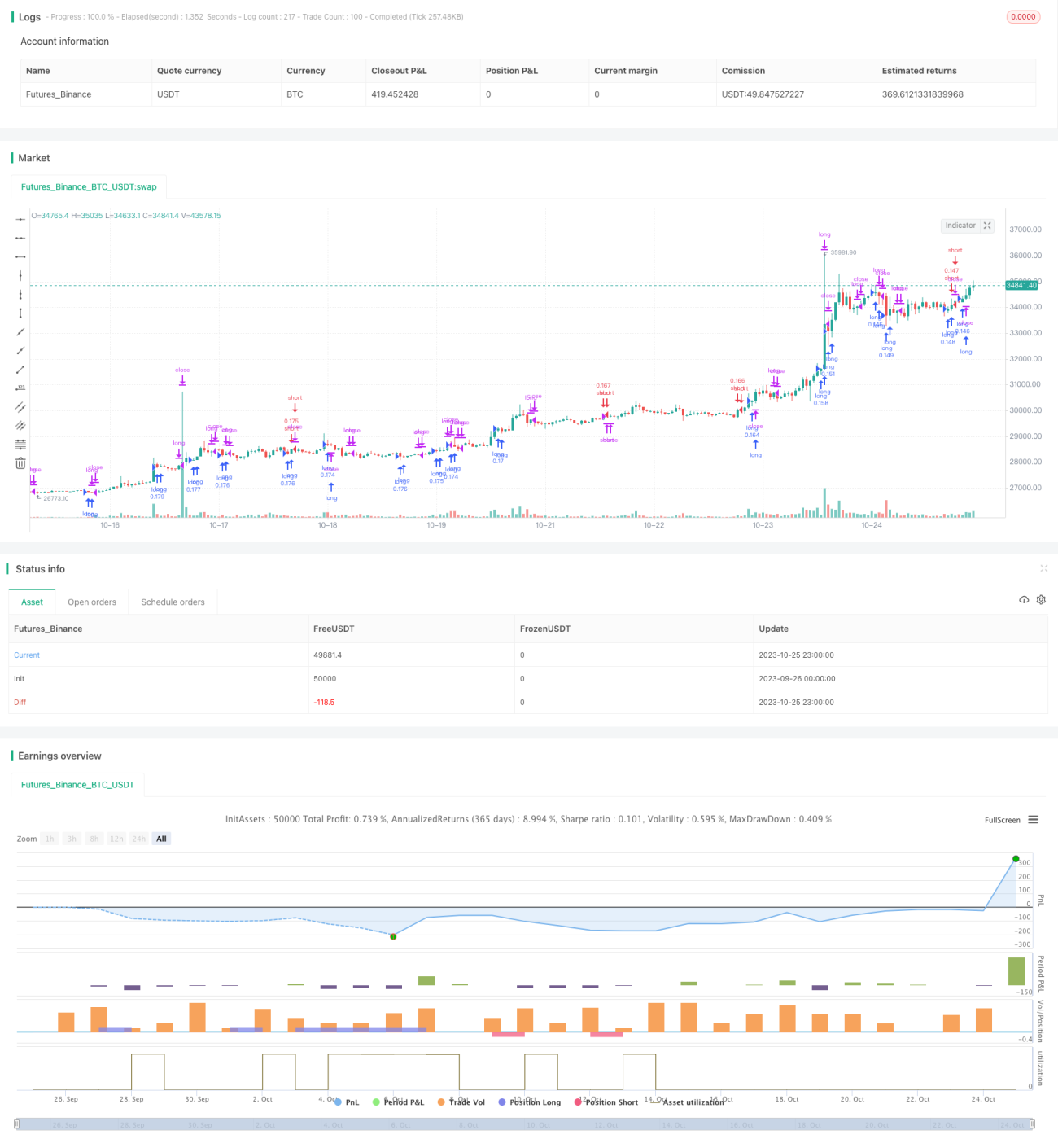

Chiến lược giao cắt đường trung bình động

Tổng quan

Chiến lược giao cắt đường trung bình động là một chiến lược momentum, sử dụng tín hiệu giao cắt của hai đường trung bình động để xác định hướng xu hướng, tạo ra tín hiệu mua và bán. Chiến lược này sử dụng 2 đường trung bình động đơn giản và 1 đường trung bình động hàm mũ, dựa vào sự giao cắt của chúng để xác định xu hướng tăng giảm, thuộc chiến lược giao dịch trung và ngắn hạn.

Nguyên lý chiến lược

Chiến lược này sử dụng 3 đường trung bình động:

- EMA1: Một đường trung bình động hàm mũ với chu kỳ ngắn hơn, đại diện cho đường nhanh

- SMA1: Một đường trung bình động đơn giản với chu kỳ dài hơn, đại diện cho đường chậm

- SMA2: Một đường trung bình động đơn giản với chu kỳ dài hơn nữa, xác định hướng xu hướng

Chiến lược xác định xu hướng dựa trên mối quan hệ giữa EMA1, SMA1 và SMA2:

- Xu hướng tăng: EMA1 > SMA1 > SMA2

- Xu hướng giảm: EMA1 < SMA1 < SMA2

Tín hiệu vào lệnh:

- Vào lệnh mua: Khi đường nhanh cắt lên trên đường chậm, mua lên

- Vào lệnh bán: Khi đường nhanh cắt xuống dưới đường chậm, bán xuống

Tín hiệu thoát lệnh:

- Thoát lệnh mua: Đóng vị thế khi đường nhanh cắt xuống dưới đường chậm

- Thoát lệnh bán: Đóng vị thế khi đường nhanh cắt lên trên đường chậm

Chiến lược này cung cấp nhiều tùy chọn tham số, có thể chọn các đường trung bình động khác nhau để xác định điểm vào và thoát.

Phân tích ưu điểm

Chiến lược này có những ưu điểm sau:

- Bắt kịp momentum: Có thể nắm bắt sự thay đổi của xu hướng thị trường, chiến lược momentum

- Cấu hình linh hoạt: Cung cấp nhiều lựa chọn đường trung bình động, có thể cấu hình linh hoạt

- Lọc xu hướng: Sử dụng đường trung bình động chu kỳ dài để xác định hướng xu hướng, tránh giao dịch ngược xu hướng

- Quản lý rủi ro: Có thể cấu hình stop loss và take profit, kiểm soát rủi ro từng giao dịch

Phân tích rủi ro

Chiến lược này cũng tồn tại những rủi ro sau:

- Whipsaws: Trước khi breakout có thể xuất hiện dao động liên tục dẫn đến nhiều tín hiệu giả

- Nhạy cảm với tham số MA: Cài đặt tham số đường trung bình động không phù hợp có thể dẫn đến quá thường xuyên hoặc không đủ nhạy

- Độ trễ: Bản chất đường trung bình động có độ trễ, có thể bỏ lỡ thời điểm breakout tốt nhất

- Không có yếu tố cơ bản: Hoàn toàn dựa trên chỉ báo kỹ thuật, không xem xét yếu tố cơ bản

Đối với rủi ro whipsaws, có thể điều chỉnh chu kỳ đường trung bình động phù hợp; đối với rủi ro nhạy cảm tham số, có thể tối ưu hóa tham số; đối với rủi ro độ trễ, có thể kết hợp các chỉ báo dẫn dắt khác để tối ưu.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

- Thêm bộ lọc chỉ báo kỹ thuật khác, ví dụ RSI, Bollinger Bands, v.v., cải thiện chất lượng tín hiệu

- Tối ưu hóa tham số chu kỳ đường trung bình động, tìm tham số tối ưu

- Thêm mô hình học máy để xác định xu hướng và độ tin cậy của tín hiệu

- Kết hợp khối lượng giao dịch, tránh breakout giả khi khối lượng thấp

- Kết hợp yếu tố cơ bản, tránh giao dịch ngược chu kỳ kinh tế

Tổng kết

Chiến lược giao cắt đường trung bình động nhìn chung khá đơn giản và trực tiếp, xác định hướng xu hướng và thời điểm tham gia dựa trên giao cắt của đường trung bình nhanh và chậm. Ưu điểm của chiến lược này là có thể bắt kịp momentum, cấu hình tham số linh hoạt, nhưng cũng tồn tại một số rủi ro về whipsaw, độ trễ, v.v. Bằng cách đưa vào các chỉ báo khác để lọc và tối ưu hóa, chiến lược này có thể trở thành một chiến lược giao dịch định lượng rất thực tế.

- 1