جائزہ

ملٹی انڈیکیٹر ویٹڈ انٹیلیجنٹ ٹریڈنگ اسٹریٹیجی ایک جامع مقداری (Quantitative) تجارتی نظام ہے جو متعدد تکنیکی اشاروں کے سگنلز کو یکجا کرکے اور مختلف وزن تفویض کرکے تجارتی فیصلے تیار کرتا ہے۔ یہ حکمت عملی مختلف تکنیکی تجزیہ کے اوزاروں جیسے MACD، سٹوکاسٹک RSI، EMA، سپر ٹرینڈ اور موونگ ایوریج کراس اوور کو ملا کر ایک مکمل تجارتی فریم ورک تشکیل دیتی ہے۔ یہ نظام نہ صرف کثیر سطحی منافع حصول (Take Profit) اور متحرک نقصان روکنے (Stop Loss) کے طریقہ کار کو سپورٹ کرتا ہے بلکہ مارکیٹ کے حالات کے مطابق خود بخود تجارتی پیرامیٹرز کو ایڈجسٹ کرتا ہے، جس سے یہ مختلف مارکیٹ ماحول میں اعلیٰ موافقت برقرار رکھتا ہے۔ یہ حکمت عملی خاص طور پر درمیانی سے طویل مدتی تاجروں کے لیے موزوں ہے، وزن کی تقسیم کا نظام تجارتی فیصلوں کو زیادہ مستحکم اور قابل اعتماد بناتا ہے۔

حکمت عملی کا اصول

اس حکمت عملی کا مرکز اس کا وزنی سگنل سسٹم ہے، جو پانچ مختلف ذیلی حکمت عملیوں کے ذریعے تجارتی سگنل تیار کرتا ہے:

-

MACD حکمت عملی: MACD لائن اور سگنل لائن کے کراس اوور کا استعمال کرکے مارکیٹ کی رجحان کی سمت کا تعین کرتا ہے۔ جب MACD لائن سگنل لائن کو اوپر سے کراس کرتی ہے تو خرید کا سگنل پیدا ہوتا ہے، اور جب نیچے سے کراس کرتی ہے تو فروخت کا سگنل پیدا ہوتا ہے۔

-

سٹوکاسٹک RSI حکمت عملی: RSI اور سٹوکاسٹک انڈیکیٹر کی خوبیوں کو ملا کر مارکیٹ کی حد سے زیادہ خرید (Overbought) یا حد سے زیادہ فروخت (Oversold) کی حالتوں کی نگرانی کرتا ہے۔ جب سٹوکاسٹک RSI مقرر کردہ حد سے زیادہ فروخت کی سطح سے نیچے ہوتا ہے تو خرید کا سگنل پیدا ہوتا ہے، اور جب حد سے زیادہ خرید کی سطح سے اوپر ہوتا ہے تو فروخت کا سگنل پیدا ہوتا ہے۔

-

EMA حد سے زیادہ خرید/فروخت کی حکمت عملی: قیمت کی اوسط سے انحراف کی مقدار کی شناخت کے لیے EMA کا استعمال کرتا ہے۔ جب RSI مقرر کردہ حد سے زیادہ فروخت کی سطح سے نیچے ہوتا ہے تو خرید کا سگنل پیدا ہوتا ہے، اور جب حد سے زیادہ خرید کی سطح سے اوپر ہوتا ہے تو فروخت کا سگنل پیدا ہوتا ہے۔

-

سپر ٹرینڈ حکمت عملی: ATR کے ضرب کی بنیاد پر قیمت چینل سیٹ کرتا ہے اور رجحان کی تبدیلی کے ذریعے تجارتی سمت کا تعین کرتا ہے۔ جب سپر ٹرینڈ انڈیکیٹر منفی سے مثبت ہوتا ہے تو خرید کا سگنل پیدا ہوتا ہے، اور جب مثبت سے منفی ہوتا ہے تو فروخت کا سگنل پیدا ہوتا ہے۔

-

موونگ ایوریج کراس اوور حکمت عملی: دو مختلف ادوار کی موونگ ایوریج کے کراس اوور کا استعمال کرکے مارکیٹ کے رجحان کا تعین کرتا ہے۔ جب قلیل مدتی اوسط طویل مدتی اوسط کو اوپر سے کراس کرتی ہے تو خرید کا سگنل پیدا ہوتا ہے، اور جب نیچے سے کراس کرتی ہے تو فروخت کا سگنل پیدا ہوتا ہے۔

یہ حکمت عملی اپنی مرضی کے مطابق ترتیب دینے کے قابل وزن کے نظام کے ذریعے ہر ذیلی حکمت عملی کے سگنلز کا وزنی حساب لگاتی ہے۔ تجارت صرف اس وقت شروع ہوتی ہے جب وزنی مجموعہ مقرر کردہ حد سے تجاوز کر جاتا ہے۔ اس کے علاوہ، حکمت عملی میں ممکنہ چوٹی اور نیچے (Top/Bottom) کی شناخت کا طریقہ کار بھی شامل ہے، جو مارکیٹ کے ممکنہ الٹ جانے پر پوزیشن کو ایڈجسٹ کر سکتا ہے۔

سگنل کی تصدیق کا یہ کثیر سطحی طریقہ کار غلط سگنلز کو مؤثر طریقے سے کم کرتا ہے اور تجارتی نظام کی وشوسنییتا کو بڑھاتا ہے، جبکہ لچکدار پیرامیٹر سیٹنگز اس حکمت عملی کو مختلف تجارتی مصنوعات اور وقت کے فریموں کے مطابق ڈھالنے کے قابل بناتی ہیں۔

حکمت عملی کے فوائد

-

سگنل کی متعدد تصدیق: پانچ آزاد تکنیکی اشاروں سے پیدا ہونے والے سگنلز کا وزنی حساب لگایا جاتا ہے، جس سے کسی ایک اشارے کی وجہ سے پیدا ہونے والی گمراہی کم ہوتی ہے اور تجارتی سگنلز کے معیار اور وشوسنییتا میں اضافہ ہوتا ہے۔

-

خود انطباقی وزن کا نظام: ہر ذیلی حکمت عملی کو مختلف وزن تفویض کیے جا سکتے ہیں، جس سے تاجر اپنے مختلف اشاروں پر اعتماد اور تاریخی کارکردگی کی بنیاد پر حکمت عملی کے فوکل پوائنٹ کو ایڈجسٹ کر سکتے ہیں، جس سے حکمت عملی کی لچک میں اضافہ ہوتا ہے۔

-

مکمل رسک مینجمنٹ: حکمت عملی میں خطرے پر قابو پانے کے کثیر سطحی طریقہ کار شامل ہیں، بشمول نقصان روکنے (Stop Loss)، کثیر سطحی منافع حصول (Take Profit) اور متحرک طور پر نقصان روکنے کی سطح کو ایڈجسٹ کرنے کی صلاحیت، جو اس بات کو یقینی بناتا ہے کہ مارکیٹ میں منفی تبدیلی کی صورت میں خطرے پر فوری قابو پایا جا سکے۔

-

خودکار ممکنہ چوٹی اور نیچے کی شناخت: RSI، تجارتی حجم اور قیمت کی رفتار کے جامع تجزیے کے ذریعے، حکمت عملی مارکیٹ کی ممکنہ چوٹیوں اور نیچوں کی شناخت کر سکتی ہے اور مناسب وقت پر جزوی طور پر پوزیشن بند کر سکتی ہے، منافع کو محفوظ بنا سکتی ہے یا نقصان کو کم کر سکتی ہے۔

-

اعلیٰ درجے کی حسب ضرورت: تقریباً تمام پیرامیٹرز کو ایڈجسٹ کیا جا سکتا ہے، بشمول ہر اشارے کے حساب کا دورانیہ، وزن کی قدریں، منافع حصول اور نقصان روکنے کے فیصد وغیرہ، جس سے تاجر اپنے ذاتی انداز اور مختلف مارکیٹ کے حالات کے مطابق حکمت عملی کو بہتر بنا سکتے ہیں۔

-

بلٹ ان تاخیر کا طریقہ کار: تجارت میں جلدی داخل ہونے یا شور والے سگنلز کی بنیاد پر تجارت کرنے سے بچنے کے لیے، حکمت عملی میں تاخیر کی تصدیق کا طریقہ کار استعمال کیا گیا ہے، جس سے یہ یقینی بنایا جاتا ہے کہ صرف مستقل سگنلز ہی تجارت کا باعث بنیں، جس سے قلیل مدتی اتار چڑھاؤ کے اثرات کم ہوتے ہیں۔

-

وقتی فلٹر کی خصوصیت: حکمت عملی تجارت کی شروع اور ختم ہونے کی تاریخ مقرر کرنے کی اجازت دیتی ہے، جس سے تاجر مخصوص وقت کے ادوار میں تاریخی ڈیٹا پر کارکردگی کا جائزہ لے سکتے ہیں، یا مارکیٹ میں معروف غیر معمولی اتار چڑھاؤ کے ادوار سے بچ سکتے ہیں۔

حکمت عملی کے خطرات

-

پیرامیٹر کی حد سے زیادہ اصلاح کا خطرہ: پیرامیٹرز کی زیادتی کی وجہ سے، تاریخی ڈیٹا کے ساتھ حد سے زیادہ فٹنگ کا خطرہ ہے، جس کی وجہ سے حقیقی تجارت میں حکمت عملی کی کارکردگی خراب ہو سکتی ہے۔ حل یہ ہے کہ متعدد وقت کے فریموں اور مصنوعات پر بیک ٹیسٹ کیا جائے، نسبتاً مستحکم پیرامیٹر سیٹنگز استعمال کی جائیں اور مخصوص تاریخی ڈیٹا کے لیے حد سے زیادہ اصلاح سے گریز کیا جائے۔

-

مارکیٹ کے حالات میں تبدیلی کا خطرہ: رجحانی مارکیٹ اور سائیڈ ویز مارکیٹ میں حکمت عملی کی کارکردگی میں فرق ہو سکتا ہے، مارکیٹ کی حالت میں اچانک تبدیلی حکمت عملی کی تاثیر کو کم کر سکتی ہے۔ حل یہ ہے کہ مارکیٹ کے ماحول کی شناخت کا طریقہ کار متعارف کرایا جائے اور مختلف مارکیٹ کے حالات میں پیرامیٹرز کو ایڈجسٹ کیا جائے یا تجارت کو روک دیا جائے۔

-

سگنل کے تضاد کا خطرہ: ایک ساتھ متعدد اشاروں کے استعمال سے متضاد سگنلز پیدا ہو سکتے ہیں، جس سے فیصلے میں ابہام پیدا ہو سکتا ہے۔ حل یہ ہے کہ ہر اشارے کے وزن کو معقول طور پر مقرر کیا جائے، زیادہ قابل اعتماد اشاروں پر زور دیا جائے، اور اس بات کو یقینی بنایا جائے کہ سگنل کی حد معقول طور پر مقرر کی گئی ہے تاکہ تضاد کے امکانات کم ہوں۔

-

منی مینجمنٹ کے نامناسب ہونے کا خطرہ: اگرچہ حکمت عملی میں نقصان روکنے کا طریقہ کار شامل ہے، لیکن نامناسب منی مینجمنٹ تیزی سے سرمائے کو ختم کر سکتی ہے۔ حل یہ ہے کہ ہر تجارت کے سرمائے کے تناسب کو سختی سے کنٹرول کیا جائے، اس بات کو یقینی بناتے ہوئے کہ ایک تجارت میں زیادہ سے زیادہ خطرہ قابل برداشت حد میں ہو۔

-

تکنیکی خرابی کا خطرہ: خودکار تجارتی نظام کو نیٹ ورک میں رکاوٹ، ڈیٹا میں تاخیر جیسے تکنیکی مسائل کا سامنا ہو سکتا ہے۔ حل یہ ہے کہ دستی مداخلت کا طریقہ کار ترتیب دیا جائے، نظام کی کارکردگی کی باقاعدگی سے نگرانی کی جائے، اور غیر معمولی حالات سے بروقت نمٹا جائے۔

حکمت عملی کی بہتری کی سمتیں

-

مارکیٹ ماحول کا فلٹر شامل کرنا: ایک ایسا اشارہ تیار کرنا جو موجودہ مارکیٹ کی رجحانی یا سائیڈ ویز حالت کی شناخت کر سکے، اور اس کے مطابق ہر ذیلی حکمت عملی کے وزن کو متحرک طور پر ایڈجسٹ کرے، رجحانی مارکیٹ میں رجحان کی پیروی کرنے والی حکمت عملیوں کو مضبوط کرے اور سائیڈ ویز مارکیٹ میں سوئنگ حکمت عملیوں کو مضبوط کرے۔

-

مشین لرننگ آپٹیمائزیشن متعارف کرانا: مشین لرننگ ٹیکنالوجی کا استعمال کرکے خود بخود ہر اشارے کے پیرامیٹرز اور وزن کو ایڈجسٹ کیا جائے، تاکہ حکمت عملی تازہ ترین مارکیٹ ڈیٹا کے مطابق مسلسل سیکھ اور ڈھل سکے، جس سے حکمت عملی کی متحرک موافقت کی صلاحیت بہتر ہو۔

-

تجارتی حجم کا تجزیہ بڑھانا: تجارتی حجم میں تبدیلی کو اضافی تصدیقی سگنل کے طور پر شامل کیا جائے، اور صرف متوقع حجم کی حمایت حاصل ہونے پر ہی تجارت کی جائے، جس سے سگنل کی وشوسنییتا میں اضافہ ہو۔

-

ممکنہ چوٹی اور نیچے کی شناخت کے الگورتھم کو بہتر بنانا: موجودہ چوٹی اور نیچے کی شناخت کی منطق کو بہتر بنایا جائے، اس میں مزید تصدیقی عوامل جیسے قیمت کی شکلیں، کثیر دورانیے کی تصدیق وغیرہ شامل کی جائیں، تاکہ شناخت کی درستگی بہتر ہو۔

-

جذباتی اشارے شامل کرنا: مارکیٹ کے جذباتی اشارے جیسے خوف کا اشاریہ (VIX)، کال/پٹ آپشن کا تناسب وغیرہ کو مربوط کیا جائے، اور انتہائی مارکیٹ جذبات کی صورت میں تجارتی حکمت عملی کو ایڈجسٹ کیا جائے یا تجارت کو روک دیا جائے، تاکہ زیادہ اتار چڑھاؤ کے دور میں حد سے زیادہ تجارت سے بچا جا سکے۔

-

متحرک منافع حصول اور نقصان روکنے کا طریقہ کار تیار کرنا: مارکیٹ کے اتار چڑھاؤ کے مطابق خود بخود منافع حصول اور نقصان روکنے کی سطحوں کو ایڈجسٹ کیا جائے، زیادہ اتار چڑھاؤ والی مارکیٹ میں نقصان روکنے کی حد کو وسیع کیا جائے اور کم اتار چڑھاؤ والی مارکیٹ میں اسے تنگ کیا جائے، جس سے رسک مینجمنٹ زیادہ لچکدار اور مؤثر ہو۔

-

وقت کے دورانیے کی اصلاح: کثیر وقتی دورانیے کے تجزیے کی خصوصیت شامل کی جائے، جس میں اعلیٰ اور نچلی سطح کے دونوں وقت کے فریموں سے سگنل کی تصدیق کی ضرورت ہو، جس سے جھوٹے بریک آؤٹ اور جھوٹے سگنلز کم ہوں۔

خلاصہ

ملٹی انڈیکیٹر ویٹڈ انٹیلیجنٹ ٹریڈنگ اسٹریٹیجی متعدد تکنیکی تجزیہ کے اوزاروں کو یکجا کرکے اور مختلف وزن تفویض کرکے ایک جامع اور لچکدار تجارتی نظام تشکیل دیتی ہے۔ یہ حکمت عملی نہ صرف سگنل کی متعدد تصدیق، خود انطباقی وزن کے نظام اور مکمل رسک مینجمنٹ کی خصوصیات رکھتی ہے بلکہ اس میں خودکار ممکنہ چوٹی اور نیچے کی شناخت کا طریقہ کار بھی شامل ہے، جو اسے پیچیدہ اور تبدیل ہونے والے مارکیٹ ماحول میں مضبوط موافقت کی صلاحیت دکھانے کے قابل بناتا ہے۔

اگرچہ پیرامیٹر کی حد سے زیادہ اصلاح، مارکیٹ کے حالات میں تبدیلی اور سگنل کے تضاد جیسے ممکنہ خطرات موجود ہیں، لیکن مناسب پیرامیٹر سیٹنگز، مارکیٹ کے ماحول کی شناخت اور سخت منی مینجمنٹ کے ذریعے ان خطرات پر مؤثر طریقے سے قابو پایا جا سکتا ہے۔ مستقبل میں بہتری کی سمتیں مارکیٹ ماحول کا فلٹر شامل کرنا، مشین لرننگ ٹیکنالوجی متعارف کرانا، تجارتی حجم کے تجزیے کو بڑھانا اور ممکنہ چوٹی اور نیچے کی شناخت کے الگورتھم کو بہتر بنانا وغیرہ شامل ہیں، یہ بہتری حکمت عملی کے استحکام اور منافع کی صلاحیت کو مزید بہتر بنائے گی۔

ان سرمایہ کاروں کے لیے جو منظم تجارتی طریقے تلاش کر رہے ہیں، یہ ملٹی انڈیکیٹر ویٹڈ انٹیلیجنٹ ٹریڈنگ اسٹریٹیجی ایک قابل غور فریم ورک فراہم کرتی ہے۔ یہ نہ صرف تجارتی فیصلوں پر جذباتی عوامل کے اثرات کو کم کر سکتی ہے بلکہ ڈیٹا پر مبنی طریقے سے تجارتی کارکردگی کو مسلسل بہتر بنا سکتی ہے۔ اس حکمت عملی کو نافذ کرتے وقت، قدامت پسند پیرامیٹر سیٹنگز سے شروع کرنے، آہستہ آہستہ ایڈجسٹ کرنے اور حکمت عملی کی کارکردگی کی قریب سے نگرانی کرنے کی سفارش کی جاتی ہے تاکہ ذاتی خطرے کی برداشت اور مارکیٹ کے حالات کے لیے موزوں ترین ترتیب تلاش کی جا سکے۔

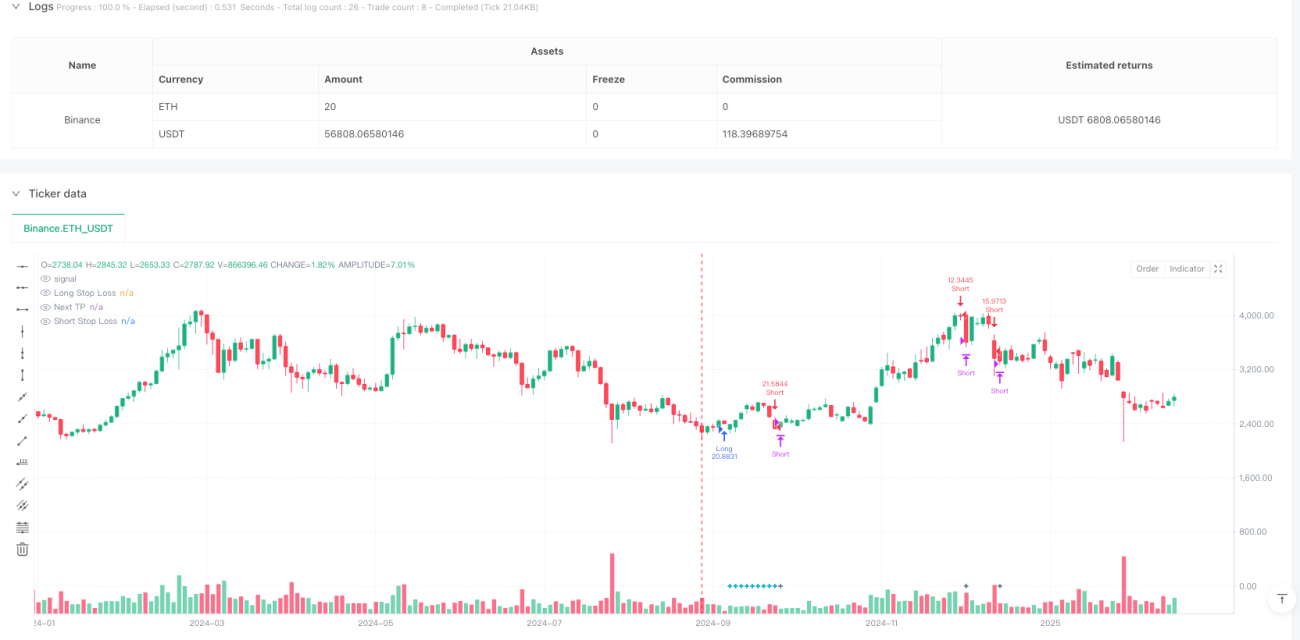

/*backtest

start: 2024-09-08 00:00:00

end: 2025-02-23 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

// **********************************************************************************************************************************************************************************************************************************************************************

// Last update: 08/03/2022

// *************************************************************************************************************************************************************************************************************************************************************************

//@version=5- 1