جائزہ

یہ ایک تجارتی حکمت عملی ہے جو متعدد شماریاتی بینڈز اور رجحان کے تجزیے پر مبنی ہے۔ یہ حکمت عملی بولنگر بینڈز، کوانٹائل بینڈز اور پاور لاء بینڈز کو ملا کر اہم سپورٹ/مزاحمتی علاقوں کی نشاندہی کرتی ہے، اور اوپری کوانٹائل بینڈ کی نچلی معیاری انحراف لائن کو سگنل کے طور پر استعمال کرتی ہے تاکہ داخلے اور باہر نکلنے کے اوقات متعین کیے جا سکیں۔ حکمت عملی میں مارکیٹ کے اتار چڑھاؤ کو مدنظر رکھا گیا ہے اور متعدد شماریاتی طریقوں کے استعمال سے سگنلز کی اعتمادیت بڑھائی گئی ہے۔

حکمت عملی کا اصول

حکمت عملی کا بنیادی اصول متعدد شماریاتی بینڈز کے کراس اوور کے ذریعے مارکیٹ کے رجحان کو پکڑنا ہے۔ اس میں درج ذیل اہم اجزاء شامل ہیں:

- بولنگر بینڈ سسٹم - قیمت کے اتار چڑھاؤ کے وقفے کا تعین کرنے کے لیے، جب قیمت اوپری بینڈ سے تجاوز کرتی ہے تو پیلا انتباہ ظاہر ہوتا ہے۔

- کوانٹائل بینڈ سسٹم - قیمت کے اوپری اور نچلے کوانٹائل کا حساب لگاتا ہے، تاکہ قیمت کی انتہائی اقدار کے امکانات کا اندازہ ہو سکے۔

- پاور لاء بینڈ سسٹم - تاریخی منافع کی بنیاد پر اہمیت کی سطح کا حساب لگاتا ہے، تاکہ زیادہ خریدے جانے یا زیادہ فروخت ہونے کی صورتحال کی پیمائش کی جا سکے۔

- ٹرگر سسٹم - اوپری کوانٹائل بینڈ کی نچلی معیاری انحراف لائن کو بنیادی ٹرگر سگنل کے طور پر استعمال کیا جاتا ہے، قیمت اس لائن سے اوپر رہنے پر تیزی کا اشارہ سمجھا جاتا ہے۔

- تصدیقی نظام - لگاتار تصدیقی کندل کی تعداد مقرر کر کے غلط سگنلز کو فلٹر کیا جاتا ہے۔

حکمت عملی کے فوائد

- سگنلز کی مضبوطی - متعدد شماریاتی بینڈز کا استعمال غلط سگنلز کو مؤثر طریقے سے کم کرتا ہے۔

- موافقت - حکمت عملی مختلف ٹائم فریموں اور مارکیٹ کے حالات کے مطابق ڈھل سکتی ہے۔

- رسک کنٹرول مکمل - متعدد شماریاتی بینڈز کے ذریعے رسک والے علاقوں کو تقسیم کیا جاتا ہے، اور اسٹاپ لوس میکانزم بھی موجود ہے۔

- پیرامیٹرز میں لچک - مختلف مارکیٹ خصوصیات کے مطابق اصلاح کے لیے وسیع پیرامیٹر آپشنز فراہم کیے گئے ہیں۔

- بصری وضاحت - مختلف انڈیکیٹر لائنوں کے رنگ واضح طور پر مختلف ہیں، اور تجارتی سگنلز براہ راست نظر آتے ہیں۔

حکمت عملی کے خطرات

- وقفہ کا خطرہ - شماریاتی انڈیکیٹرز میں کچھ تاخیر ہوتی ہے، جس کی وجہ سے داخلے کا بہترین موقع ہاتھ سے نکل سکتا ہے۔

- سائیڈ ویز مارکیٹ میں نقصان - افقی طور پر چلنے والی مارکیٹ میں بہت زیادہ تجارتی سگنلز پیدا ہو سکتے ہیں۔

- پیرامیٹرز کی حساسیت - مختلف پیرامیٹر امتزاجوں کے نتائج میں بڑا فرق ہوتا ہے، جس کے لیے بار بار اصلاح کی ضرورت ہوتی ہے۔

- حساب کا بوجھ - متعدد شماریاتی انڈیکیٹرز کے ریئل ٹائم حساب کے لیے زیادہ پروسیسنگ پاور درکار ہوتی ہے۔

- مارکیٹ کے ماحول پر انحصار - انتہائی مارکیٹ حالات میں شماریاتی اصول ناکام ہو سکتے ہیں۔

حکمت عملی کی اصلاح کی سمت

- متحرک پیرامیٹرز کا اضافہ - مارکیٹ کے اتار چڑھاؤ کے مطابق خود بخود مختلف پیرامیٹرز کو ایڈجسٹ کرنا۔

- مارکیٹ کے ماحول کا تعین شامل کرنا - سائیڈ ویز مارکیٹ میں سگنلز کو فلٹر کرنے کے لیے رجحان کی شدت کے انڈیکیٹرز شامل کرنا۔

- حساب کی کارکردگی بہتر بنانا - کچھ حساب کے عمل کو آسان بنا کر وسائل کی کھپت کم کرنا۔

- رسک کنٹرول میں بہتری - مزید اسٹاپ لوس شرائط اور پوزیشن مینجمنٹ کی حکمت عملی شامل کرنا۔

- موافقت بڑھانا - خودکار موافقت پذیر پیرامیٹر آپٹیمائزیشن سسٹم تیار کرنا۔

خلاصہ

یہ ایک جامع رجحان پیروی کرنے والی حکمت عملی ہے جو متعدد شماریاتی طریقوں کو یکجا کرتی ہے۔ بولنگر بینڈز، کوانٹائل بینڈز اور پاور لاء بینڈز کے باہمی تعاون سے مارکیٹ کے رجحان کو اچھی طرح پکڑا جا سکتا ہے، اور ساتھ ہی رسک کنٹرول بھی مضبوط ہے۔ اگرچہ اس میں کچھ وقفہ اور پیرامیٹر کی اصلاح میں دشواری ہے، لیکن مسلسل بہتری اور اصلاح کے ذریعے یہ حکمت عملی عملی استعمال اور ترقی کے امکانات رکھتی ہے۔

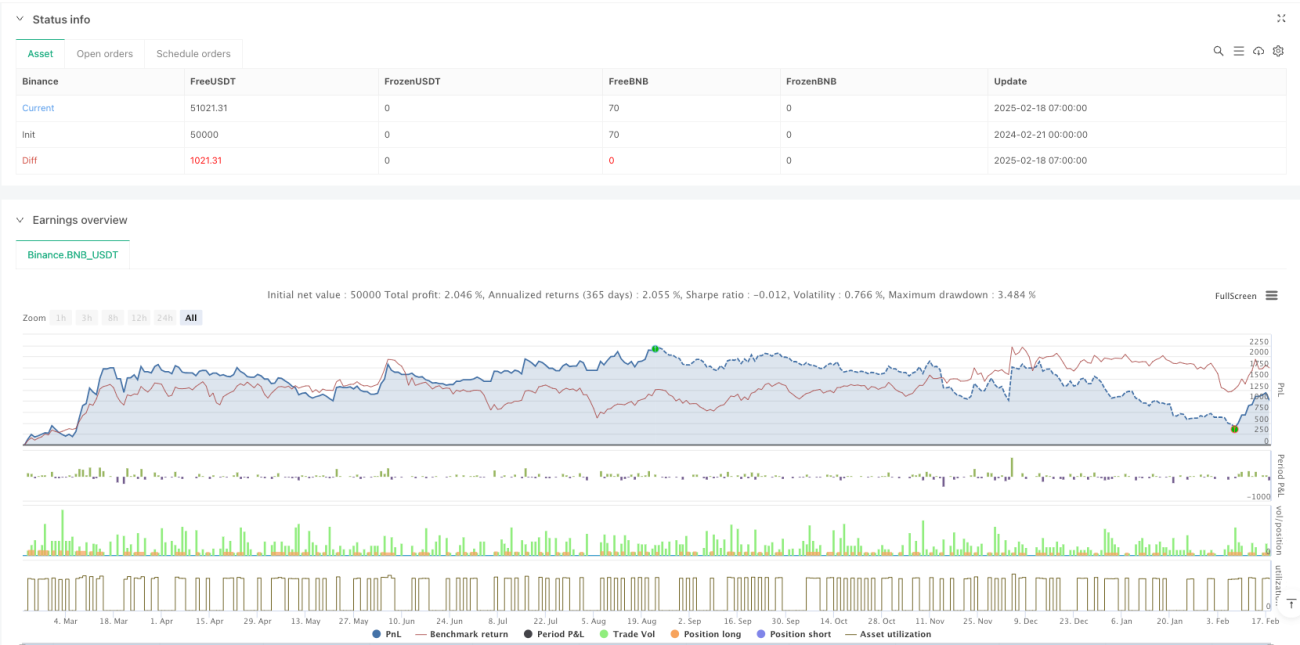

/*backtest

start: 2024-02-21 00:00:00

end: 2025-02-18 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"BNB_USDT"}]

*/

//@version=6

strategy("Multi-Band Comparison Strategy with Separate Entry/Exit Confirmation", overlay=true,

default_qty_type=strategy.percent_of_equity, default_qty_value=10,

initial_capital=5000, currency=currency.USD)- 1