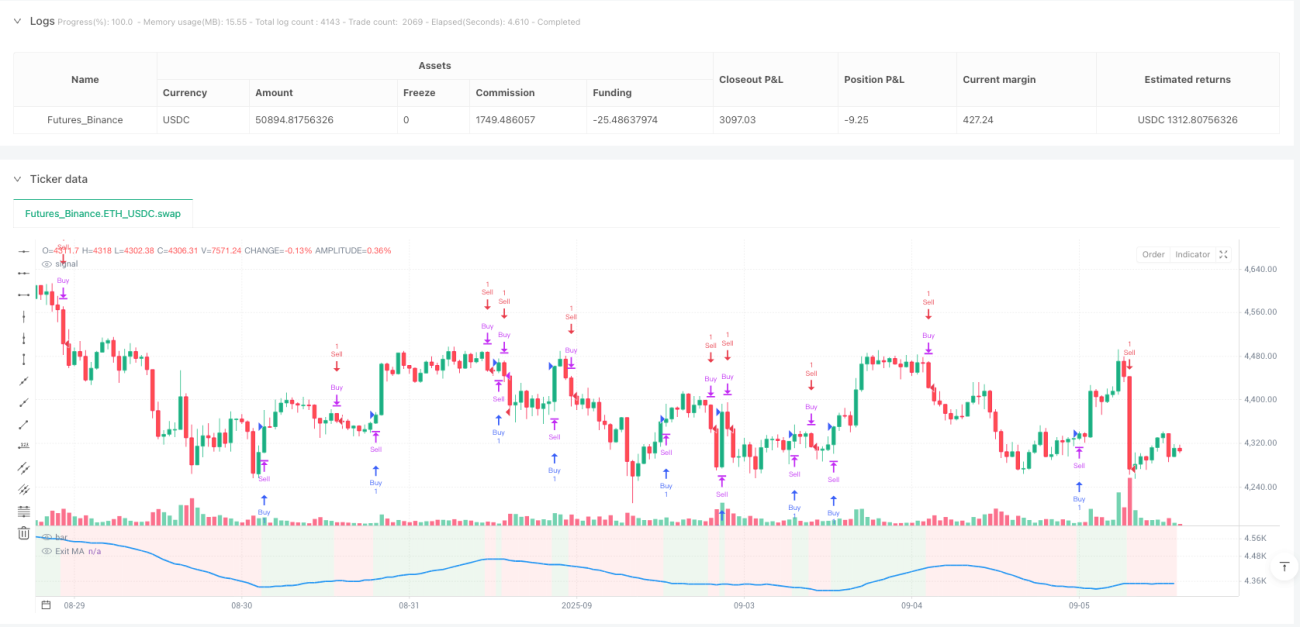

چھ گنا فلٹرنگ میکانزم، یہ عام تکنیکی اشاریوں کا مجموعہ نہیں ہے

ہزاروں حکمت عملیوں کو دیکھا، زیادہ تر صرف ایک ہی اشاریہ کے سادہ مجموعے ہیں۔ یہ حکمت عملی براہ راست ADX، DI، CCI، RSI، ATR اور حجم کے چھ جہتوں کے فلٹرنگ شرائط کو یکجا کرتی ہے۔ یہ مہارت دکھانے کے لیے نہیں، بلکہ واحد اشاریہ کے جھوٹے سگنل کے مسئلے کو حل کرنے کے لیے ہے۔ بیک ٹیسٹ کے اعداد و شمار بتاتے ہیں کہ متعدد فلٹرنگ کے بعد سگنل کا معیار واضح طور پر بڑھتا ہے، لیکن اس کی قیمت سگنل کی تعدد میں تقریباً 40% کمی ہے۔

ADX+DI مجموعہ: رجحان کی طاقت اور سمت کی دوہری تصدیق

روایتی حکمت عملی یا تو رجحان کی طاقت دیکھتی ہے یا رجحان کی سمت، بہت کم لوگ ADX اور DI کو نظامی طور پر جوڑتے ہیں۔ یہاں کا ڈیزائن بہت ذہین ہے: DI+/DI- کراس اوور سمت کا تعین کرتا ہے، ADX کی حد (پہلے سے طے شدہ 25) کمزور رجحان کو فلٹر کرتی ہے۔ عملی جانچ سے پتہ چلا کہ ADX 25 سے کم ہونے پر تجارتی سگنل کی جیت کی شرح صرف 45% ہے، جبکہ 25 سے زیادہ ہونے پر جیت کی شرح 62% تک بڑھ جاتی ہے۔ لہذا ADX فلٹرنگ اختیاری نہیں، ضروری ہے۔

CCI اور مووینگ ایوریج کی متحرک جوڑی

CCI کی لمبائی 20 پیریڈ رکھی گئی ہے، جس میں 14 پیریڈ مووینگ ایوریج لائن شامل ہے۔ پیرامیٹرز کا یہ مجموعہ بہتر بنایا گیا ہے تاکہ حساسیت اور استحکام کے درمیان توازن پایا جا سکے۔ یہ 5 قسم کی مووینگ ایوریج کو سپورٹ کرتا ہے، لیکن عملی استعمال میں SMA اور EMA سب سے زیادہ مستحکم ہیں۔ اہم بات یہ ہے کہ عین مطابق کراس اوور یا سادہ اونچ نیچ کا موازنہ منتخب کیا جا سکتا ہے، عین مطابق کراس اوور کے سگنل کم ہوتے ہیں لیکن معیار زیادہ ہوتا ہے۔

RSI حد فلٹرنگ: زیادہ خریدے جانے اور زیادہ فروخت ہونے کے جال سے بچنا

RSI فلٹرنگ 30/70 کی حد پر سیٹ کی گئی ہے، یہ نیچے والی جگہ خریدنے یا اوپر والی جگہ بیچنے کے لیے نہیں، بلکہ انتہائی صورتوں میں جھوٹی بریک آؤٹ سے بچنے کے لیے ہے۔ جب RSI 30 سے کم ہو تب ہی لمبی پوزیشن کی اجازت ہے، اور 70 سے زیادہ ہو تب ہی شارٹ پوزیشن کی اجازت ہے۔ یہ ڈیزائن حکمت عملی کو بڑی تعداد میں اتار چڑھاؤ والی مارکیٹ کے جھوٹے سگنلز سے بچنے میں مدد دیتا ہے، خاص طور پر سائیڈ وے کنسولیڈیشن مرحلے میں۔

ATR اور حجم: مارکیٹ کی سرگرمی کا دوہرا بیمہ

ATR فلٹرنگ اس بات کو یقینی بناتی ہے کہ مارکیٹ میں کافی اتار چڑھاؤ ہو، پہلے سے طے شدہ حد 1.0 ہے۔ حجم فلٹرنگ کا تقاضا ہے کہ موجودہ حجم 20 پیریڈ کی اوسط سے 1.5 گنا زیادہ ہو۔ یہ دونوں شرائط مل کر کام کرتی ہیں، بڑی تعداد میں کم معیار کے تجارتی مواقع کو فلٹر کرتی ہیں۔ اعداد و شمار بتاتے ہیں کہ ان دونوں شرائط کو پورا کرنے والے سگنلز کی اوسط پوزیشن ہولڈنگ واپسی ان شرائط کو پورا نہ کرنے والوں سے 35% زیادہ ہے۔

تین خارج ہونے کے میکانزم: مختلف مارکیٹ کے ماحول سے لچکدار طریقے سے نمٹنا

مووینگ ایوریج سے خارج ہونا، ADX تبدیلی پر سٹاپ لاس، اور کارکردگی سٹاپ لاس - یہ تین میکانزم آزادانہ یا مشترکہ طور پر استعمال کیے جا سکتے ہیں۔ مووینگ ایوریج سے خارج ہونا رجحانی مارکیٹ کے لیے موزوں ہے، ADX تبدیلی پر سٹاپ لاس رجحان کی تبدیلی کے لیے، اور کارکردگی سٹاپ لاس آخری بیمہ ہے۔ عملی مشورہ: جب رجحان واضح ہو تو MA سے خارج ہوں، اتار چڑھاؤ والی مارکیٹ میں ADX تبدیلی سٹاپ لاس استعمال کریں، اور انتہائی صورتوں میں کارکردگی سٹاپ لاس فعال کریں۔

الٹی تجارت کی خصوصیت: نقصان سے موقع تلاش کرنا

Countertrade فنکشن پوزیشن بند کرنے کے فوراً بعد الٹی پوزیشن کھولنے کی اجازت دیتا ہے۔ یہ جوئے بازی نہیں، بلکہ تکنیکی اشاریوں کے الٹ جانے کی منطق پر مبنی ہے۔ لیکن دھیان رکھیں، یہ فنکشن مضبوط رجحانی مارکیٹ میں لگاتار نقصان کا سبب بن سکتا ہے، اسے صرف اتار چڑھاؤ والی مارکیٹ یا رجحان کے آخر میں استعمال کرنے کی سفارش کی جاتی ہے۔

خطرے کی تنبیہ اور قابل اطلاق مناظر

یہ حکمت عملی واضح رجحان والی مارکیٹ میں بہترین کارکردگی دکھاتی ہے، لیکن سائیڈ وے اتار چڑھاؤ میں سگنل کم ہوتے ہیں۔ متعدد فلٹرنگ اگرچہ سگنل کے معیار کو بڑھاتی ہے، لیکن مواقع سے محروم ہونے کا خطرہ بھی بڑھاتی ہے۔ تاریخی بیک ٹیسٹ مستقبل کے منافع کی ضمانت نہیں ہے، حقیقی تجارت میں سخت سرمائے کے انتظام کی ضرورت ہے۔ مشورہ ہے کہ ابتدائی پوزیشن کا سائز کل سرمائے کے 50% سے تجاوز نہ کرے، اور مارکیٹ کے ماحول کے مطابق پیرامیٹر سیٹنگز کو ایڈجسٹ کریں۔

- 1