذریعے، یہ حکمت عملی استحکام کے ساتھ ساتھ اچھی منافع کی صلاحیت بھی فراہم کرتی ہے۔ تاہم، صارفین کو اپنے تجارتی انداز اور مارکیٹ کے حالات کے مطابق پیرامیٹرز کو بہتر بنانا ہوگا اور ہمیشہ سخت خطرے پر قابو رکھنا ہوگا۔

- 1