Chiến lược xu hướng ngắn hạn dựa trên quyết định chỉ báo đa chiều

Tổng quan

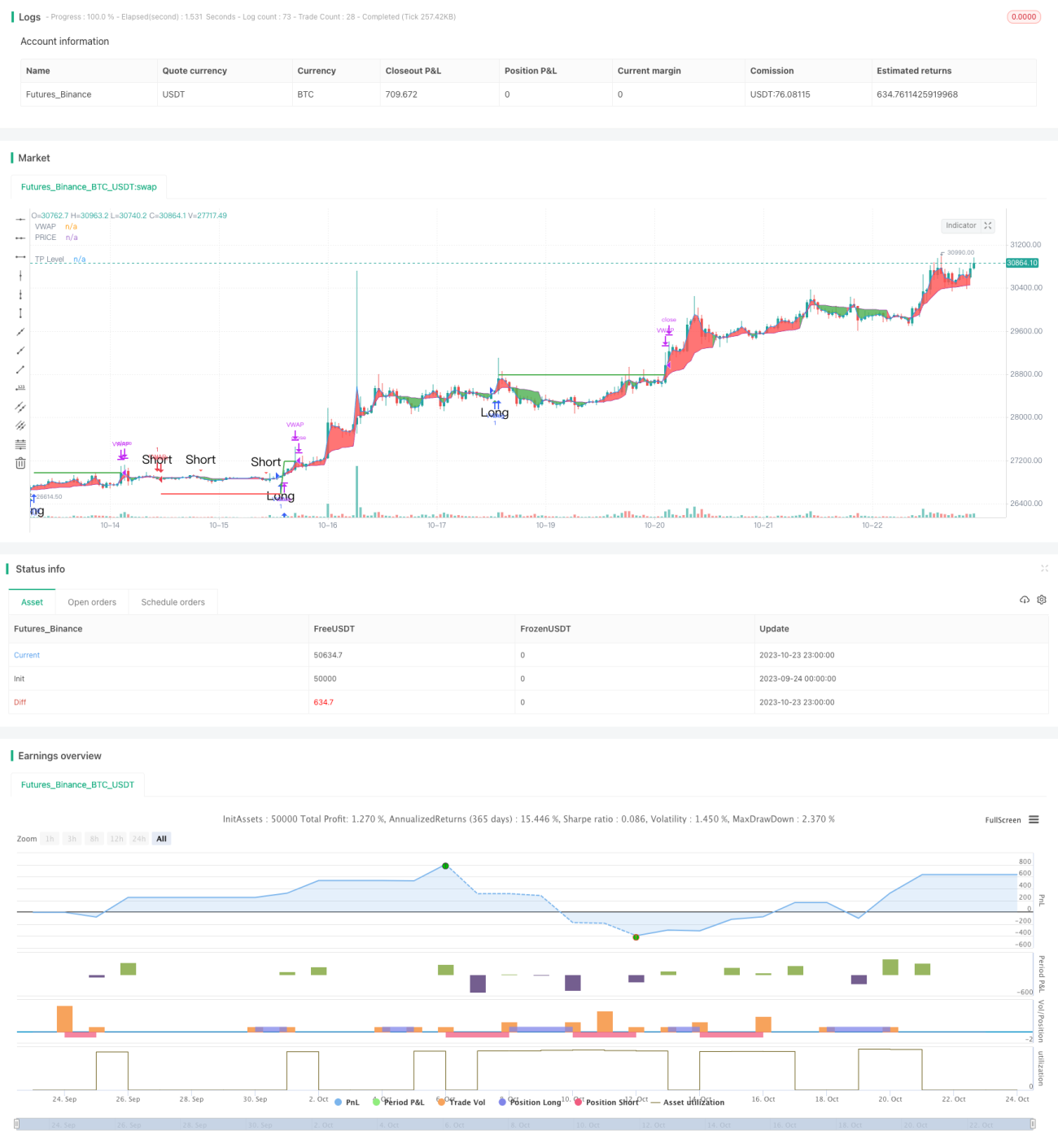

Chiến lược này kết hợp ba chỉ báo kỹ thuật từ các chiều không gian khác nhau, bao gồm ngưỡng hỗ trợ và kháng cự, hệ thống đường trung bình động và chỉ báo quá mua/quá bán, dựa trên tín hiệu tổng hợp của chúng để xác định hướng đi ngắn hạn, nhằm đạt được tỷ lệ thắng cao.

Nguyên lý chiến lược

Trong mã nguồn, trước tiên tính toán các ngưỡng hỗ trợ và kháng cự của giá, bao gồm trục dao động chuẩn và ngưỡng hỗ trợ/kháng cự Fibonacci, và vẽ chúng trên biểu đồ. Khi giá phá vỡ các ngưỡng quan trọng này, đó được coi là tín hiệu xu hướng quan trọng.

Tiếp theo là tính đường trung bình động có trọng số VWAP và giá trung bình, xác định tín hiệu giao cắt vàng và giao cắt tử thần của chúng. Đây thuộc về phán đoán xu hướng trung và dài hạn.

Cuối cùng là tính chỉ báo Stochastic RSI, xác định tín hiệu giao cắt vàng và giao cắt tử thần của nó, thuộc về chỉ báo quá mua/quá bán.

Tổng hợp các chỉ báo từ ba chiều không gian này, nếu ngưỡng hỗ trợ/kháng cự, đường trung bình VWAP và Stochastic RSI đồng thời phát ra tín hiệu mua, thì mở lệnh mua; nếu cả ba đồng thời phát ra tín hiệu bán, thì mở lệnh bán.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược này là kết hợp các chỉ báo từ ba chiều không gian khác nhau, giúp phán đoán toàn diện và chính xác hơn, tỷ lệ thắng cao. Trước tiên, ngưỡng hỗ trợ/kháng cự xác định xu hướng lớn; tiếp theo, VWAP xác định xu hướng trung và dài hạn; cuối cùng, Stochastic RSI xác định tình trạng quá mua/quá bán. Ba chiều chỉ báo phát tín hiệu đồng thời có thể lọc bỏ phần lớn tín hiệu nhiễu, nâng cao tỷ lệ thành công khi vào lệnh.

Ngoài ra, chiến lược có thêm chức năng chốt lời, có thể khóa một phần lợi nhuất nhất định, có lợi cho quản lý vốn.

Phân tích rủi ro

Rủi ro chính của chiến lược này là quyết định mua/bán phụ thuộc vào các chỉ báo phát tín hiệu đồng bộ; nếu một số chỉ báo phát tín hiệu sai, có thể dẫn đến quyết định sai. Ví dụ, Stochastic RSI phát tín hiệu quá mua, nhưng VWAP và ngưỡng hỗ trợ/kháng cự vẫn nhận định tăng, khi đó có thể bỏ lỡ điểm mua và không vào lệnh.

Ngoài ra, thông số chỉ báo cài đặt không phù hợp cũng có thể dẫn đến sai lầm trong nhận định tín hiệu, cần phải backtest nhiều lần để tìm ra thông số tối ưu.

Hơn nữa, thị trường chứng khoán thường xảy ra các sự kiện thiên nga đen trong ngắn hạn, khiến chỉ báo mất hiệu lực. Để phòng ngừa rủi ro này, có thể thêm chiến lược cắt lỗ, tránh thua lỗ quá lớn cho một lệnh.

Hướng tối ưu hóa

Chiến lược này có thể tiếp tục tối ưu hóa từ các khía cạnh sau:

-

Thêm nhiều tín hiệu chỉ báo hơn, ví dụ chỉ báo khối lượng, để đánh giá sức mạnh xu hướng, nâng cao độ chính xác khi ra quyết định.

-

Bổ sung mô hình học máy, huấn luyện dựa trên các chỉ báo đa chiều, tự động tìm kiếm chiến lược giao dịch tối ưu.

-

Tối ưu hóa thông số theo từng sản phẩm khác nhau, thiết lập thông số thích ứng.

-

Thêm chiến lược cắt lỗ và kiểm soát kích thước vị thế dựa trên mức sụt giảm, để kiểm soát rủi ro tốt hơn.

-

Thực hiện tối ưu hóa danh mục, tìm các sản phẩm có tương quan thấp để kết hợp, giảm mức sụt giảm của danh mục.

Tổng kết

Nhìn chung, chiến lược này rất phù hợp cho giao dịch xu hướng ngắn hạn. Nó sử dụng các chỉ báo đa chiều để ra quyết định, có thể lọc bỏ nhiều nhiễu, tỷ lệ thắng cao. Tuy nhiên, vẫn cần chú ý đến rủi ro chỉ báo phát tín hiệu sai; thông qua việc tối ưu hóa tiếp tục, chiến lược này có tiềm năng trở thành chiến lược ngắn hạn hiệu quả và ổn định.

- 1