Chiến lược giao dịch sóng định lượng dựa trên đa khung thời gian

1

Follow

1802

Followers

Tổng quan

Chiến lược này kết hợp các chỉ báo định lượng trên các khung thời gian khác nhau để nhận diện các sóng giá của Bitcoin, từ đó thực hiện giao dịch theo xu hướng. Chiến lược sử dụng khung thời gian 5 phút, nắm giữ dài hạn để thu lợi từ các sóng.

Nguyên lý chiến lược

- Dựa trên chỉ báo RSI tính toán trên khung thời gian ngày, sử dụng khối lượng để tính trọng số, nhằm lọc các phá vỡ giả.

- Thực hiện làm mịn EMA cho chỉ báo RSI ngày, xây dựng chỉ báo sóng định lượng.

- Khung thời gian 5 phút sử dụng chỉ báo hồi quy tuyến tính và chỉ báo HMA để tạo tín hiệu giao dịch.

- Chiến lược kết hợp chỉ báo sóng định lượng và tín hiệu giao dịch, tạo sự liên kết giữa các khung thời gian khác nhau, nhận diện các sóng trung và dài hạn của giá.

Phân tích ưu điểm

- Chỉ báo RSI có trọng số khối lượng giúp nhận diện hiệu quả các sóng thực, lọc các phá vỡ giả.

- Chỉ báo HMA nhạy cảm hơn với biến động giá, có thể kịp thời bắt được các điểm đảo chiều.

- Kết hợp nhiều khung thời gian giúp nhận diện sóng trung và dài hạn chính xác hơn.

- Giao dịch trên khung thời gian 5 phút cho tần suất hoạt động cao hơn.

- Chiến lược theo đuổi sóng, không cần chọn điểm chính xác, thời gian nắm giữ lâu hơn.

Phân tích rủi ro

- Các chỉ báo định lượng có thể phát tín hiệu sai, khuyến nghị kết hợp phân tích cơ bản.

- Sóng có thể đảo chiều giữa chừng, cần thiết lập cơ chế cắt lỗ.

- Tín hiệu giao dịch có độ trễ, có thể bỏ lỡ điểm vào lệnh tối ưu.

- Sóng có lợi nhuận yêu cầu thời gian nắm giữ dài, cần chịu áp lực vốn nhất định.

Hướng tối ưu hóa

- Kiểm tra hiệu quả của chỉ báo RSI với các tham số khác nhau.

- Thử nghiệm đưa vào các chỉ báo sóng hỗ trợ khác.

- Tối ưu hóa tham số độ dài của chỉ báo HMA.

- Thêm chiến lược cắt lỗ và chốt lời.

- Điều chỉnh chu kỳ nắm giữ của giao dịch sóng.

Tổng kết

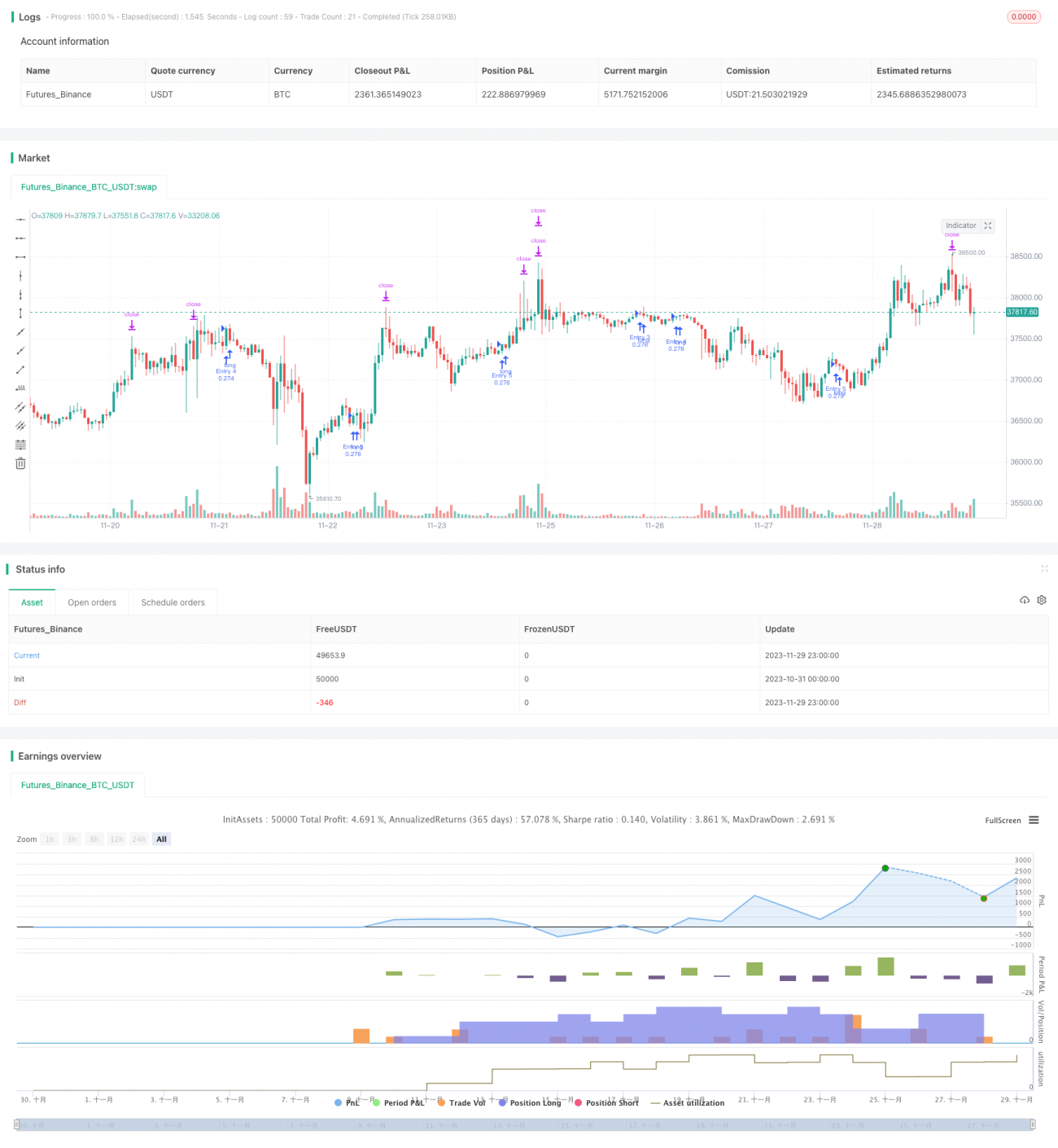

Chiến lược này thông qua việc kết hợp nhiều khung thời gian và phương pháp theo đuổi sóng, đã đạt được hiệu quả trong việc bắt xu hướng trung và dài hạn của Bitcoin. So với giao dịch ngắn hạn, giao dịch sóng trung và dài hạn có mức drawdown nhỏ hơn, không gian lợi nhuận lớn hơn. Bước tiếp theo, thông qua việc điều chỉnh tham số và bổ sung chiến lược quản lý rủi ro, có thể kỳ vọng cải thiện thêm tỷ suất lợi nhuận và tính ổn định của chiến lược.

Source

Pine

/*backtest

start: 2023-10-31 00:00:00

end: 2023-11-30 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title='Pyramiding BTC 5 min', overlay=true, pyramiding=5, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=20, commission_type=strategy.commission.percent, commission_value=0.075)

//the pyramide based on this script https://www.tradingview.com/script/7NNJ0sXB-Pyramiding-Entries-On-Early-Trends-by-Coinrule/Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1