جائزہ

یہ حکمت عملی Nasdaq 100 مائیکرو فیوچرز کے لیے ڈیزائن کردہ ایک انٹرا ڈے ٹریڈنگ حکمت عملی ہے۔ اس حکمت عملی کا بنیادی مرکز دوہری مووینگ ایوریج سسٹم ہے جو خرید و فروخت کے اشاروں کی تصدیق کے لیے ویٹڈ اوسط قیمت (VWAP) کے ساتھ مل کر استعمال ہوتا ہے، اور سٹاپ لاس کی پوزیشن کو متحرک طور پر ایڈجسٹ کرنے کے لیے حقیقی اتار چڑھاؤ کی حد (ATR) کا استعمال کرتا ہے۔ یہ حکمت عملی سرمائے کی حفاظت کو یقینی بناتے ہوئے سخت رسک مینجمنٹ اور متحرک پوزیشن سائزنگ کے ذریعے مارکیٹ کے رجحانات کو پکڑنے کی کوشش کرتی ہے۔

حکمت عملی کا اصول

یہ حکمت عملی درج ذیل بنیادی اجزاء پر مبنی ہے:

- سگنل سسٹم 9 اور 21 پیریڈز کے ایکسپونینشل مووینگ ایوریج (EMA) کے کراس اوور کو رجحان کی سمت شناخت کرنے کے لیے استعمال کرتا ہے۔ جب قلیل مدتی اوسط طویل مدتی اوسط کو اوپر سے عبور کرتی ہے تو خرید کا سگنل پیدا ہوتا ہے، اور اس کے برعکس فروخت کا سگنل پیدا ہوتا ہے۔

- VWAP کو رجحان کی تصدیق کے اشارے کے طور پر استعمال کیا جاتا ہے۔ خرید کی پوزیشن کھولنے کے لیے قیمت کا VWAP سے اوپر ہونا ضروری ہے، اور فروخت کی پوزیشن کھولنے کے لیے قیمت کا VWAP سے نیچے ہونا ضروری ہے۔

- رسک مینجمنٹ سسٹم ATR پر مبنی متحرک سٹاپ لاس استعمال کرتا ہے۔ خرید پوزیشن کے لیے سٹاپ لاس 2 گنا APR، اور فروخت پوزیشن کے لیے 1.5 گنا ATR پر سیٹ کیا جاتا ہے۔

- منافع کا ہدف غیر متناسب ڈیزائن کیا گیا ہے، خرید پوزیشن کے لیے 3:1 کا رسک ریوارڈ تناسب اور فروخت پوزیشن کے لیے 2:1 کا تناسب استعمال ہوتا ہے۔

- ٹریلنگ سٹاپ اور بریک ایون سٹاپ کا میکانزم لاگو کیا گیا ہے۔ جب قیمت ہدف منافع کے 50% تک پہنچ جاتی ہے، تو سٹاپ لاس کو لاگت کی سطح پر منتقل کر دیا جاتا ہے۔

حکمت عملی کے فوائد

- متحرک موافقت - ATR کے ذریعے سٹاپ لاس اور ٹریلنگ سٹاپ پیرامیٹرز کو ایڈجسٹ کرتے ہوئے، حکمت عملی خود بخود مختلف مارکیٹ کے اتار چڑھاؤ والے ماحول میں ڈھل سکتی ہے۔

- مکمل رسک کنٹرول - ہر ٹریڈ کے لیے رسک $1500 تک محدود ہے، اور ہفتہ وار زیادہ سے زیادہ نقصان $7500 مقرر کیا گیا ہے۔

- غیر متناسب منافع کا ڈیزائن - مارکیٹ کی خصوصیات کو مدنظر رکھتے ہوئے، خرید و فروخت کی حکمت عملیوں میں مختلف رسک ریوارڈ تناسب اور پوزیشن سائز استعمال کیے جاتے ہیں، جو مارکیٹ کی حقیقت کے مطابق زیادہ موزوں ہے۔

- متعدد تصدیقی میکانزم - EMA کراس اوور اور VWAP کی تصدیق کو ملا کر جھوٹے بریک آؤٹ سگنلز کو مؤثر طریقے سے کم کیا جاتا ہے۔

- مکمل سٹاپ سسٹم - فکسڈ سٹاپ، ٹریلنگ سٹاپ اور بریک ایون سٹاپ کے تینوں تحفظات شامل ہیں۔

حکمت عملی کے خطرات

- سائیڈ ویز مارکیٹ کا خطرہ - سائیڈ ویز مارکیٹ میں، مووینگ ایوریج کراس اوور سگنلز کثرت سے جھوٹے اشارے پیدا کر سکتے ہیں۔

- سلپیج کا خطرہ - تیزی سے چلنے والی مارکیٹ میں، حقیقی ٹریڈنگ قیمت اور سگنل قیمت کے درمیان بڑا فرق ہو سکتا ہے۔

- نظامی خطرہ - جب مارکیٹ میں کوئی بڑا واقعہ پیش آتا ہے، تو سٹاپ لاس کام نہ کر سکے۔

- حد سے زیادہ ٹریڈنگ کا خطرہ - بار بار سگنلز کی وجہ سے ٹریڈنگ کے اخراجات بڑھ سکتے ہیں۔

- سرمائے کے انتظام کا خطرہ - اگر ابتدائی سرمایہ کم ہو تو پوزیشن سائزنگ کا مکمل منصوبہ مؤثر طریقے سے لاگو نہیں کیا جا سکتا۔

حکمت عملی کی بہتری کے ممکنہ پہلو

- والیوم فلٹر متعارف کرانا - والیوم کی تصدیق کا میکانزم شامل کیا جا سکتا ہے، تاکہ صرف اس وقت ٹریڈ کی جائے جب والیوم شرائط پوری کرتا ہو۔

- ٹائم فلٹر کی اصلاح - مخصوص ٹریڈنگ ٹائم ونڈو شامل کرنے پر غور کیا جائے، تاکہ زیادہ اتار چڑھاؤ والے اوپن اور کلوز کے اوقات سے بچا جا سکے۔

- متحرک پیرامیٹر ایڈجسٹمنٹ - مختلف مارکیٹ کے ماحول کے مطابق مووینگ ایوریج پیریڈز اور ATR کے ضربوں کو خود بخود ایڈجسٹ کیا جا سکتا ہے۔

- مارکیٹ جذبات کے اشاریے شامل کرنا - VIX جیسے اتار چڑھاؤ کے اشاریوں کو شامل کر کے ٹریڈنگ کی فریکوئنسی اور پوزیشن سائز کو ایڈجسٹ کیا جا سکتا ہے۔

- ٹریلنگ سٹاپ کو بہتر بنانا - ایک زیادہ لچکدار ٹریلنگ سٹاپ الگورتھم ڈیزائن کیا جا سکتا ہے، جس سے رجحان کو پکڑنے کی صلاحیت بہتر ہوگی۔

خلاصہ

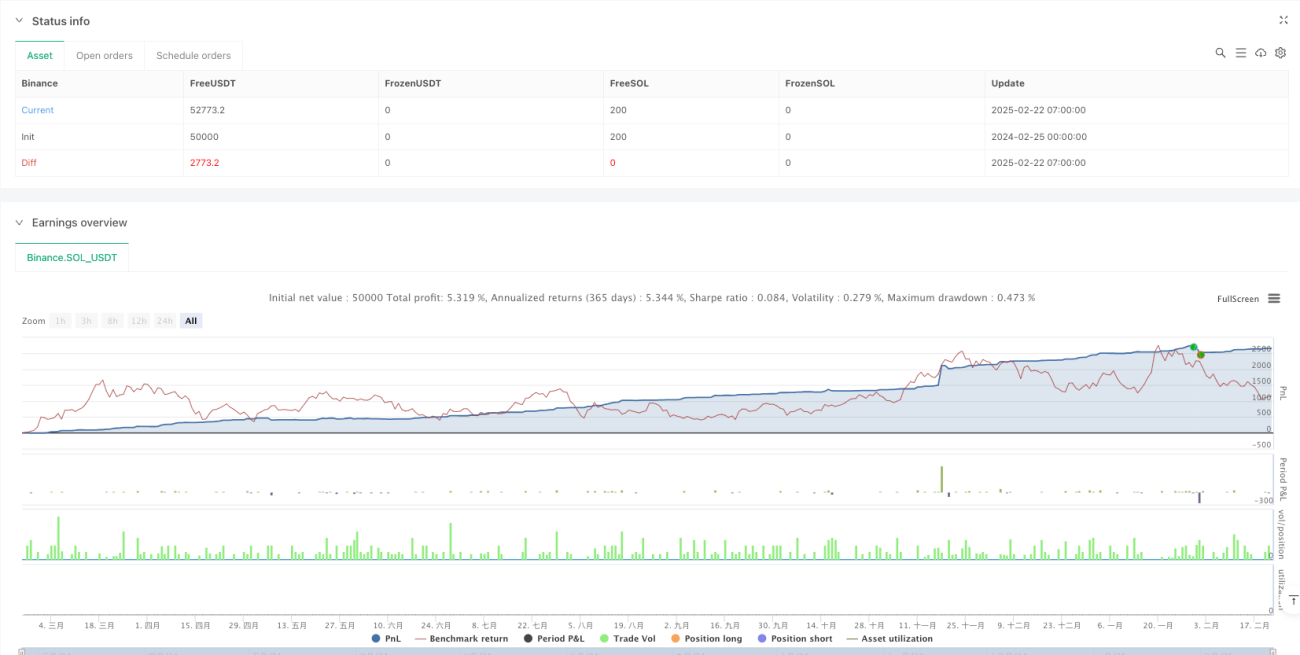

یہ حکمت عملی مووینگ ایوریج سسٹم اور VWAP کے امتزاج سے ایک مضبوط رجحان کی پیروی کا نظام تشکیل دیتی ہے، اور متعدد سطحوں کے رسک کنٹرول میکانزم کے ذریعے سرمائے کی حفاظت کرتی ہے۔ حکمت عملی کی سب سے بڑی خوبی اس کی موافقت اور رسک مینجمنٹ کی صلاحیت ہے۔ ATR کے ذریعے مختلف پیرامیٹرز کو متحرک طور پر ایڈجسٹ کر کے، یہ حکمت عملی مختلف مارکیٹ کے حالات میں مستحکم کارکردگی دکھا سکتی ہے۔ یہ حکمت عملی خاص طور پر Nasdaq 100 مائیکرو فیوچرز کی انٹرا ڈے ٹریڈنگ کے لیے موزوں ہے، لیکن تاجر کو رسک کنٹرول کے قواعد پر سختی سے عمل کرنا ہوگا اور مارکیٹ کی تبدیلیوں کے مطابق پیرامیٹرز کو بروقت ایڈجسٹ کرنا ہوگا۔

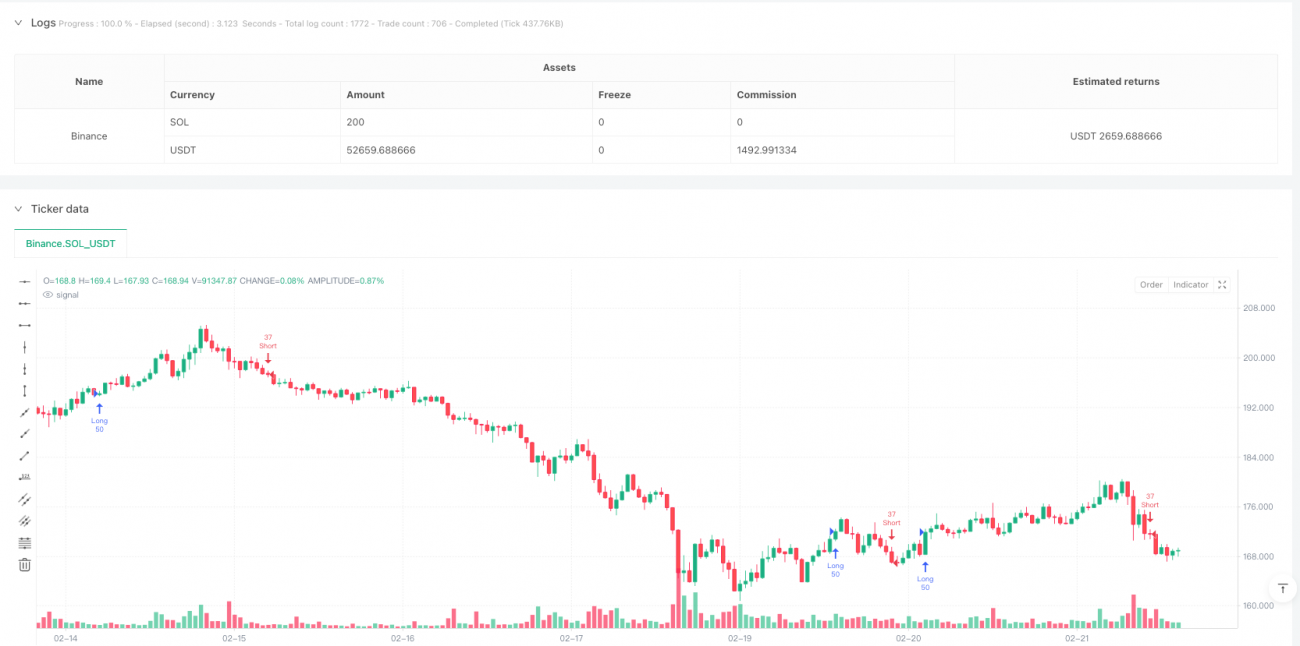

/*backtest

start: 2024-02-25 00:00:00

end: 2025-02-22 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("Nasdaq 100 Micro - Optimized Risk Management", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// === INPUTS ===- 1