Chiến lược ghép cặp hai kênh động lượng và đảo chiều

Tổng quan

Chiến lược này kết hợp tổng hợp nhiều chỉ báo kỹ thuật, thực hiện đảo chiều động lượng và ghép cặp song ray, tạo thành tín hiệu giao dịch. Chiến lược sử dụng mô hình 123 để xác định điểm đảo chiều, kết hợp với chỉ báo ergodic CSI tạo thành tín hiệu cặp, thực hiện theo dõi xu hướng. Chiến lược này nhằm nắm bắt xu hướng trung và ngắn hạn, đạt lợi nhuận cao.

Nguyên lý chiến lược

Chiến lược này bao gồm hai phần:

- Mô hình 123 xác định điểm đảo chiều

- Chỉ báo ergodic CSI tạo tín hiệu cặp

Mô hình 123 xác định đảo chiều giá dựa trên mối quan hệ giá đóng cửa của 3 cây nến gần nhất. Logic xác định cụ thể:

Nếu hai cây nến trước đó có giá đóng cửa sau tăng và chỉ báo stoch nhanh và chậm hiện tại đều dưới 50, thì đó là tín hiệu mua.

Nếu hai cây nến trước đó có giá đóng cửa sau giảm và chỉ báo stoch nhanh và chậm hiện tại đều trên 50, thì đó là tín hiệu bán.

Chỉ báo ergodic CSI xem xét nhiều yếu tố như giá, biên độ thực, chỉ báo xu hướng, tổng hợp đánh giá diễn biến thị trường, tạo ra vùng mua bán.

Khi chỉ báo cao hơn vùng mua, phát sinh tín hiệu mua; khi thấp hơn vùng bán, phát sinh tín hiệu bán.

Cuối cùng, tín hiệu đảo chiều từ mô hình 123 kết hợp với tín hiệu đường ray từ ergodic CSI thông qua phép toán AND để có tín hiệu chiến lược cuối cùng.

Ưu điểm của chiến lược

- Nắm bắt xu hướng trung và ngắn hạn, tiềm năng lợi nhuận lớn

- Nhận diện mô hình đảo chiều, có thể nắm bắt hiệu quả điểm xoay chiều

- Ghép cặp song ray, giảm tín hiệu giả

Rủi ro của chiến lược

- Hành vi cổ phiếu riêng lẻ có thể phân kỳ, dẫn đến cắt lỗ

- Mô hình đảo chiều dễ bị ảnh hưởng bởi thị trường dao động

- Không gian tối ưu hóa tham số hạn chế, hiệu quả biến động lớn

Hướng tối ưu hóa

- Tối ưu hóa tham số, nâng cao hiệu quả lợi nhuận của chiến lược

- Thêm logic cắt lỗ, giảm thua lỗ mỗi giao dịch

- Kết hợp mô hình đa nhân tố, nâng cao chất lượng chọn cổ phiếu

Tổng kết

Chiến lược này thông qua mô hình đảo chiều và ghép cặp song ray, đã thực hiện theo dõi hiệu quả xu hướng trung và ngắn hạn. So với chỉ báo kỹ thuật đơn lẻ, nó có độ ổn định và mức lợi nhuận cao hơn. Bước tiếp theo sẽ tiếp tục tối ưu hóa tham số, đồng thời bổ sung module cắt lỗ và chọn cổ phiếu, nhằm giảm sụt giảm và nâng cao hiệu quả tổng thể.

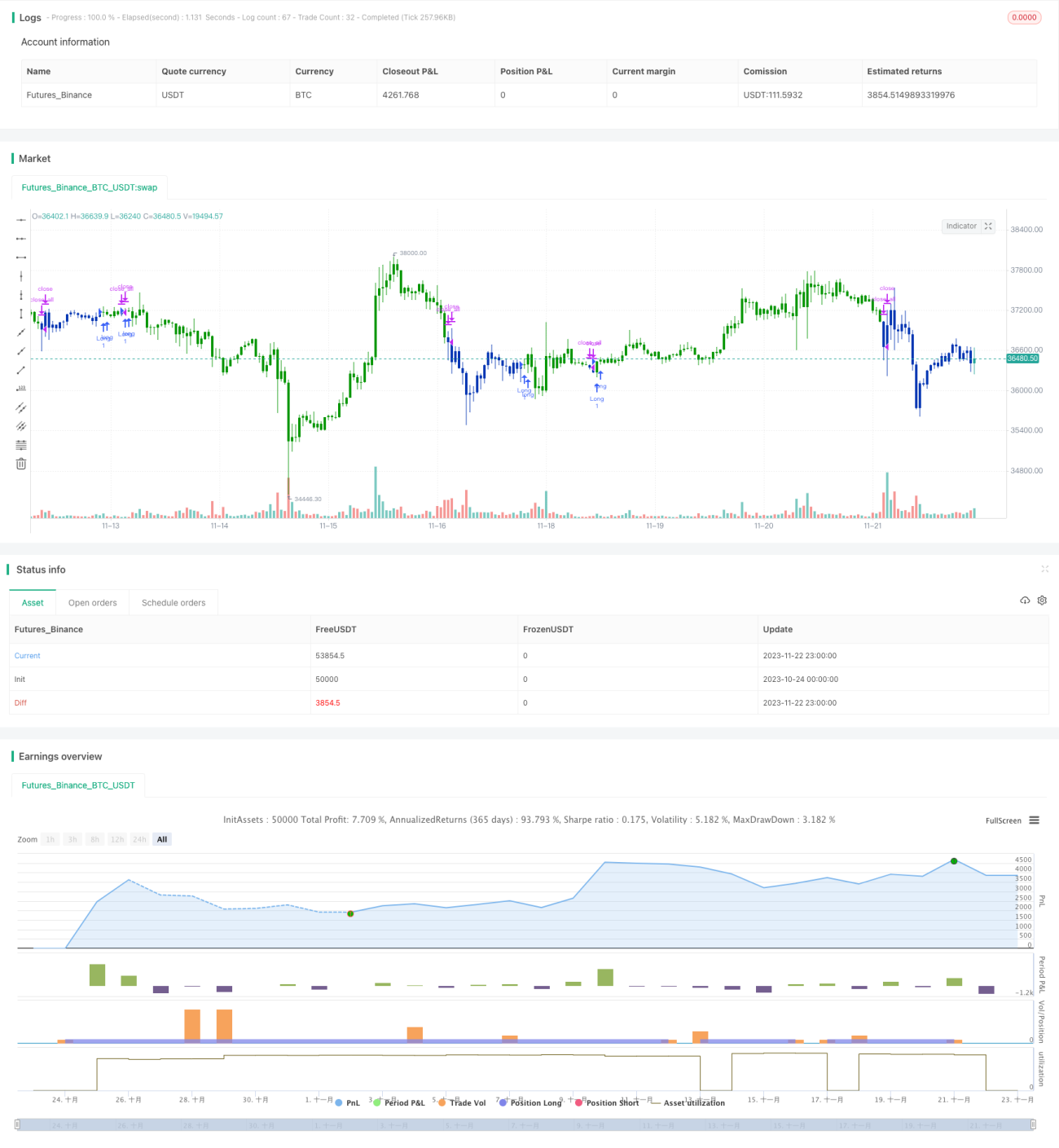

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 22/07/2020

// This is combo strategies for get a cumulative signal. - 1