Chiến lược theo dõi xu hướng gốc dựa trên đường trung bình động

Tổng quan

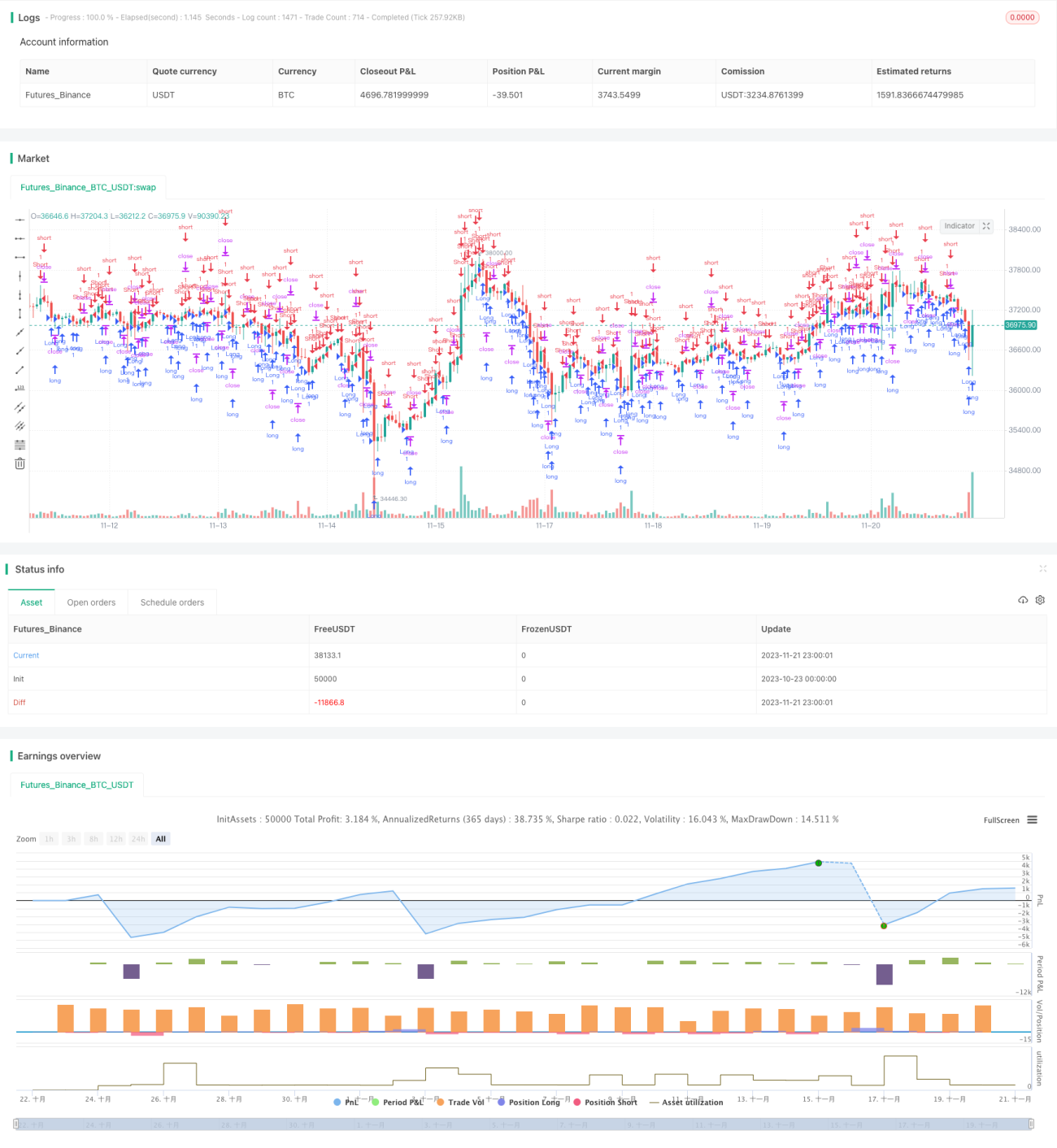

Chiến lược này dựa trên phần thân của nến (candle), kết hợp với chỉ báo EMA để đánh giá hướng xu hướng thị trường, đạt được hiệu quả THEO DÕI XU HƯỚNG GỐC (ORIGINAL PRIMITIVE TREND TRACKING). Khi xuất hiện nến xanh lớn thì vào lệnh mua, khi xuất hiện nến đỏ lớn thì vào lệnh bán, từ đó theo dõi xu hướng thị trường.

Nguyên lý chiến lược

- Tính độ dài trung bình thân nến (sbody) của 30 cây nến gần nhất.

- Khi nến mới nhất là nến xanh, độ dài thân nến lớn hơn sbody/2, thì vào lệnh mua.

- Khi đã mua, nếu nến mới nhất là nến đỏ, độ dài thân nến lớn hơn sbody/2, và vị thế hiện tại đang có lãi, thì đóng vị thế mua.

- Khi nến mới nhất là nến đỏ, độ dài thân nến lớn hơn sbody/2, thì vào lệnh bán.

- Khi đã bán, nếu nến mới nhất là nến xanh, độ dài thân nến lớn hơn sbody/2, và vị thế hiện tại đang có lãi, thì đóng vị thế bán.

Phân tích ưu điểm

Chiến lược này có các ưu điểm sau:

- Nguyên thủy và đơn giản, dễ hiểu và dễ thực hiện.

- Dựa trên cấu trúc nến để phán đoán, có hiệu quả nhất định đối với các đột phá giao dịch (Trading Breakouts).

- Theo dõi xu hướng, có thể bắt được các biến động lớn.

- Dừng lỗ nhanh sau khi vị thế có lãi, giúp chốt lợi nhuận.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro:

- Không thể lọc hiệu quả các đột phá giả, có thể dẫn đến thua lỗ không cần thiết.

- Chỉ dựa trên phán đoán nến dễ bị ảnh hưởng bởi trượt giá và gap qua đêm.

- Chưa xem xét vấn đề tần suất giao dịch quá cao.

Có thể giảm thiểu rủi ro bằng các phương pháp sau:

- Kết hợp các chỉ báo khác để lọc tín hiệu.

- Thiết lập chiến lược dừng lỗ.

- Tối ưu hóa tham số, kiểm soát tần suất giao dịch.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa theo các hướng sau:

- Thêm chỉ báo đột phá để lọc đột phá giả.

- Thêm chiến lược dừng lỗ để giảm thua lỗ mỗi lệnh.

- Kết hợp chỉ báo xu hướng để kiểm tra hướng xu hướng.

- Tối ưu hóa tham số để tìm ra tổ hợp tham số tốt nhất.

Tổng kết

Chiến lược này thuộc loại chiến lược theo dõi xu hướng đơn giản nguyên thủy. Thông qua cấu trúc nến, có thể theo dõi hiệu quả hướng xu hướng. Đồng thời thiết lập cơ chế dừng lỗ nhanh để chốt lợi nhuận. Chiến lược này có thể bổ sung cho các tổ hợp theo dõi xu hướng, nhưng vẫn cần tối ưu hóa để giảm rủi ro. Trong tương lai, đáng để nghiên cứu thêm hiệu quả khi kết hợp với các chỉ báo khác.

/*backtest

start: 2023-10-23 00:00:00

end: 2023-11-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy(title = "Noro's Primitive Strategy v1.0", shorttitle = "Primitive str 1.0", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100.0, pyramiding = 10)

//Settings- 1