Chiến lược giao dịch dao động ba mô hình

Tổng quan

Chiến lược giao dịch dao động ba mô hình là một chiến lược giao dịch ngắn hạn dựa trên sự kết hợp của nhiều chỉ báo kỹ thuật. Chiến lược này kết hợp chỉ báo Siêu xu hướng (SuperTrend), Đường trung bình động hỗn hợp SSL (SSL Hybrid MA) và chỉ báo QQE cải tiến để tạo ra tín hiệu giao dịch ổn định. Nó phù hợp với các sản phẩm giao dịch có biến động cao như tiền điện tử và cổ phiếu, đặc biệt là trong giai đoạn sau khi bứt phá (breakout).

Nguyên lý

Tín hiệu vào lệnh

Vào lệnh mua (Long):

- Siêu xu hướng chuyển từ xu hướng giảm sang xu hướng tăng

- Giá đóng cửa cắt lên trên biên trên của đường trung bình động hỗn hợp SSL

- QQE cải tiến hiển thị màu xanh lam (xu hướng tăng)

Vào lệnh bán (Short):

- Siêu xu hướng chuyển từ xu hướng tăng sang xu hướng giảm

- Giá đóng cửa cắt xuống dưới biên dưới của đường trung bình động hỗn hợp SSL

- QQE cải tiến hiển thị màu đỏ (xu hướng giảm)

Tín hiệu thoát lệnh

Thoát lệnh mua: Siêu xu hướng chuyển từ xu hướng tăng sang xu hướng giảm

Thoát lệnh bán: Siêu xu hướng chuyển từ xu hướng giảm sang xu hướng tăng

Cắt lỗ (Stop Loss)

Có thể chọn cắt lỗ theo tỷ lệ phần trăm, theo ATR (Dải biến động trung bình) hoặc theo mức giá cao nhất/thấp nhất gần đây.

Chốt lời (Take Profit)

Có thể thiết lập tỷ lệ lợi nhuận chốt lời, tự động tính toán giá chốt lời.

Quản lý vốn

Tùy chọn sử dụng logic quản lý vốn để kiểm soát kích thước vị thế.

Vẽ biểu đồ

- Vẽ đường Siêu xu hướng, kênh đường trung bình động hỗn hợp SSL

- Tùy chọn có vẽ đường EMA (Đường trung bình động hàm mũ) hay không

- Vẽ các đường vào lệnh mua/bán, cắt lỗ, chốt lời

- Vẽ nhãn vào lệnh mua/bán

Ưu điểm

-

Kết hợp nhiều chỉ báo, tạo tín hiệu giao dịch ổn định

Kết hợp các chỉ báo Siêu xu hướng, Đường trung bình động hỗn hợp SSL và QQE cải tiến, các chỉ báo khác nhau xác nhận lẫn nhau, có thể lọc các phá vỡ giả (false breakout), tạo ra tín hiệu giao dịch chất lượng cao.

-

Phù hợp với giao dịch dao động trên các sản phẩm có biến động cao

Chiến lược áp dụng phương pháp giao dịch ngắn hạn, tập trung vào việc nắm bắt biến động giá ngắn và trung hạn. Siêu xu hướng có thể theo dõi xu hướng giá hiệu quả, trong khi Đường trung bình động hỗn hợp SSL có thể xác định rõ ràng các mức hỗ trợ và kháng cự. Sự kết hợp của cả hai có thể thu được lợi nhuận trong điều kiện thị trường dao động.

-

Nhiều tùy chọn cắt lỗ và chốt lời

Cắt lỗ có thể chọn tỷ lệ phần trăm, giá trị ATR hoặc giá trị cực đoan gần đây. Chốt lời có thể thiết lập tỷ lệ lợi nhuận. Quản lý vốn có thể kiểm soát vị thế. Người dùng có thể tự do kết hợp dựa trên đặc điểm sản phẩm và mức độ chấp nhận rủi ro.

-

Biểu đồ rõ ràng

Biểu đồ chiến lược rõ ràng, hiển thị trực quan các mức cắt lỗ và chốt lời. Các đường vào lệnh được đánh dấu dễ nhận biết tín hiệu giao dịch.

Rủi ro và Tối ưu hóa

-

Có thể xảy ra các khoản lỗ nhỏ

Do sử dụng giao dịch ngắn hạn, không thể tránh hoàn toàn các khoản lỗ nhỏ do dao động thông thường. Có thể nới lỏng biên độ cắt lỗ một cách phù hợp và tối ưu hóa logic quản lý vốn.

-

Rủi ro phá vỡ giả

Khi giá có những phá vỡ giả, có thể tạo ra tín hiệu sai. Có thể thử nghiệm các chu kỳ EMA khác nhau để lọc các phá vỡ giả, hoặc tối ưu hóa các tham số của chỉ báo nhận diện xu hướng.

-

Rủi ro chỉ báo cơ sở mất hiệu lực

Nếu các chỉ báo cơ sở mất hiệu lực, sẽ xuất hiện nhiều tín hiệu sai. Cần thường xuyên kiểm tra tính hiệu quả của chỉ báo và điều chỉnh kịp thời khi phát hiện vấn đề.

-

Tối ưu hóa chu kỳ backtest

Chu kỳ backtest hiện tại là khoảng thời gian cố định, không tương ứng với các chu kỳ thị trường khác nhau của sản phẩm. Khuyến nghị tối ưu hóa để phù hợp với khung thời gian giao dịch chính của hợp đồng.

-

Tối ưu hóa khả năng thích ứng với sản phẩm

Có thể tinh chỉnh các tham số chiến lược dựa trên đặc điểm dữ liệu của từng sản phẩm, cải thiện tỷ lệ thắng cho các lệnh mua và bán. Khuyến nghị sử dụng phương pháp tối ưu hóa từng bước (step optimization) để so sánh ảnh hưởng của các tham số khác nhau lên chiến lược.

Tổng kết

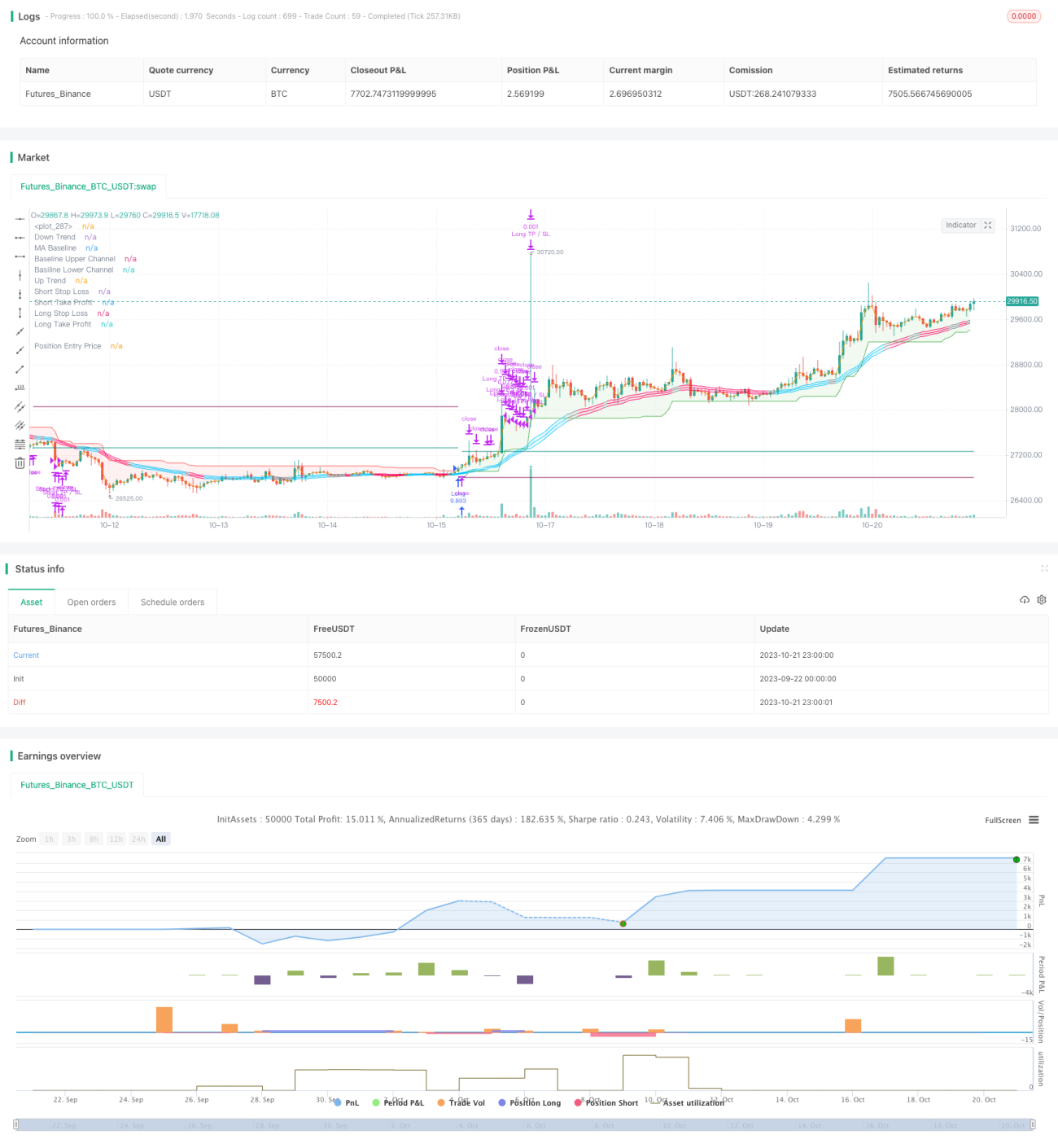

Chiến lược này kết hợp nhiều chỉ báo để tạo tín hiệu giao dịch, có thể lọc hiệu quả các phá vỡ giả, phù hợp với các loại tiền điện tử và cổ phiếu có biến động lớn. Đồng thời cung cấp nhiều tùy chọn cắt lỗ và chốt lời khác nhau, linh hoạt trong sử dụng. Nhìn chung, chiến lược tạo ra các tín hiệu giao dịch ổn định và có thể đạt được lợi nhuận tốt trong các điều kiện thị trường dao động ngắn và trung hạn. Bằng cách tối ưu hóa thêm, có thể điều chỉnh tham số cho từng sản phẩm giao dịch khác nhau, cải thiện hệ số lợi nhuận (profit factor) của chiến lược. Đây là một hệ thống giao dịch hiệu quả đáng để nghiên cứu sâu.

/*backtest

start: 2023-09-22 00:00:00

end: 2023-10-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5- 1