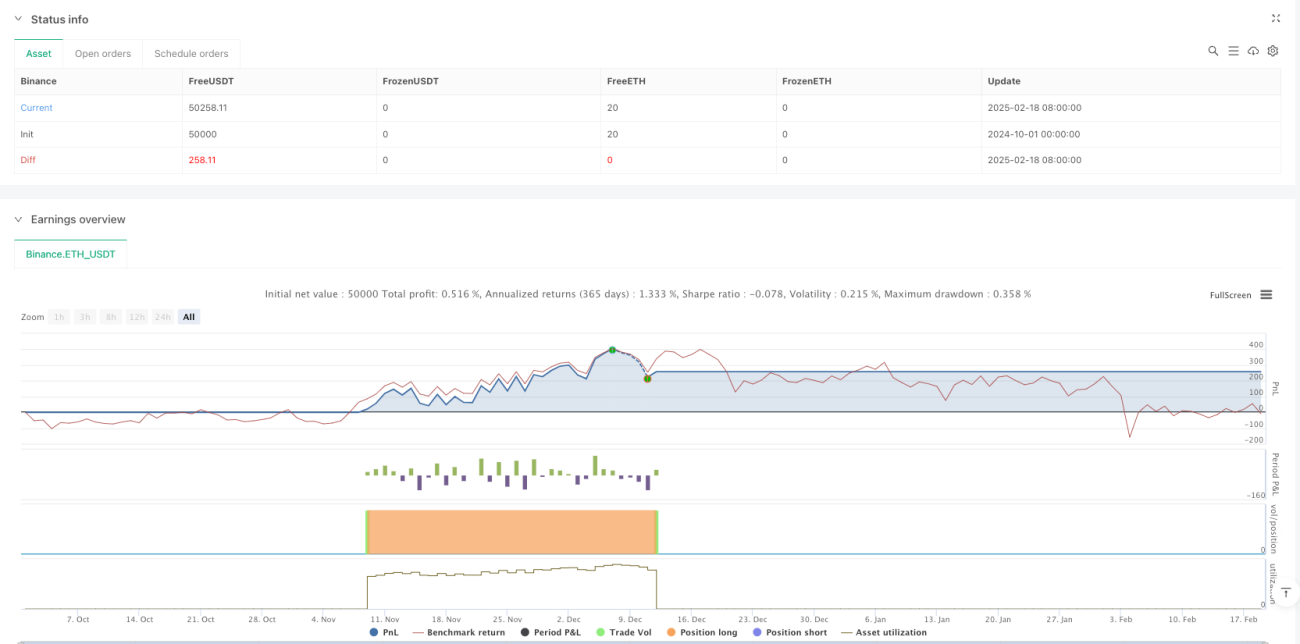

جائزہ

یہ حکمت عملی ڈونچیان چینل (Donchian Channel) کی بریک آؤٹ پر مبنی ٹرینڈ فالو کرنے والا تجارتی نظام ہے، جس میں سپر ٹرینڈ انڈیکیٹر (SuperTrend) اور والیوم فلٹر (Volume Filter) کو شامل کرکے سگنلز کی وشوسنییتا میں اضافہ کیا گیا ہے۔ یہ حکمت عملی بنیادی طور پر قیمت کی تاریخی بلندیوں کو توڑنے کے ذریعے ممکنہ لانگ انٹری مواقع کی نشاندہی کرتی ہے، جبکہ والیوم کی تصدیق اور ٹرینڈ فالو کرنے والے انڈیکیٹرز کا استعمال جھوٹے بریک آؤٹ سگنلز کو فلٹر کرنے کے لیے کیا جاتا ہے۔ اس حکمت عملی کا ڈیزائن لچکدار ہے، جسے مختلف مارکیٹ حالات اور تجارتی مصنوعات کے مطابق پیرامیٹرز کی اصلاح کے ذریعے ڈھالا جا سکتا ہے۔

حکمت عملی کا اصول

حکمت عملی کی بنیادی منطق درج ذیل اہم اجزاء پر مبنی ہے:

- ڈونچیان چینل: صارف کے متعین کردہ مدت کے اندر زیادہ سے زیادہ اور کم سے کم قیمت کا حساب لگایا جاتا ہے، جس سے اوپری بینڈ، نچلا بینڈ اور درمیانی بینڈ تشکیل پاتے ہیں۔ جب قیمت اوپری بینڈ کو توڑتی ہے تو لانگ انٹری کا سگنل متحرک ہوتا ہے۔

- والیوم فلٹر: موجودہ والیوم کا 20 دوروں کی موونگ ایوریج سے موازنہ کرکے یہ یقینی بنایا جاتا ہے کہ انٹری صرف والیوم میں اضافے کے وقت ہو، تاکہ بریک آؤٹ کی وشوسنییتا بڑھ جائے۔

- سپر ٹرینڈ انڈیکیٹر: یہ ٹرینڈ کی تصدیق کرنے والے آلے کے طور پر کام کرتا ہے، لانگ ٹرینڈ میں سبز اور شارٹ ٹرینڈ میں سرخ رنگ دکھاتا ہے۔

- لچکدار اسٹاپ لاس میکانزم: چار مختلف اسٹاپ لاس آپشنز فراہم کیے گئے ہیں، جن میں نچلے بینڈ اسٹاپ، درمیانی بینڈ اسٹاپ، سپر ٹرینڈ اسٹاپ اور فیصدی ٹریلنگ اسٹاپ شامل ہیں۔

حکمت عملی کے فوائد

- متعدد سگنلز کی تصدیق: قیمت کی بریک آؤٹ، والیوم کی تصدیق اور ٹرینڈ انڈیکیٹرز کو ملا کر جھوٹے بریک آؤٹ کے خطرے کو بہت حد تک کم کیا گیا ہے۔

- موافقت کی صلاحیت: پیرامیٹرز میں تبدیلی کے ذریعے اسے مختلف مارکیٹ حالات اور تجارتی ادوار کے مطابق ڈھالا جا سکتا ہے۔

- رسک مینجمنٹ میں بہتری: اسٹاپ لاس کے متعدد اختیارات فراہم کیے گئے ہیں، جو مارکیٹ کی خصوصیات کے مطابق مناسب اسٹاپ لاس طریقہ منتخب کرنے کی اجازت دیتے ہیں۔

- بصری وضاحت: حکمت عملی کا انٹرفیس مختلف انڈیکیٹرز کو واضح طور پر دکھاتا ہے، جس سے تاجر مارکیٹ کی حالت کو سمجھ سکتے ہیں۔

- بیک ٹیسٹنگ میں لچک: صارف بیک ٹیسٹنگ کے لیے وقت کی حد خود متعین کر سکتا ہے، جس سے حکمت عملی کی اصلاح میں آسانی ہوتی ہے۔

حکمت عملی کے خطرات

- اتار چڑھاؤ والی مارکیٹ کا خطرہ: رینج میں اتار چڑھاؤ والی مارکیٹ میں بار بار جھوٹے بریک آؤٹ سگنلز پیدا ہو سکتے ہیں۔

- سلپج کا خطرہ: کم لیکویڈیٹی والی مارکیٹ میں بریک آؤٹ سگنلز کی وجہ سے سلپج کی وجہ سے انٹری قیمت میں فرق آ سکتا ہے۔

- ضرورت سے زیادہ فلٹرنگ کا خطرہ: والیوم فلٹر کو چالو کرنے سے کچھ کارآمد تجارتی مواقع ضائع ہو سکتے ہیں۔

- پیرامیٹرز کی حساسیت: حکمت عملی کے نتائج پیرامیٹرز کی ترتیب سے کافی متاثر ہوتے ہیں، اس لیے محتاط اصلاح کی ضرورت ہے۔

حکمت عملی کی بہتری کے ممکنہ پہلو

- ٹرینڈ کی طاقت کا فلٹر شامل کرنا: ADX جیسے ٹرینڈ کی طاقت کے انڈیکیٹر شامل کیے جا سکتے ہیں، تاکہ صرف مضبوط ٹرینڈ میں انٹری کی جائے۔

- والیوم انڈیکیٹر کی اصلاح: سادہ موونگ ایوریج کی بجائے رشتہ دار والیوم یا والیوم بریک آؤٹ انڈیکیٹر استعمال کیے جا سکتے ہیں۔

- وقت کا فلٹر شامل کرنا: تجارت کے وقت کی حد مقرر کی جا سکتی ہے، تاکہ مارکیٹ میں زیادہ اتار چڑھاؤ والے ادوار سے بچا جا سکے۔

- متحرک پیرامیٹرز کی اصلاح: مارکیٹ کے اتار چڑھاؤ کے مطابق چینل کی مدت اور سپر ٹرینڈ کے پیرامیٹرز خود بخود ایڈجسٹ کیے جا سکتے ہیں۔

- مشین لرننگ کا استعمال: پیرامیٹرز کے انتخاب اور سگنل فلٹرنگ کو بہتر بنانے کے لیے مشین لرننگ الگورتھم استعمال کیے جا سکتے ہیں۔

خلاصہ

یہ حکمت عملی متعدد تکنیکی انڈیکیٹرز کو یکجا کرکے ایک نسبتاً مکمل ٹرینڈ فالو کرنے والا تجارتی نظام تشکیل دیتی ہے۔ اس حکمت عملی کا فائدہ اعلیٰ سگنل وشوسنییتا اور لچکدار رسک مینجمنٹ میں ہے، لیکن تاجر کو مارکیٹ کی مخصوص خصوصیات کے مطابق پیرامیٹرز کی اصلاح کرنے کی ضرورت ہوتی ہے۔ مسلسل بہتری اور اصلاح کے ذریعے، یہ حکمت عملی ٹرینڈ والی مارکیٹ میں مستحکم تجارتی نتائج دینے کی امید رکھتی ہے۔

- 1