ذہین کثیر جہتی خودکار رجحان تجارتی نظام

خلاصہ

یہ حکمت عملی ایک جدید تجارتی نظام ہے جو متعدد تکنیکی اشاریوں کو یکجا کرتی ہے۔ Fair Value Gap (FVG)، رجحان کے اشاروں اور قیمت کے رویے کے جامع تجزیے کے ذریعے مارکیٹ کے مواقع کی نشاندہی کرتی ہے۔ یہ نظام دوہری حکمت عملی کے طریقہ کار پر مبنی ہے، جو رجحان کی پیروی اور بینڈ ٹریڈنگ کی خصوصیات کو یکجا کرتا ہے، اور متحرک پوزیشن مینجمنٹ اور متعدد جہتی اخراج کے طریقہ کار کے ذریعے تجارتی کارکردگی کو بہتر بناتا ہے۔ یہ حکمت عملی خاص طور پر رسک کنٹرول پر زور دیتی ہے، اور اتار چڑھاؤ کی فلٹریشن اور تجارتی حجم کی تصدیق کے ذریعے سگنل کے معیار کو بہتر کرتی ہے۔

حکمت عملی کا اصول

حکمت عملی کا بنیادی منطق درج ذیل پہلوؤں پر مبنی ہے:

- FVG خلا کی شناخت - قیمت کے خلاء کے سائز کا حساب لگا کر ممکنہ تجارتی مواقع تلاش کرنا

- رجحان کی تصدیق کا نظام - 200 دن کی موونگ ایوریج، SuperTrend اشاریہ اور MACD کو ملا کر مارکیٹ کے رجحان کی تصدیق کرنا

- ذہین رقم کی تصدیق - RSI کے انتہائی خرید/فروخت، غیر معمولی حجم اور قیمت کے رویے کے پیٹرن کو تجارتی محرک کے طور پر استعمال کرنا

- متحرک پوزیشن مینجمنٹ - ATR پر مبنی اتار چڑھاؤ کے مطابق پوزیشن کا سائز ایڈجسٹ کرنا، تاکہ رسک کی نمائش مستقل رہے

- کثیر سطحی اخراج کا طریقہ کار - ٹریلنگ اسٹاپ اور ٹارگٹ پرافٹ کے امتزاج کے ذریعے تجارت کے اخراج کا انتظام کرنا

حکمت عملی کے فوائد

- اعلیٰ موافقت - حکمت عملی مارکیٹ کے اتار چڑھاؤ کے مطابق خود بخود پیرامیٹرز اور پوزیشنز کو ایڈجسٹ کر سکتی ہے

- مکمل رسک کنٹرول - متعدد فلٹرز اور سخت پوزیشن مینجمنٹ کے ذریعے رسک کو کنٹرول کرنا

- قابل اعتماد سگنل معیار - کثیر جہتی اشاریوں کی تصدیق کے ذریعے تجارتی سگنلز کی درستگی بڑھانا

- لچکدار تجارتی طریقہ - ایک ساتھ رجحانی اور دوغلی مارکیٹ کے مواقع کو پکڑ سکتا ہے

- سائنسی فنڈ مینجمنٹ - فیصدی رسک مینجمنٹ کا استعمال، فنڈز کے استعمال کی معقولیت کو یقینی بنانا

حکمت عملی کے خطرات

- پیرامیٹر حساسیت - متعدد پیرامیٹرز کی ترتیبات حکمت عملی کی کارکردگی کو متاثر کر سکتی ہیں، مسلسل اصلاح کی ضرورت ہے

- مارکیٹ کے ماحول پر انحصار - بعض مارکیٹ حالات میں جھوٹے بریک آؤٹ سگنلز ظاہر ہو سکتے ہیں

- سلپج کا اثر - کم لیکویڈیٹی والی مارکیٹوں میں زیادہ سلپج کا سامنا ہو سکتا ہے

- حسابی پیچیدگی - متعدد اشاریوں کا حساب سگنل میں تاخیر کا سبب بن سکتا ہے

- زیادہ سرمائے کی ضرورت - مکمل عمل درآمد کے لیے بڑے ابتدائی سرمائے کی ضرورت ہے

حکمت عملی کی اصلاح کے سمت

- اشاریوں کے وزن کی اصلاح - مشین لرننگ کے طریقوں کو متعارف کروا کر ہر اشاریے کے وزن کو متحرک طور پر ایڈجسٹ کیا جا سکتا ہے

- مارکیٹ کی موافقت میں اضافہ - مارکیٹ کے اتار چڑھاؤ کے لیے خودکار موافقت کا طریقہ کار شامل کرنا

- سگنل فلٹریشن میں بہتری - مزید مارکیٹ مائیکرو سٹرکچر اشاریوں کو متعارف کرانا

- عمل درآمد کے طریقہ کار کی اصلاح - اثر لاگت کو کم کرنے کے لیے ذہین آرڈر ڈویژن کا طریقہ کار شامل کرنا

- رسک کنٹرول میں اضافہ - متحرک رسک بجٹ مینجمنٹ سسٹم شامل کرنا

خلاصہ

یہ حکمت عملی متعدد تکنیکی اشاریوں اور تجارتی تکنیکوں کے جامع استعمال کے ذریعے ایک مکمل تجارتی نظام تشکیل دیتی ہے۔ اس کا فائدہ مارکیٹ کی تبدیلیوں کے مطابق خود کو ڈھالنے کی صلاحیت ہے، جبکہ سخت رسک کنٹرول کو برقرار رکھتی ہے۔ اگرچہ اصلاح کی گنجائش موجود ہے، لیکن مجموعی طور پر یہ ایک معقول طور پر ڈیزائن کردہ مقداری تجارتی حکمت عملی ہے۔

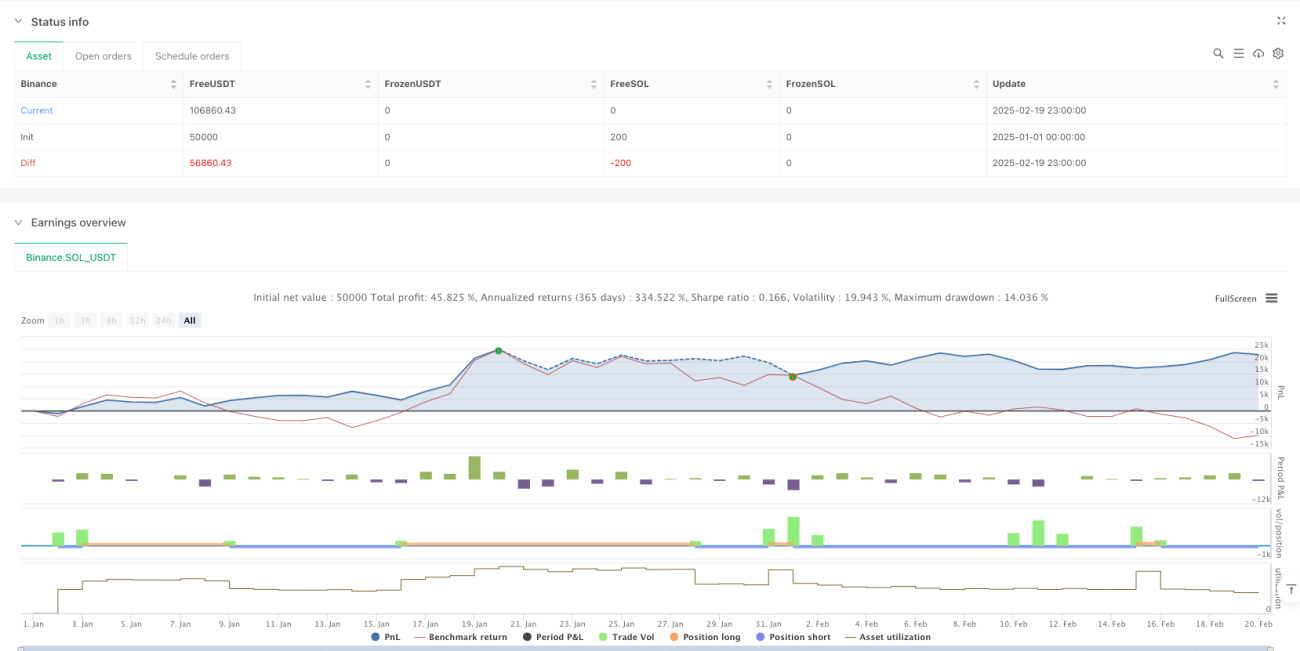

/*backtest

start: 2025-01-01 00:00:00

end: 2025-02-20 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=6

strategy("Adaptive Trend Signals", overlay=true, margin_long=100, margin_short=100, pyramiding=1, initial_capital=50000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075)

// 1. Enhanced Inputs with Debugging Options- 1