Chiến lược đột phá Rùa kép

Tổng quan

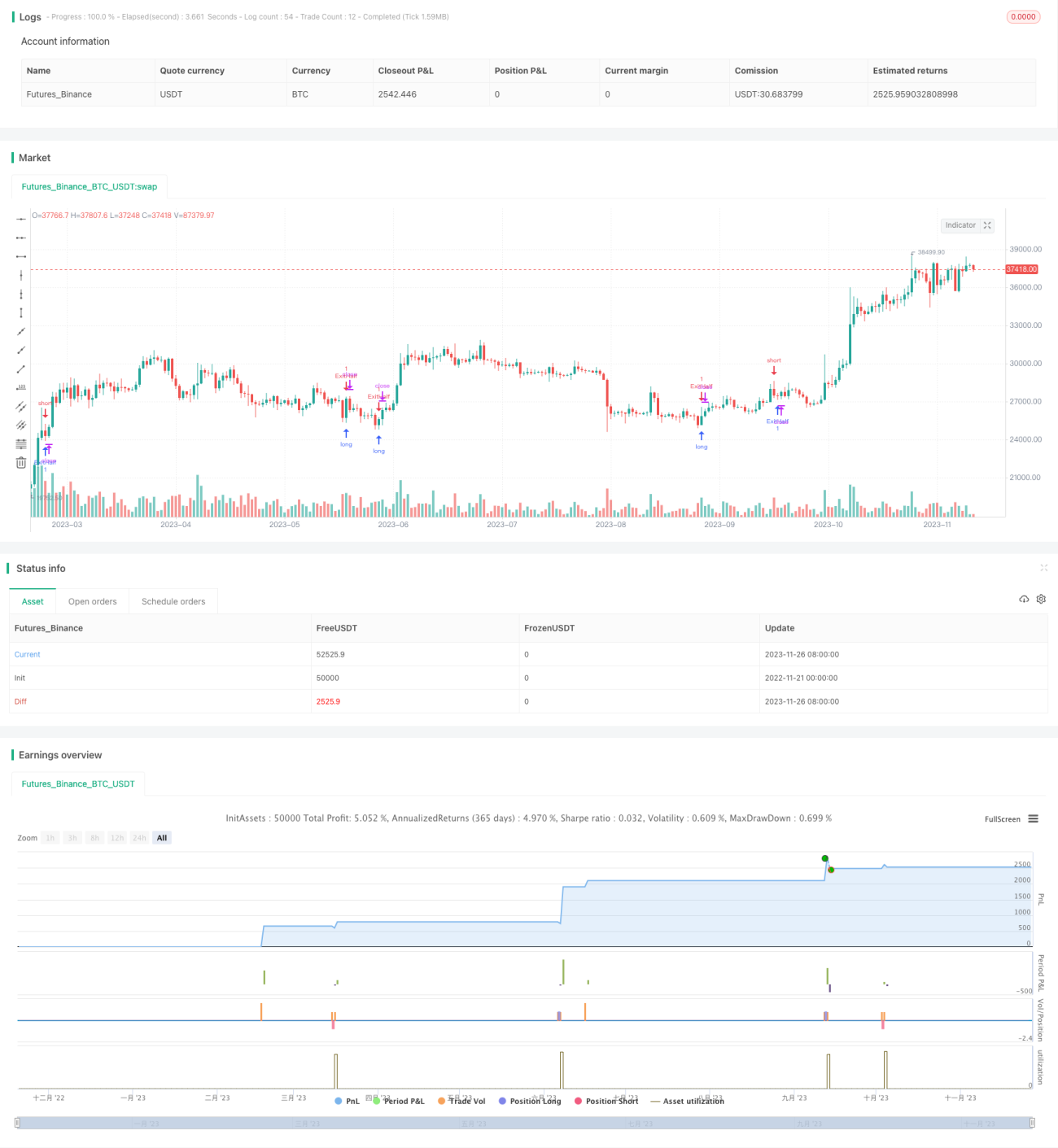

Chiến lược đột phá Rùa Đôi kết hợp chiến lược đột phá của phương pháp giao dịch Rùa và nguyên lý trailing stop loss của Linda Raschke, mang lại hiệu suất đột phá xuất sắc và kiểm soát rủi ro chặt chẽ. Chiến lược này đồng thời theo dõi các mức đột phá lên và xuống của giá, thiết lập vị thế mua hoặc bán khi xảy ra đột phá, và quản lý vị thế bằng trailing stop loss và trailing take profit.

Nguyên lý chiến lược

Logic cốt lõi là bán khống khi giá phá vỡ đỉnh của chu kỳ lớn nhưng thấp hơn đỉnh của chu kỳ nhỏ, và mua khi giá phá vỡ đáy của chu kỳ lớn nhưng cao hơn đáy của chu kỳ nhỏ. Sau khi vào lệnh, thiết lập trailing stop loss và trailing take profit, trước hết dừng lỗ để xác nhận rủi ro. Khi số lượng vị thế tích lũy đạt đến số lượng take profit đã cài đặt, ở chu kỳ tiếp theo hủy lệnh dừng lỗ, sau đó thoát một nửa vị thế và thiết lập trailing stop loss và trailing take profit để khóa lợi nhuận và theo dõi chênh lệch giá.

Các bước thực hiện cụ thể:

- Tính toán đỉnh của chu kỳ lớn (20 chu kỳ) prevHigh và đỉnh của chu kỳ nhỏ (4 chu kỳ) smallPeriodHigh.

- Khi high của nến mới nhất lớn hơn prevHigh, và prevHigh lớn hơn smallPeriodHigh, điều đó cho thấy đỉnh của chu kỳ lớn phá vỡ đỉnh của chu kỳ nhỏ, lúc này nếu không có vị thế thì bán khống.

- Sau khi vào lệnh, thiết lập trailing stop loss, khi vị thế đảo chiều thì hủy lệnh dừng lỗ, tránh bị dừng lỗ.

- Khi số lượng vị thế đạt đến số chu kỳ trailing take profit đã cài đặt (hiện tại là 0 chu kỳ), ở chu kỳ tiếp theo thoát một nửa vị thế, và thiết lập trailing stop loss và trailing take profit, theo dõi chênh lệch giá và khóa lợi nhuận.

- Đối với đột phá đáy cũng tương tự, dựa trên mối quan hệ đột phá giữa đáy của chu kỳ lớn và đáy của chu kỳ nhỏ để thiết lập vị thế mua.

Phân tích ưu điểm

Đây là một chiến lược đột phá toàn diện, đồng thời có những ưu điểm sau:

- Kết hợp phương pháp giao dịch Rùa hai chu kỳ, có thể nhận diện tín hiệu đột phá hiệu quả.

- Sử dụng kỹ thuật trailing stop loss và trailing take profit để kiểm soát rủi ro chặt chẽ, tránh thua lỗ lớn.

- Thoát lệnh hai lần: lần đầu take profit một nửa vị thế, sau đó trailing take profit toàn bộ vị thế, khóa lợi nhuận.

- Kết hợp cả giao dịch mua và bán hai chiều, phù hợp với đặc điểm thị trường đan xen tăng giảm.

- Hiệu quả backtest xuất sắc, có khả năng thực chiến mạnh mẽ.

Phân tích rủi ro

Các rủi ro chính và biện pháp đối phó như sau:

- Rủi ro đột phá giả. Cần điều chỉnh tham số chu kỳ phù hợp để đảm bảo tính hiệu quả của đột phá.

- Rủi ro đuổi theo giá. Cần kết hợp xu hướng và hình thái để lọc, tránh vào lệnh vào cuối xu hướng.

- Rủi ro bị quét stop loss. Có thể nới rộng biên độ dừng lỗ một cách phù hợp, đảm bảo có đủ không gian.

- Rủi ro trailing stop loss quá nhạy. Cần điều chỉnh cài đặt trượt giá sau stop loss, tránh dừng lỗ vô ích.

Hướng tối ưu hóa

Chiến lược này còn có thể được tối ưu hóa từ các khía cạnh sau:

- Thêm bộ lọc đột phá khối lượng giao dịch để đảm bảo tính xác thực của đột phá.

- Thêm chỉ báo đánh giá xu hướng, tránh vào lệnh vào cuối xu hướng.

- Kết hợp nhiều khung thời gian hơn để xác định thời điểm đột phá.

- Thêm thuật toán học máy để tối ưu hóa tham số động.

- Kết hợp các chiến lược khác để thực hiện giao dịch chênh lệch thống kê.

Tổng kết

Chiến lược đột phá Rùa Đôi tích hợp toàn diện kỹ thuật hai chu kỳ, lý thuyết đột phá và các phương pháp quản lý rủi ro chặt chẽ, vừa duy trì tỷ lệ thắng cao vừa đảm bảo tính ổn định của lợi nhuận. Mô hình chiến lược này đơn giản, rõ ràng, dễ hiểu và dễ áp dụng, là một chiến lược định lượng xuất sắc. Chiến lược này còn có không gian tối ưu hóa rất lớn, nhà đầu tư có thể sáng tạo dựa trên đó để xây dựng hệ thống giao dịch tốt hơn.

- 1