رجحان سیڑھی اوسط حکمت عملی: جب مارکیٹ افقی ہو تو خوبصورتی سے "لیٹنا" کیسے ممکن ہے؟

روایتی ٹرینڈ فالو کرنے والی حکمت عملیاں رینج مارکیٹ میں کیوں بار بار ناکام ہو جاتی ہیں؟

ایک کوانٹیٹیٹو ٹریڈر کے طور پر، مجھ سے اکثر یہ سوال پوچھا جاتا ہے: وہ حکمت عملیاں جو ٹرینڈ مارکیٹ میں بہترین کارکردگی دکھاتی ہیں، جیسے ہی مارکیٹ رینج میں آتی ہیں، بڑی کمی کا سامنا کیوں کرتی ہیں؟

جواب بہت آسان ہے: زیادہ تر ٹرینڈ فالو کرنے والی حکمت عملیوں میں "ٹرینڈ کا جنون" ہوتا ہے – وہ ہر مارکیٹ ماحول میں بار بار ٹریڈ کرنے کی کوشش کرتی ہیں، جبکہ ایک بنیادی حقیقت کو نظر انداز کرتی ہیں: مارکیٹ کا 70% وقت سائیڈ ویز یا رینج میں ہوتا ہے۔

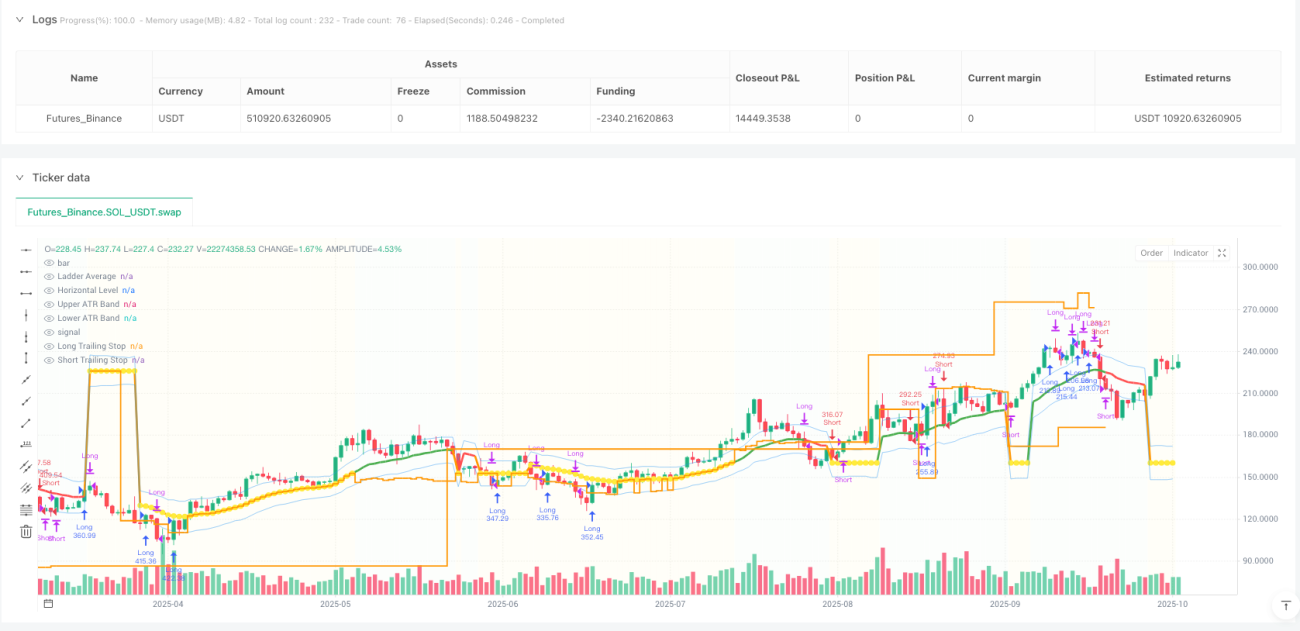

آج جس "ٹرینڈ اسٹیپ اوسط" حکمت عملی کا تجزیہ کیا جا رہا ہے، وہ خاص طور پر اس مسئلے کا ایک دلچسپ حل پیش کرتی ہے: ٹرینڈ مارکیٹ میں فعال طور پر فالو کریں، رینج مارکیٹ میں "خوبصورتی سے آرام کریں"۔

"اسٹیپ اوسط" کیا ہے؟ یہ تصور ٹرینڈ فالونگ کو کیسے نئے سرے سے متعین کرتا ہے؟

روایتی موونگ ایوریج حکمت عملیوں میں ایک مہلک خامی ہے: وہ ہمیشہ تبدیل ہوتی رہتی ہیں۔ چاہے مارکیٹ مضبوط ٹرینڈ میں ہو یا سائیڈ ویز، اوسط قیمت کی لکیر قیمت کے اتار چڑھاؤ کے ساتھ مسلسل ایڈجسٹ ہوتی رہتی ہے، جس کی وجہ سے بہت سے جھوٹے سگنل پیدا ہوتے ہیں۔

"اسٹیپ اوسط" کا بنیادی خیال یہ ہے: مخصوص حالات میں موونگ ایوریج کو "منجمد" کرنا۔

عملی نفاذ کا طریقہ کار درج ذیل ہے:

-

ٹرینڈ کی حالت کا پتہ لگانا: ADX انڈیکیٹر کے ذریعے مارکیٹ کی ٹرینڈ کی طاقت کا اندازہ لگانا

- ADX > 25: مضبوط ٹرینڈ مارکیٹ

- اوسط کی ڈھلان < 0.3%: سائیڈ ویز مارکیٹ

-

متحرک اوسط سوئچنگ:

- مضبوط ٹرینڈ: عام طور پر EMA(21) کو فالو کریں

- سائیڈ ویز: اوسط کو افقی پوزیشن پر "منجمد" کر دیا جاتا ہے، جو سپورٹ/ریزسٹنس بناتا ہے

اس ڈیزائن کی خوبصورتی یہ ہے: یہ حکمت عملی کو مختلف مارکیٹ ماحول میں مختلف "شخصیت" دکھانے دیتا ہے – ٹرینڈ میں حساس، رینج میں مستحکم۔

"ٹرینڈ کیپچر" سسٹم کیسے لاگو کیا جائے؟

بنیادی اسٹیپ اوسط میکانزم کے علاوہ، اس حکمت عملی میں ایک "ٹرینڈ کیپچر" ماڈیول بھی شامل ہے، جو میرے خیال میں سب سے زیادہ اختراعی حصہ ہے:

فوری ریورسل میکانزم:

- جب ابھی بند پوزیشن کے برعکس مضبوط ٹرینڈ ظاہر ہو

- 3 ادوار کے اندر تیزی سے نئی پوزیشن کھولیں

- شرائط: ADX > 30 اور DI+ اور DI- کے درمیان فرق > 10

یہ ڈیزائن روایتی حکمت عملیوں کے ایک اہم مسئلے کو حل کرتا ہے: ٹرینڈ ریورسل کے ابتدائی مرحلے میں پوزیشن کو جلدی کیسے ایڈجسٹ کیا جائے۔

ایک منظر کا تصور کریں: آپ نے ابھی اسٹاپ لاس کی وجہ سے لانگ پوزیشن بند کی، اور مارکیٹ فوراً مضبوط نیچے کی طرف ٹرینڈ میں آ جاتی ہے۔ روایتی حکمت عملی کو نئے سگنل کی تصدیق کے لیے انتظار کرنا پڑتا، لیکن یہ "ٹرینڈ کیپچر" سسٹم 3 ادوار کے اندر تیزی سے شارٹ پوزیشن کھول سکتا ہے۔

رسک مینجمنٹ: مارکیٹ کی حالتوں کے مطابق فرق کیوں کیا جائے؟

اس حکمت عملی کا سب سے قابلِ تعلیم پہلو اس کا تفریقی رسک مینجمنٹ میکانزم ہے:

رینج مارکیٹ میں رسک کنٹرول:

- اسٹاپ لاس کو اسٹیپ اوسط کے قریب ایڈجسٹ کریں

- ATR کے ضرب کو کم کر کے اسٹاپ کو تنگ کریں

- ہدف کی سطحوں کو زیادہ قدامت پسند بنائیں

ٹرینڈ مارکیٹ میں رسک کنٹرول:

- معیاری ATR ضرب کے ساتھ اسٹاپ لاس استعمال کریں

- اسٹیپ وار موونگ اسٹاپ کو فعال کریں

- قیمت کے زیادہ اتار چڑھاؤ کی گنجائش دیں

یہ ڈیزائن ایک اہم تجارتی فلسفے کی عکاسی کرتا ہے: مختلف مارکیٹ ماحول میں مختلف رسک رویہ اختیار کرنا چاہیے۔ رینج مارکیٹ میں ہمیں زیادہ محتاط رہنا چاہیے؛ ٹرینڈ مارکیٹ میں ہمیں منافع کو بڑھنے کے لیے زیادہ جگہ دینی چاہیے۔

اسٹیپ وار موونگ اسٹاپ: منافع کی حفاظت اور ٹرینڈ فالونگ میں توازن کیسے قائم کیا جائے؟

روایتی موونگ اسٹاپ اکثر بہت مشینی ہوتا ہے، یا تو بہت تنگ ہونے کی وجہ سے جلد باہر نکلنا پڑتا ہے، یا بہت ڈھیلا ہونے کی وجہ سے منافع کی مؤثر حفاظت نہیں ہو پاتی۔ اس حکمت عملی کا اسٹیپ وار موونگ اسٹاپ ایک زیادہ ذہین حل پیش کرتا ہے:

اسٹیپ سیٹنگ کا طریقہ کار:

- ATR کی بنیاد پر متحرک طور پر اسٹیپ کے درمیان فاصلہ شمار کریں

- زیادہ سے زیادہ 5 اسٹیپ لیولز

- ہر اسٹیپ کو توڑنے پر اسٹاپ لاس کو اسی حساب سے اوپر لے جائیں

اس ڈیزائن کا فائدہ یہ ہے: یہ منافع کی حفاظت کرتے ہوئے ٹرینڈ کو ترقی کے لیے کافی جگہ دیتا ہے۔

عملی استعمال میں کیا خیال رکھنا چاہیے؟

میرے حقیقی تجربے کی بنیاد پر، اس قسم کی حکمت عملی استعمال کرتے وقت درج ذیل نکات پر توجہ دینی چاہیے:

-

پیرامیٹر آپٹیمائزیشن کا جال: ADX کی حد کو زیادہ آپٹیمائز نہ کریں، 25-30 کے درمیان کی قدریں زیادہ تر مارکیٹوں میں مستحکم رہتی ہیں

-

مارکیٹ کی موزونیت: یہ حکمت عملی اعتدال پسند اتار چڑھاؤ والی مارکیٹ کے لیے بہتر ہے، انتہائی اتار چڑھاؤ والے ماحول میں ATR ضرب کو ایڈجسٹ کرنے کی ضرورت پڑ سکتی ہے

-

سرمایہ انتظام: مشورہ ہے کہ ایک ٹریڈ میں کل سرمائے کا 10% سے زیادہ نہ لگائیں، خاص طور پر جب ٹرینڈ کیپچر فنکشن فعال ہو

-

بیک ٹیسٹ کے نقصانات: خاص طور پر سلپیج اور کمیشن کے اثرات پر توجہ دیں، خاص طور پر رینج مارکیٹ میں بار بار ٹریڈ کرنے کی صورت میں

اس حکمت عملی کی اختراعی قدر کیا ہے؟

کوانٹیٹیٹو حکمت عملیوں کی ترقی کے زاویے سے، یہ حکمت عملی ایک اہم ارتقائی سمت کی نمائندگی کرتی ہے: ایک ہی منطق سے کثیر حالتی خود انطباق کی طرف تبدیلی۔

روایتی حکمت عملیاں اکثر ایک مقررہ منطق کے ساتھ تمام مارکیٹ حالات کا مقابلہ کرنے کی کوشش کرتی ہیں، جبکہ یہ حکمت عملی "مقامی حالات کے مطابق" حکمت کو ظاہر کرتی ہے:

- ٹرینڈ مارکیٹ میں یہ ایک جارحانہ ٹرینڈ فالو کرنے والے کی طرح برتاؤ کرتی ہے

- رینج مارکیٹ میں یہ ایک قدامت پسند رینج ٹریڈر کی طرح برتاؤ کرتی ہے

یہ ڈیزائن سوچ حکمت عملی تیار کرنے والوں کے لیے اہم سبق رکھتی ہے: ہمیں اپنی حکمت عملیوں کو "مارکیٹ کا احساس" دینا چاہیے، نہ کہ اندھا دھند مقررہ منطق پر عمل کرنا۔

آخر میں، یہ یاد رکھنا ضروری ہے کہ کوئی بھی حکمت عملی کامل نہیں ہوتی۔ یہ اسٹیپ اوسط حکمت عملی نظریاتی طور پر خوبصورت ہے، لیکن عملی استعمال میں اسے مخصوص مارکیٹ ماحول اور ذاتی رسک رویے کے مطابق ایڈجسٹ کرنے کی ضرورت ہے۔ یاد رکھیں، بہترین حکمت عملی وہی ہے جو آپ کے لیے سب سے زیادہ موزوں ہو۔

/*backtest

start: 2024-10-09 00:00:00

end: 2025-10-07 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"SOL_USDT","balance":500000}]

*/

//@version=5

strategy("Trend Following Ladder Average Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// ═══════════════════════════════════════════════════════════════════════════════- 1