Chiến lược giao dịch giao cắt đường trung bình động (MA) theo xu hướng

Tổng quan

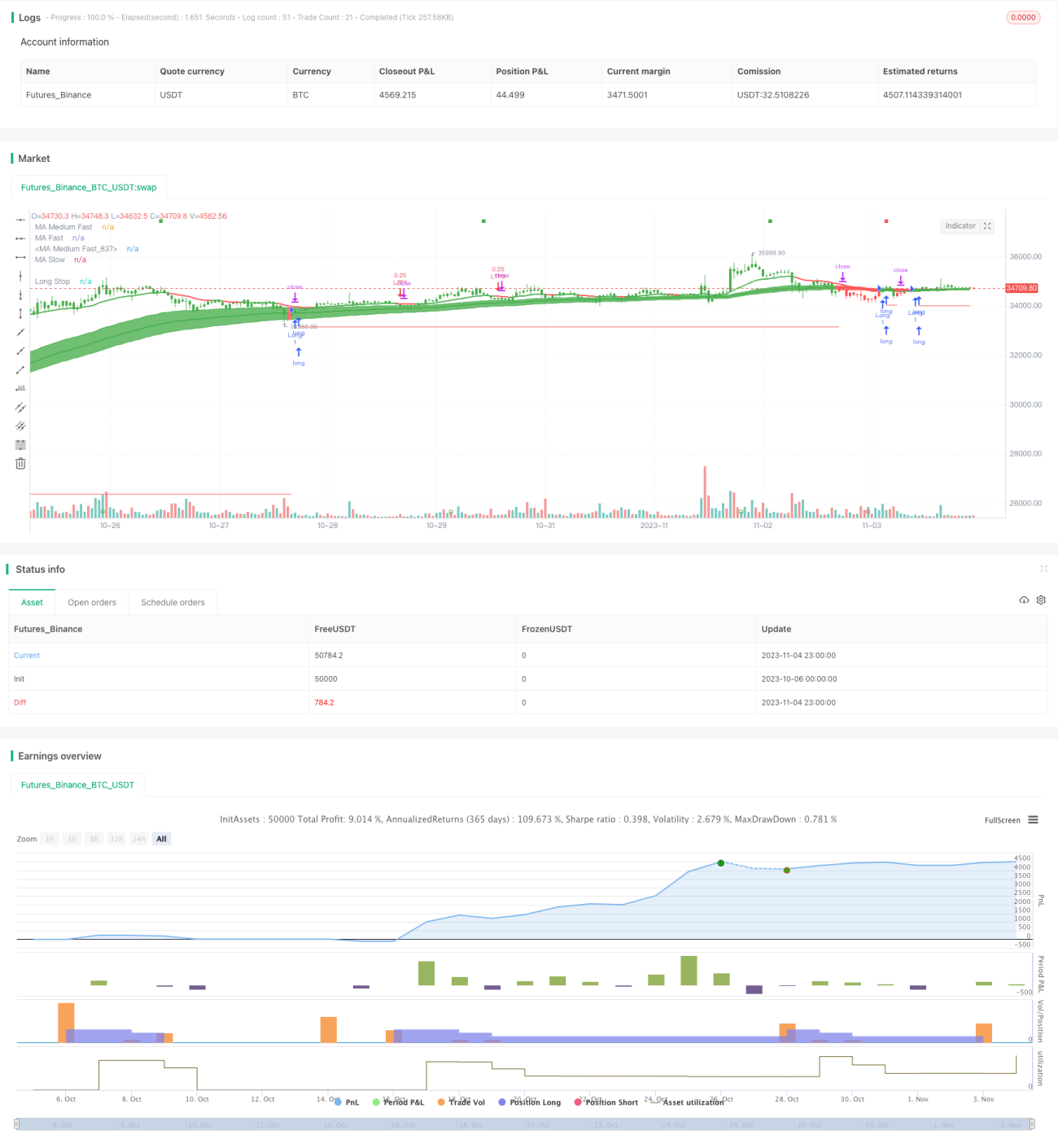

Chiến lược này là một chiến lược giao dịch theo xu hướng dựa trên đường trung bình động. Nó sử dụng ba đường trung bình động Hull với các tham số khác nhau để xác định hướng xu hướng giá, kết hợp với bộ lọc ATR nhanh để nhận biết sớm các đảo chiều xu hướng tiềm năng. Khi ba đường trung bình nhanh, trung bình và chậm giao cắt lên hoặc xuống, sẽ phát ra tín hiệu mua hoặc bán. Chiến lược này cũng có chức năng cắt lỗ di động và chốt lời di động, giúp kiểm soát rủi ro hiệu quả.

Nguyên lý chiến lược

Chiến lược sử dụng ba đường trung bình động Hull để xác định xu hướng giá, bao gồm một đường Hull MA nhanh, một đường Hull MA trung bình và một đường Hull MA chậm. Dựa vào sự giao cắt của chúng để xác định hướng xu hướng:

-

Khi đường nhanh cắt lên trên đường trung bình, cho thấy giá đang bước vào xu hướng tăng, phát ra tín hiệu mua.

-

Khi đường nhanh cắt xuống dưới đường trung bình, cho thấy giá đang bước vào xu hướng giảm, phát ra tín hiệu bán.

Để tăng độ nhạy trong việc nhận biết đảo chiều xu hướng, chiến lược đưa vào bộ lọc ATR nhanh dựa trên RSI. Bộ lọc này có thể đo lường sự biến động của giá, khi xu hướng giá thay đổi, giá trị của nó sẽ thay đổi rõ rệt. Do đó, chúng ta có thể dựa vào sự phá vỡ lên/xuống của bộ lọc ATR để nhận biết sớm sự đảo chiều xu hướng giá.

Cụ thể, hàm filtr thực hiện logic tính toán của bộ lọc ATR nhanh này. Nó dựa trên giá trị RSI để tính toán độ lớn của ATR. Khi giá trị ATR cắt lên hoặc cắt xuống đường RSI, có thể báo hiệu sự thay đổi của xu hướng giá.

Ngoài ra, chiến lược thiết lập các điều kiện cắt lỗ di động và chốt lời di động, có thể tự động quản lý rủi ro theo tỷ lệ phần trăm cắt lỗ và chốt lời đã đặt.

Phân tích ưu điểm

-

Sử dụng ba đường Hull MA để xác định hướng xu hướng, có thể lọc nhiễu thị trường hiệu quả, nhận diện xu hướng trung và dài hạn.

-

Ứng dụng bộ lọc ATR nhanh giúp tăng khả năng nhận biết sớm đảo chiều xu hướng.

-

Tự động nắm bắt cơ hội đảo chiều xu hướng, điều chỉnh vị thế kịp thời, không bỏ lỡ mua hay bán.

-

Cắt lỗ và chốt lời di động thiết lập sự cân bằng động giữa rủi ro và lợi nhuận.

-

Có thể tùy chỉnh tham số, phù hợp với các thị trường và sản phẩm giao dịch khác nhau.

Phân tích rủi ro

-

Chiến lược giao cắt MA dễ phát sinh tín hiệu giả tăng và giảm, cần bộ lọc ATR hỗ trợ xác nhận.

-

Trong thị trường biến động mạnh, MA dễ xảy ra giao cắt thường xuyên, cần theo dõi chặt chẽ đường ATR.

-

Điểm dừng lỗ quá nhỏ dễ bị chạm, quá lớn lại khó kiểm soát thua lỗ. Cần điều chỉnh tham số tùy tình hình cụ thể.

-

Chiến lược này phù hợp hơn với thị trường có xu hướng, không nên dùng cho thị trường đi ngang.

-

Có thể tối ưu hóa tham số, chọn bộ MA và chu kỳ ATR tốt nhất để giảm tỷ lệ tín hiệu giả.

Hướng tối ưu

-

Có thể thử đổi loại MA thành DEMA, TEMA và các biến thể EMA khác để xem có lọc được nhiều nhiễu hơn không.

-

Bộ lọc ATR có thể đổi thành đường MIDDLE của Keltner Channel để kiểm tra khả năng nhận biết đảo chiều.

-

Có thể thử nghiệm các tổ hợp tham số MA khác nhau để tìm cặp tham số tối ưu.

-

Có thể thử nghiệm tham số chu kỳ ATR để tìm hiệu ứng làm mịn tốt nhất.

-

Có thể thêm chỉ báo khối lượng để hỗ trợ đánh giá khả năng phá vỡ thật/giả.

-

Có thể thử nghiệm thêm các chỉ báo khác như MACD để tăng độ tin cậy của tín hiệu.

Tổng kết

Chiến lược này tích hợp nhiều chức năng: đường trung bình động xác định hướng xu hướng, bộ lọc ATR phát hiện sớm đảo chiều và tự động cắt lỗ/chốt lời quản lý rủi ro. Nó có thể tự động theo dõi xu hướng, kịp thời nắm bắt cơ hội đảo chiều, và thông qua tối ưu hóa tham số có thể phù hợp với nhiều sản phẩm và khung thời gian khác nhau – một chiến lược giao dịch theo xu hướng rất thực tế. Ưu điểm của nó là logic chiến lược đơn giản rõ ràng và phương pháp kiểm soát rủi ro hiệu quả. Tuy nhiên, cũng cần lưu ý đến vấn đề tín hiệu giả và cài đặt điểm dừng lỗ. Thông qua tối ưu hóa tiếp theo, có thể đạt được hiệu quả chiến lược tốt hơn.

- 1