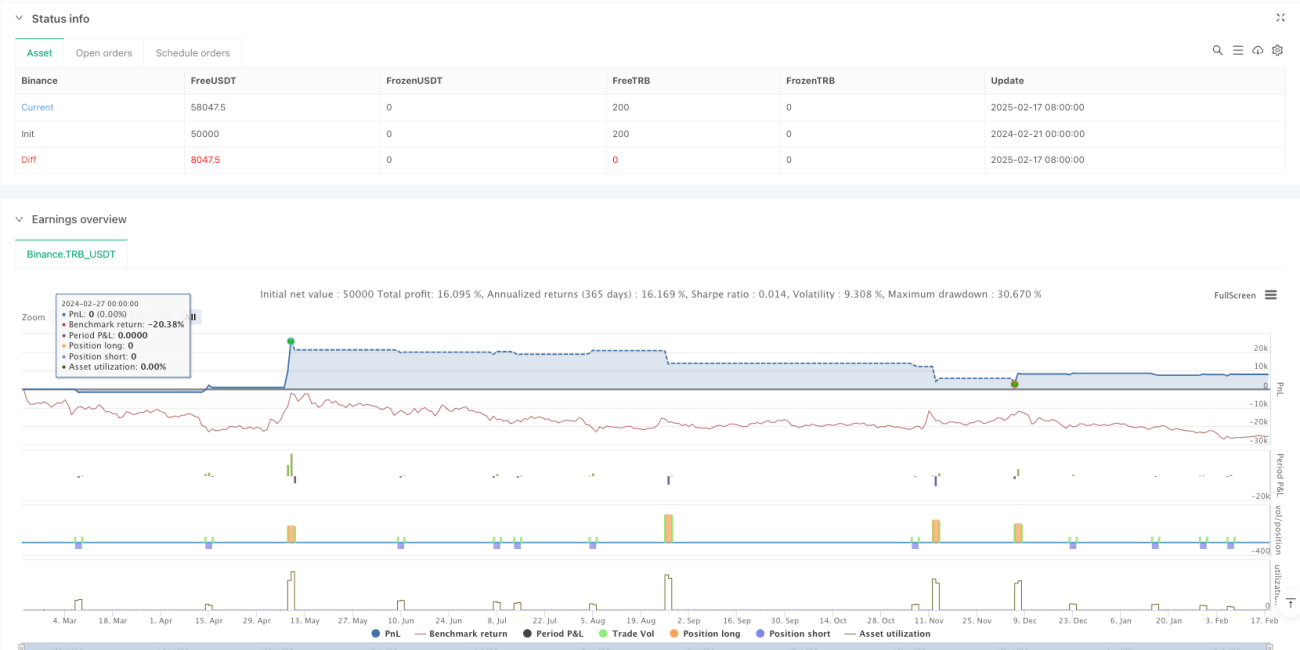

جائزہ

یہ حکمت عملی قیمت کی بریک آؤٹ اور متحرک ٹریلنگ اسٹاپ لاس پر مبنی ایک تجارتی نظام ہے۔ یہ پچھلے N ادوار کی بلند ترین اور کم ترین قیمتوں کی نگرانی کرتا ہے اور جب قیمت ان اہم سطحوں کو عبور کرتی ہے تو تجارت کرتا ہے۔ حکمت عملی ایک ذہین اسٹاپ لاس میکانزم استعمال کرتی ہے، جو صرف 1% منافع حاصل ہونے کے بعد متحرک ہوتا ہے، تاکہ منافع کو پوری طرح ترقی کرنے دیا جا سکے۔ اس کے علاوہ، 1 گھنٹے کے کولنگ آف پیریڈ کے ذریعے زیادہ تجارت سے بچا جاتا ہے اور ہر تجارت کے معیار کو بہتر بنایا جاتا ہے۔

حکمت عملی کا اصول

حکمت عملی کے بنیادی منطق میں درج ذیل اہم حصے شامل ہیں:

- انٹری سگنل: پچھلے N ادوار کی بلند ترین اور کم ترین قیمتوں کا حساب لگا کر، جب موجودہ قیمت ان سطحوں کو عبور کرتی ہے تو تجارتی سگنل متحرک ہوتا ہے۔ لمبی پوزیشن کے لیے قیمت کو پچھلی بلند ترین سے ایک خاص فیصد اوپر جانا ضروری ہے، جبکہ چھوٹی پوزیشن کے لیے پچھلی کم ترین سے نیچے جانا ضروری ہے۔

- تجارت کا انتظام: 1 گھنٹے کا تجارتی کولنگ آف پیریڈ نافذ کیا جاتا ہے تاکہ اتار چڑھاؤ کے دوران بار بار تجارت سے بچا جا سکے۔

- خطرے کا کنٹرول: متحرک ٹریلنگ اسٹاپ لاس استعمال کیا جاتا ہے، جو صرف 1% منافع حاصل ہونے کے بعد فعال ہوتا ہے، جس سے منافع کو بہتر طور پر محفوظ کیا جا سکتا ہے۔

- پیرامیٹر کی اصلاح: کلیدی پیرامیٹرز جیسے کہ بیک لاک پیریڈ، بریک آؤٹ تھریشولڈ، اور اسٹاپ لاس فیصد کو مختلف مارکیٹ حالات کے مطابق ایڈجسٹ کیا جا سکتا ہے۔

حکمت عملی کے فوائد

- متحرک رسک مینجمنٹ: ٹریلنگ اسٹاپ لاس میکانزم کے ذریعے، حکمت عملی منافع کی حفاظت کرتے ہوئے اسے بڑھنے دیتی ہے۔

- لچکدار موافقت: حکمت عملی مختلف مارکیٹ حالات کے مطابق ڈھل سکتی ہے، پیرامیٹرز کو ایڈجسٹ کرکے کارکردگی کو بہتر بنایا جا سکتا ہے۔

- فلٹرنگ میکانزم: تجارتی کولنگ آف پیریڈ کا استعمال زیادہ تجارت سے بچنے اور تجارت کے معیار کو بہتر بنانے کے لیے کیا جاتا ہے۔

- سادہ اور مؤثر: حکمت عملی کی منطق واضح ہے، سمجھنے اور لاگو کرنے میں آسان ہے، اور اچھی توسیع پذیری رکھتی ہے۔

حکمت عملی کے خطرات

- غلط بریک آؤٹ کا خطرہ: مارکیٹ میں غلط بریک آؤٹ ہو سکتے ہیں، جس سے غلط سگنل پیدا ہو سکتے ہیں۔ حجم کی تصدیق شامل کرنے کی سفارش کی جاتی ہے۔

- سلپج کا اثر: زیادہ اتار چڑھاؤ کے دوران، بڑی سلپج کا سامنا ہو سکتا ہے، جو حکمت عملی کی کارکردگی کو متاثر کر سکتا ہے۔

- پیرامیٹر کی حساسیت: حکمت عملی کی کارکردگی پیرامیٹر سیٹنگز کے لیے حساس ہوتی ہے، اس لیے محتاط اصلاح کی ضرورت ہے۔

- مارکیٹ کے ماحول پر انحصار: کم اتار چڑھاؤ والے ماحول میں کارکردگی کمزور ہو سکتی ہے۔

حکمت عملی کی بہتری کے امکانات

- حجم کے اشاریے شامل کرنا: حجم کی تصدیق کے ذریعے بریک آؤٹ سگنلز کی وشوسنییتا کو بہتر بنایا جا سکتا ہے۔

- رجحان فلٹر شامل کرنا: طویل مدتی رجحان کے اشاریوں کے ساتھ ملا کر صرف رجحان کی سمت میں تجارت کی جا سکتی ہے۔

- متحرک پیرامیٹر ایڈجسٹمنٹ: مارکیٹ کے اتار چڑھاؤ کے مطابق بریک آؤٹ تھریشولڈ اور اسٹاپ لاس پیرامیٹرز کو خودکار طور پر ایڈجسٹ کیا جا سکتا ہے۔

- متعدد ٹائم فریم: درستگی بڑھانے کے لیے متعدد ٹائم فریموں کے سگنلز کو یکجا کیا جا سکتا ہے۔

خلاصہ

یہ ایک معقول طور پر ڈیزائن کردہ رجحان پر عمل کرنے والی حکمت عملی ہے، جو قیمت کی بریک آؤٹ اور متحرک اسٹاپ لاس کو ملا کر بڑے رجحانات کو پکڑنے اور خطرے کو مؤثر طریقے سے کنٹرول کرنے کی صلاحیت رکھتی ہے۔ حکمت عملی میں حسب ضرورت کی مضبوط صلاحیت ہے، جسے پیرامیٹر کی اصلاح کے ذریعے مختلف مارکیٹ حالات کے مطابق ڈھالا جا سکتا ہے۔ تجویز ہے کہ لائیو ٹریڈنگ میں چھوٹے حجم سے شروع کریں اور آہستہ آہستہ مختلف مارکیٹ حالات میں حکمت عملی کی کارکردگی کو تصدیق کریں۔

- 1