Chiến lược dừng lỗ theo dõi đột phá V2

Tổng quan

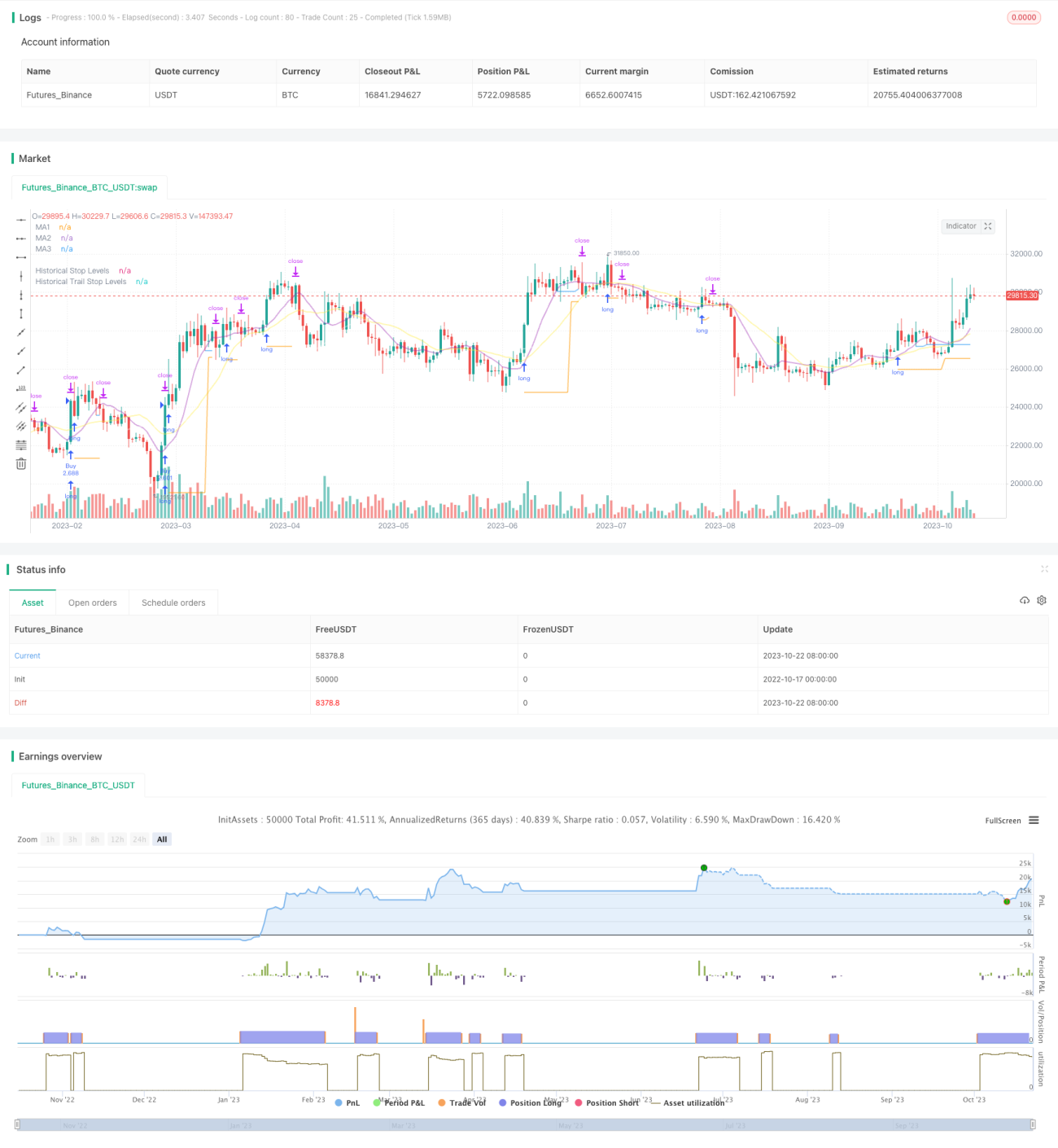

Chiến lược này kết hợp ưu điểm của chiến lược đột phá và chiến lược dừng lỗ theo xu hướng, nhằm nắm bắt tín hiệu đột phá vùng hỗ trợ kháng cự trong biểu đồ dài hạn, đồng thời sử dụng đường trung bình động để theo dõi dừng lỗ, giúp thu lợi nhuận theo hướng xu hướng dài hạn và kiểm soát rủi ro.

Nguyên lý chiến lược

-

Đầu tiên, chiến lược tính toán nhiều nhóm đường trung bình động với các tham số khác nhau, lần lượt sử dụng để xác định xu hướng, hỗ trợ kháng cự và theo dõi dừng lỗ.

-

Sau đó, xác định điểm cao nhất và điểm thấp nhất trong chu kỳ nhất định làm vùng hỗ trợ kháng cự để vào lệnh. Khi giá phá vỡ các vùng hỗ trợ kháng cự này, tín hiệu được tạo ra.

-

Chiến lược sử dụng phá vỡ điểm cao nhất làm tín hiệu mua (long), phá vỡ điểm thấp nhất làm tín hiệu bán (short).

-

Sau khi vào lệnh, vị thế sẽ được giữ với mức dừng lỗ được đặt tại điểm thấp nhất đã phá vỡ.

-

Khi vị thế đạt trạng thái có lợi nhuận, mức dừng lỗ sẽ chuyển sang theo dõi đường trung bình động. Khi giá phá vỡ xuống dưới đường trung bình động, điểm dừng lỗ được đặt tại mức thấp nhất của cây nến đó.

-

Nhờ vậy có thể khóa lợi nhuận, đồng thời cho phép vị thế có đủ không gian để theo dõi xu hướng.

-

Chiến lược cũng kết hợp chỉ báo ATR (Average True Range) để đảm bảo chỉ mua khi có sự đột phá trong phạm vi phù hợp, tránh các đột phá quá mức.

Phân tích ưu điểm chiến lược

-

Kết hợp ưu điểm kép của chiến lược đột phá và chiến lược dừng lỗ theo xu hướng.

-

Có thể mua vào khi đột phá theo xu hướng dài hạn, tăng xác suất thu lợi nhuận.

-

Chiến lược dừng lỗ vừa bảo vệ vị thế, vừa cho phép vị thế có đủ không gian hoạt động.

-

Thêm bộ lọc biến động, tránh các đột phá bất lợi do kéo dài quá mức.

-

Giao dịch tự động, phù hợp với một phần thời gian sao chép lệnh.

-

Có thể tùy chỉnh các đường trung bình động với chu kỳ khác nhau để giao dịch.

-

Có thể linh hoạt điều chỉnh phương thức theo dõi dừng lỗ.

Phân tích rủi ro chiến lược

-

Chiến lược đột phá dễ gặp rủi ro đột phá giả. Có thể nới lỏng xác nhận đột phá một cách phù hợp.

-

Cần đủ biến động để tạo ra tín hiệu đột phá, dễ không hiệu quả trong thị trường dao động mạnh.

-

Một số đột phá có thể quá ngắn để nắm bắt. Có thể giảm khung thời gian để tìm kiếm thêm cơ hội.

-

Dừng lỗ theo dõi có thể bị dừng quá thường xuyên trong thị trường dao động ngang. Có thể nới rộng khoảng cách dừng lỗ.

-

Bộ lọc biến động có thể bỏ lỡ một số cơ hội. Có thể giảm tham số lọc.

Hướng tối ưu hóa chiến lược

-

Thử nghiệm các tổ hợp tham số đường trung bình động khác nhau để tìm ra tham số tối ưu.

-

Thử nghiệm các cơ chế xác nhận đột phá khác nhau, như kênh, mô hình nến,...

-

Thử nghiệm các phương thức theo dõi dừng lỗ khác nhau để tìm ra mức dừng lỗ tối ưu.

-

Tối ưu hóa chiến lược quản lý vốn, như điểm số vị thế,...

-

Thêm bộ lọc chỉ báo kỹ thuật thống kê để nâng cao độ chính xác của bộ lọc.

-

Thử nghiệm hiệu quả của chiến lược trên các sản phẩm khác nhau.

-

Thêm thuật toán học máy để nâng cao hiệu quả chiến lược.

Tổng kết

Chiến lược này tích hợp tư tưởng đột phá và tư tưởng dừng lỗ theo xu hướng, dựa trên nhận định dài hạn đúng đắn, có thể tối ưu hóa không gian lợi nhuận. Chìa khóa là tìm ra tổ hợp tham số tối ưu, kết hợp với chiến lược quản lý vốn tốt để nắm bắt cơ hội dài hạn đồng thời kiểm soát rủi ro. Chiến lược này có tiềm năng trở thành một chiến lược xu hướng dài hạn đáng tin cậy thông qua tối ưu hóa thêm.

/*backtest

start: 2022-10-17 00:00:00

end: 2023-10-23 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1