حکمت عملی کا جائزہ

اوپننگ رینج بریک آؤٹ ATR ٹریلنگ اسٹاپ لاس حکمت عملی ایک مقداری تجارتی نظام ہے جو اوپننگ رینج بریک آؤٹ (ORB) اور اسمارٹ منی کانسیپٹس (Smart Money Concepts) کو یکجا کرتا ہے۔ یہ حکمت عملی امریکی اسٹاک مارکیٹ کے افتتاح کے بعد پہلے 5 منٹ (09:30-09:35 EST) میں بننے والی قیمت کی حد سے بریک آؤٹ کے مواقعوں پر توجہ مرکوز کرتی ہے، اور متعدد فلٹرنگ میکانزم کے ذریعے تجارتی سگنلز کے معیار کو یقینی بناتی ہے۔ یہ نظام فوری یا ریٹریسمنٹ انٹری کو سپورٹ کرتا ہے، رسک سے ریوارڈ ریشیو کی متحرک ایڈجسٹمنٹ کا استعمال کرتا ہے، اور منافع کے انتظام کو بہتر بنانے کے لیے ATR (Average True Range) ٹریلنگ اسٹاپ لاس کا انتخاب کرسکتا ہے۔ اس حکمت عملی میں "دوسرا موقع" (Second Chance) تجارتی فیچر بھی شامل ہے، جو ابتدائی تجارت ناکام ہونے کے بعد مخالف سمت میں بریک آؤٹ کے مواقعوں کو پکڑنے کی اجازت دیتا ہے، اور تاجروں کو مارکیٹ کی حرکیات کو بہتر طور پر سمجھنے میں مدد کے لیے جامع تصوراتی خصوصیات فراہم کرتا ہے۔

حکمت عملی کا اصول

اوپننگ رینج بریک آؤٹ ATR ٹریلنگ اسٹاپ لاس حکمت عملی کی بنیادی منطق مارکیٹ کے افتتاح کے بعد قیمت کی ابتدائی حد کی اہمیت پر مبنی ہے۔ یہ حکمت عملی پہلے مخصوص وقت کی ونڈو (09:30-09:35 EST) میں قیمت کی بلند ترین اور پست ترین سطحوں کو ریکارڈ کرتی ہے، جسے "اوپننگ رینج" کہا جاتا ہے۔ اس کے بعد، نظام قیمت کے اس حد سے بریک آؤٹ ہونے کی نگرانی کرتا ہے، اور درج ذیل کلیدی میکانزم کے ذریعے تجارتی معیار کو یقینی بناتا ہے:

-

اوپننگ رینج کی شناخت اور بریک آؤٹ کی تصدیق: نظام مقررہ وقت کی ونڈو میں قیمت کی بلند ترین اور پست ترین سطحوں کو ریکارڈ کرتا ہے، پھر بریک آؤٹ کی نگرانی کرتا ہے۔ بریک آؤٹ کو دوہرے فلٹرنگ میکانزم کے ذریعے تصدیق کرنی ہوگی:

- کینڈل اسٹک کی وِک (wick) فیصد فلٹرنگ: اس بات کو یقینی بناتا ہے کہ بریک آؤٹ کرنے والی کینڈل کی اوپر/نیچے کی وِک کینڈل باڈی کے مخصوص فیصد سے زیادہ نہ ہو، جھوٹے بریک آؤٹ سے بچنے کے لیے۔

- بریک آؤٹ فاصلہ فلٹرنگ: اس بات کو یقینی بناتا ہے کہ قیمت کا بریک آؤٹ معقول حد تک ہو، نہ بہت چھوٹا (معمولی بریک آؤٹ سے بچنے کے لیے) اور نہ بہت بڑا (ضرورت سے زیادہ پھیلاؤ سے بچنے کے لیے)۔

-

انٹری میکانزم: حکمت عملی دو انٹری طریقوں کو سپورٹ کرتی ہے:

- فوری انٹری: تصدیق شدہ بریک آؤٹ والی اسی کینڈل کے کلوزنگ پرائس پر براہ راست داخل ہونا۔

- ریٹریسمنٹ انٹری: بریک آؤٹ کرنے والی کینڈل کے باڈی کے مخصوص فیصد پوزیشن تک قیمت کے واپس آنے کا انتظار کرنا، عام طور پر 50% ریٹریسمنٹ پوزیشن پر سیٹ کیا جاسکتا ہے۔

-

اسٹاپ لاس سیٹنگ: نظام دو قسم کے اسٹاپ لاس فراہم کرتا ہے:

- بریک آؤٹ کینڈل اسٹاپ لاس: اسٹاپ لاس کو بریک آؤٹ کرنے والی کینڈل کے انتہائی نقطے سے باہر رکھنا۔

- مخالف رینج اسٹاپ لاس: اسٹاپ لاس کو اوپننگ رینج کے مخالف کنارے سے باہر رکھنا، قیمت کو زیادہ اتار چڑھاؤ کی گنجائش فراہم کرتا ہے۔

-

رسک مینجمنٹ: نظام رسک سے ریوارڈ ریشیو ملٹیپلائر (Risk:Reward Multiplier) کا استعمال کرتے ہوئے خود بخود ٹیک پرافٹ کی پوزیشن کا حساب لگاتا ہے، متحرک رسک مینجمنٹ کو نافذ کرتا ہے۔ مثال کے طور پر، 2:1 کا رسک سے ریوارڈ ریشیو ترتیب دینے کا مطلب ہے کہ ممکنہ منافع ممکنہ نقصان سے دوگنا ہے۔

-

ATR ٹریلنگ اسٹاپ لاس: ایک بار جب منافع پہلے سے طے شدہ رسک سے ریوارڈ ریشیو تک پہنچ جاتا ہے، تو نظام ATR پر مبنی ٹریلنگ اسٹاپ لاس کو فعال کرسکتا ہے، جس سے کچھ منافع کو لاک کیا جاسکتا ہے جبکہ رجحان کو جاری رہنے دیا جاسکتا ہے۔

-

دوسرا موقع تجارت: جب ابتدائی تجارت اسٹاپ لاس کو ٹرگر کرتی ہے یا ناکام ہوتی ہے، تو نظام خود بخود اوپننگ رینج کی مخالف سمت میں بریک آؤٹ کے مواقع تلاش کرسکتا ہے، جس سے اسی دن دو طرفہ تجارت ممکن ہوتی ہے۔

حکمت عملی کے فوائد

-

اعلیٰ معیار کے تجارتی مواقع پر توجہ: متعدد تصدیقی میکانزم (وِک فلٹرنگ، فاصلہ فلٹرنگ) کے ذریعے، حکمت عملی جھوٹے بریک آؤٹ تجارت کو نمایاں طور پر کم کرتی ہے اور جیتنے کی شرح کو بہتر بناتی ہے۔

-

لچکدار انٹری میکانزم: فوری یا ریٹریسمنٹ انٹری کو سپورٹ کرتی ہے، مختلف تجارتی انداز اور مارکیٹ کے حالات کے مطابق ڈھلتی ہے۔ فوری انٹری مضبوط رجحان کے لیے موزوں ہے، جبکہ ریٹریسمنٹ انٹری بہتر انٹری قیمت فراہم کرسکتی ہے۔

-

خود کو ڈھالنے والا رسک مینجمنٹ: رسک سے ریوارڈ ریشیو ملٹیپلائر پر مبنی متحرک ٹیک پرافٹ سیٹنگ اس بات کو یقینی بناتی ہے کہ ہر تجارت میں یکساں رسک کی خصوصیات ہوں، معیاری سرمایہ کا انتظام ممکن بناتا ہے۔

-

منافع کی زیادہ سے زیادہ حد: ATR ٹریلنگ اسٹاپ لاس کی خصوصیت حاصل شدہ منافع کی حفاظت کرتے ہوئے مضبوط رجحان کو جاری رہنے دیتی ہے، قبل از وقت اخراج سے بچاتی ہے۔

-

اعلیٰ درجے کی تصوریت: نظام جامع بصری معاونت فراہم کرتا ہے، جس میں رینج مارکرز، بریک آؤٹ تصدیقی لیبلز، تجارتی حیثیت کے اشارے، انٹری/اسٹاپ لاس/ٹیک پرافٹ مارکرز وغیرہ شامل ہیں، جو تجارتی فیصلوں کو زیادہ بدیہی بناتے ہیں۔

-

غیر جانبدارانہ پیچھے نظر آنے والا ڈیزائن: حکمت عملی مکمل طور پر

barstate.isconfirmedکا استعمال کرتی ہے تاکہ اس بات کو یقینی بنایا جاسکے کہ تمام فیصلے تصدیق شدہ قیمت کے اعداد و شمار پر مبنی ہوں، آگے کی تعصب (look-ahead bias) سے بچتے ہوئے، جو حقیقی تجارتی ماحول کے مطابق ہے۔ -

دوسرے موقع کا میکانزم: دوسرے موقع کی تجارت کو فعال کرکے، حکمت عملی ابتدائی سمت کی غلطی کی صورت میں مارکیٹ کی تبدیلیوں کے مطابق تیزی سے ڈھل سکتی ہے، مخالف مواقعوں کو پکڑ سکتی ہے اور سرمائے کے استعمال کی کارکردگی کو بڑھا سکتی ہے۔

-

سیشن مینجمنٹ کی بہتری: سیشن کے اختتام پر خود بخود پوزیشن بند کرنے کی خصوصیت اس بات کو یقینی بناتی ہے کہ رات بھر پوزیشن نہ رکھی جائے، رات کے خطرے کو کم کرتا ہے۔

حکمت عملی کے خطرات

-

رینج کی تشکیل کے دوران اتار چڑھاؤ کا خطرہ: اوپننگ رینج کی تشکیل کے دوران (09:30-09:35)، مارکیٹ میں غیر معمولی اتار چڑھاؤ ہوسکتا ہے، جس کی وجہ سے رینج بہت وسیع یا بہت تنگ ہوسکتی ہے۔ بہت وسیع رینج بڑے اسٹاپ لاس کا سبب بن سکتی ہے، جبکہ بہت تنگ رینج بار بار جھوٹے بریک آؤٹ کو متحرک کرسکتی ہے۔

حل: اوپننگ رینج کے سائز کے لیے فلٹرنگ کی شرائط شامل کرنے پر غور کیا جاسکتا ہے، غیر معمولی رینج کو خارج کرنے کے لیے؛ یا تجارتی تاریخ کے فلٹر کو ایڈجسٹ کرکے مخصوص دنوں (جیسے اہم اقتصادی ڈیٹا کے اعلان کے دن) میں زیادہ اتار چڑھاؤ سے بچا جاسکتا ہے۔ -

بریک آؤٹ کے بعد شدید واپسی کا خطرہ: مؤثر بریک آؤٹ کے بعد مارکیٹ میں شدید واپسی ہوسکتی ہے، جس کی وجہ سے اسٹاپ لاس متحرک ہونے کے بعد مارکیٹ اصل سمت میں جاری رہ سکتی ہے۔

حل: زیادہ ڈھیلی اسٹاپ لاس سیٹنگ استعمال کرنے پر غور کریں، جیسے مخالف رینج اسٹاپ لاس؛ یا انٹری میکانزم کو ریٹریسمنٹ انٹری میں تبدیل کریں تاکہ بہتر انٹری قیمت اور کم رسک ایکسپوژر حاصل ہو۔ -

سگنل کا معیار فلٹر سیٹنگ پر منحصر: بریک آؤٹ کی تصدیق کے لیے وِک فلٹرنگ اور فاصلہ فلٹرنگ کے پیرامیٹرز سگنل کے معیار کو نمایاں طور پر متاثر کرتے ہیں، نامناسب پیرامیٹرز اچھے تجارتی مواقع کو فلٹر کرسکتے ہیں یا زیادہ کم معیار کے سگنل قبول کرسکتے ہیں۔

حل: تاریخی بیک ٹیسٹنگ کے ذریعے فلٹر پیرامیٹرز کو بہتر بنائیں، مخصوص مارکیٹ اور آلے کے لیے بہترین سیٹنگ تلاش کریں؛ خود کو ڈھالنے والے پیرامیٹرز استعمال کرنے پر غور کریں، جو مارکیٹ کے اتار چڑھاؤ کے مطابق فلٹر کے معیار کو متحرک طور پر ایڈجسٹ کریں۔ -

ٹریلنگ اسٹاپ لاس پیرامیٹرز کی حساسیت: ATR ٹریلنگ اسٹاپ لاس کے پیرامیٹرز بہت تنگ سیٹ کرنے سے چھوٹی واپسی میں قبل از وقت اخراج ہوسکتا ہے، جبکہ بہت ڈھیلے سیٹ کرنے سے زیادہ منافع واپس جانے کا امکان ہوتا ہے۔

حل: ہدف کے آلے کے تاریخی اتار چڑھاؤ کی خصوصیات کی بنیاد پر ATR کی مدت اور ملٹیپلائر کو ایڈجسٹ کریں؛ جزوی پوزیشن بند کرنے کی حکمت عملی پر عمل کریں، کچھ حصے کے لیے فکسڈ ٹیک پرافٹ اور کچھ کے لیے ٹریلنگ اسٹاپ لاس استعمال کریں۔ -

تجارتی تعدد کی حد: حکمت عملی روزانہ زیادہ سے زیادہ دو بار تجارت کرتی ہے (ابتدائی تجارت اور دوسرا موقع)، جو دن کے اندر تمام مواقعوں کا مکمل فائدہ نہیں اٹھا سکتی۔

حل: حکمت عملی کو بڑھانے پر غور کریں، دن کے دیگر اوقات میں اہم قیمت کی حدود کی نگرانی کریں؛ یا دیگر تکنیکی اشاروں کے ساتھ ملا کر ایک جامع حکمت عملی تشکیل دیں، تجارتی سگنل کے ذرائع میں اضافہ کریں۔

حکمت عملی کی بہتری کی سمت

-

خود کو ڈھالنے والی اوپننگ رینج کی مدت: فی الحال حکمت عملی 5 منٹ کی فکسڈ اوپننگ رینج استعمال کرتی ہے، اسے مارکیٹ کے اتار چڑھاؤ کے مطابق متحرک طور پر ایڈجسٹ کرنے پر غور کیا جاسکتا ہے۔ کم اتار چڑھاؤ والی مارکیٹ میں رینج کا وقت 3 منٹ تک کم کیا جاسکتا ہے، جبکہ زیادہ اتار چڑھاؤ والی مارکیٹ میں 10 منٹ تک بڑھایا جاسکتا ہے، مختلف مارکیٹ حالات کے مطابق بہتر طور پر ڈھلنے کے لیے۔

-

حجم کے ساتھ تصدیق شامل کریں: بریک آؤٹ کی تصدیق کے میکانزم میں حجم کی فلٹرنگ شامل کریں، جس کے تحت بریک آؤٹ کے وقت حجم پچھلے چند ادوار کی اوسط حجم سے نمایاں طور پر زیادہ ہونا چاہیے، بریک آؤٹ کی تاثیر کو بڑھانے کے لیے۔ یہ بریک آؤٹ کینڈل کے حجم اور پچھلے N ادوار کے اوسط حجم کے تناسب کا حساب لگا کر حاصل کیا جاسکتا ہے۔

-

ملٹی ٹائم فریم تجزیہ: اعلیٰ ٹائم فریم کے رجحان کی سمت کا فلٹر متعارف کروائیں، صرف اس وقت داخل ہوں جب ڈیلی یا آورلی ٹائم فریم کا رجحان بریک آؤٹ کی سمت کے ساتھ موافق ہو، جیتنے کی شرح بڑھانے کے لیے۔ سادہ موونگ ایوریج کی ڈھلوان یا زیادہ جدید رجحان کے اشارے اعلیٰ ٹائم فریم کے رجحان کا تعین کرنے کے لیے استعمال کیے جاسکتے ہیں۔

-

سرمایہ کے انتظام کو بہتر بنائیں: متحرک پوزیشن سائز ایڈجسٹمنٹ میکانزم نافذ کریں، تاریخی اتار چڑھاؤ، موجودہ اکاؤنٹ سائز اور حالیہ کارکردگی کی بنیاد پر خود بخود معاہدوں کی تعداد کو ایڈجسٹ کریں، بہتر رسک کنٹرول حاصل کرنے کے لیے۔ مثال کے طور پر، مسلسل منافع کے بعد آہستہ آہستہ پوزیشن بڑھائیں، اور مسلسل نقصان کے بعد پوزیشن کم کریں۔

-

مشین لرننگ ماڈل کا انضمام: بریک آؤٹ کے معیار کا اندازہ لگانے کے لیے مشین لرننگ ماڈل متعارف کروائیں، تاریخی ڈیٹا پر ماڈل کو تربیت دے کر ان بریک آؤٹ پیٹرن کی شناخت کریں جن کے کامیاب ہونے کا سب سے زیادہ امکان ہو۔ خصوصیات میں اوپننگ رینج کا سائز، مارکیٹ کا اتار چڑھاؤ، پچھلے تجارتی دن کی قیمت کی حرکت، مخصوص وقت کے پیٹرن وغیرہ شامل ہوسکتے ہیں۔

-

دوسرے موقع کی تجارتی منطق کو بہتر بنائیں: دوسرے موقع کی تجارت کے ٹرگر کی شرائط کو بہتر بنائیں، نہ صرف ابتدائی تجارت کی ناکامی پر مبنی ہوں بلکہ مارکیٹ کے ڈھانچے میں تبدیلی اور ابھرتے ہوئے مومینٹم اشاروں پر بھی غور کریں، دوسری تجارت کی کامیابی کی شرح بڑھانے کے لیے۔

-

انفرادی آلے کے لیے پیرامیٹرز کو ذاتی بنائیں: مختلف تجارتی آلات کے لیے بہتر پیرامیٹرز کے سیٹ تیار کریں، ہر آلے کی منفرد اتار چڑھاؤ کی خصوصیات اور قیمت کے رویے کو مدنظر رکھتے ہوئے۔ مثال کے طور پر، زیادہ اتار چڑھاؤ والے آلات کو ڈھیلے فلٹر سیٹنگ اور زیادہ قدامت پسند رسک سے ریوارڈ ریشیو کی ضرورت ہوسکتی ہے۔

-

مارکیٹ جذبات کے اشارے شامل کریں: VIX انڈیکس یا دیگر مارکیٹ جذبات کے اشارے متعارف کروائیں، انتہائی مارکیٹ جذبات کے دوران حکمت عملی کے پیرامیٹرز کو ایڈجسٹ کریں یا عارضی طور پر تجارت کو غیر فعال کریں، اعلیٰ غیر یقینی صورتحال والے ماحول سے بچنے کے لیے۔

خلاصہ

اوپننگ رینج بریک آؤٹ ATR ٹریلنگ اسٹاپ لاس حکمت عملی ایک اچھی طرح سے تشکیل شدہ مقداری تجارتی نظام ہے، جو اوپننگ رینج بریک آؤٹ، ذہین فلٹرنگ میکانزم، لچکدار انٹری آپشنز اور جدید رسک مینجمنٹ کی خصوصیات کو خوبصورتی سے یکجا کرتا ہے۔ یہ حکمت عملی خاص طور پر امریکی اسٹاک اور فیوچر مارکیٹوں میں انٹرا ڈے ٹریڈنگ کے لیے موزوں ہے، افتتاح کے بعد سمتاتی بریک آؤٹس کو پکڑ کر منافع کماتی ہے۔

حکمت عملی کی بنیادی قدر اس کے کثیر پرت تصدیقی میکانزم اور رسک مینجمنٹ سسٹم میں مضمر ہے، جو وِک اور فاصلے کے فلٹرز کے ذریعے جھوٹے بریک آؤٹ تجارت کو نمایاں طور پر کم کرتی ہے، جبکہ رسک سے ریوارڈ ریشیو ملٹیپلائر اور ATR ٹریلنگ اسٹاپ لاس کا استعمال کرتے ہوئے یکساں رسک ایکسپوژر اور منافع کی حفاظت کو یقینی بناتی ہے۔ دوسرے موقع کی تجارت کی خصوصیت حکمت عملی میں موافقت اور اضافی منافع کے مواقع کا اضافہ کرتی ہے۔

اگرچہ اس حکمت عملی کے متعدد فوائد ہیں، لیکن صارفین کو پیرامیٹر کی اصلاح کی اہمیت پر توجہ دینی چاہیے، مختلف مارکیٹوں اور آلات کو بہترین نتائج حاصل کرنے کے لیے ہدفی ایڈجسٹمنٹ کی ضرورت ہوسکتی ہے۔ اسی کے ساتھ، تاجروں کو مشورہ دیا جاتا ہے کہ وہ اس حکمت عملی کو اپنے مکمل تجارتی نظام کے ایک حصے کے طور پر استعمال کریں، وسیع تر مارکیٹ تجزیہ اور رسک مینجمنٹ کے اصولوں کے ساتھ۔

تجویز کردہ بہتری کی سمتوں، خاص طور پر خود کو ڈھالنے والے پیرامیٹرز، ملٹی ٹائم فریم تجزیہ اور بہتر سرمایہ کے انتظام کے نظام کو نافذ کرکے، اس حکمت عملی میں اپنی استحکام اور منافع کی صلاحیت کو مزید بڑھانے کی صلاحیت ہے، اور یہ پیشہ ور تاجروں کے ٹول باکس میں ایک طاقتور آلہ بن سکتی ہے۔

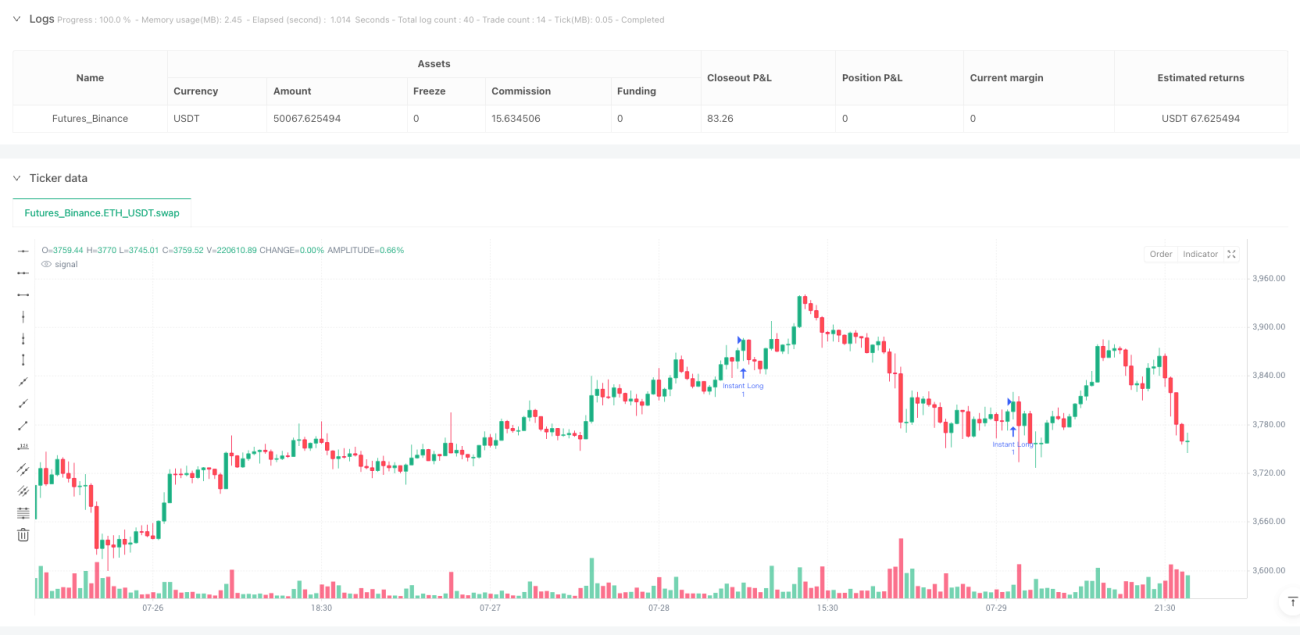

/*backtest

start: 2025-07-18 00:00:00

end: 2025-07-30 00:00:00

period: 30m

basePeriod: 30m

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Casper SMC 5min ORB - Roboquant AI", overlay=true, default_qty_type=strategy.fixed, default_qty_value=1, max_bars_back=500, calc_on_order_fills=true, calc_on_every_tick=false, initial_capital=50000, currency=currency.USD)

// === STRATEGY SETTINGS ===- 1