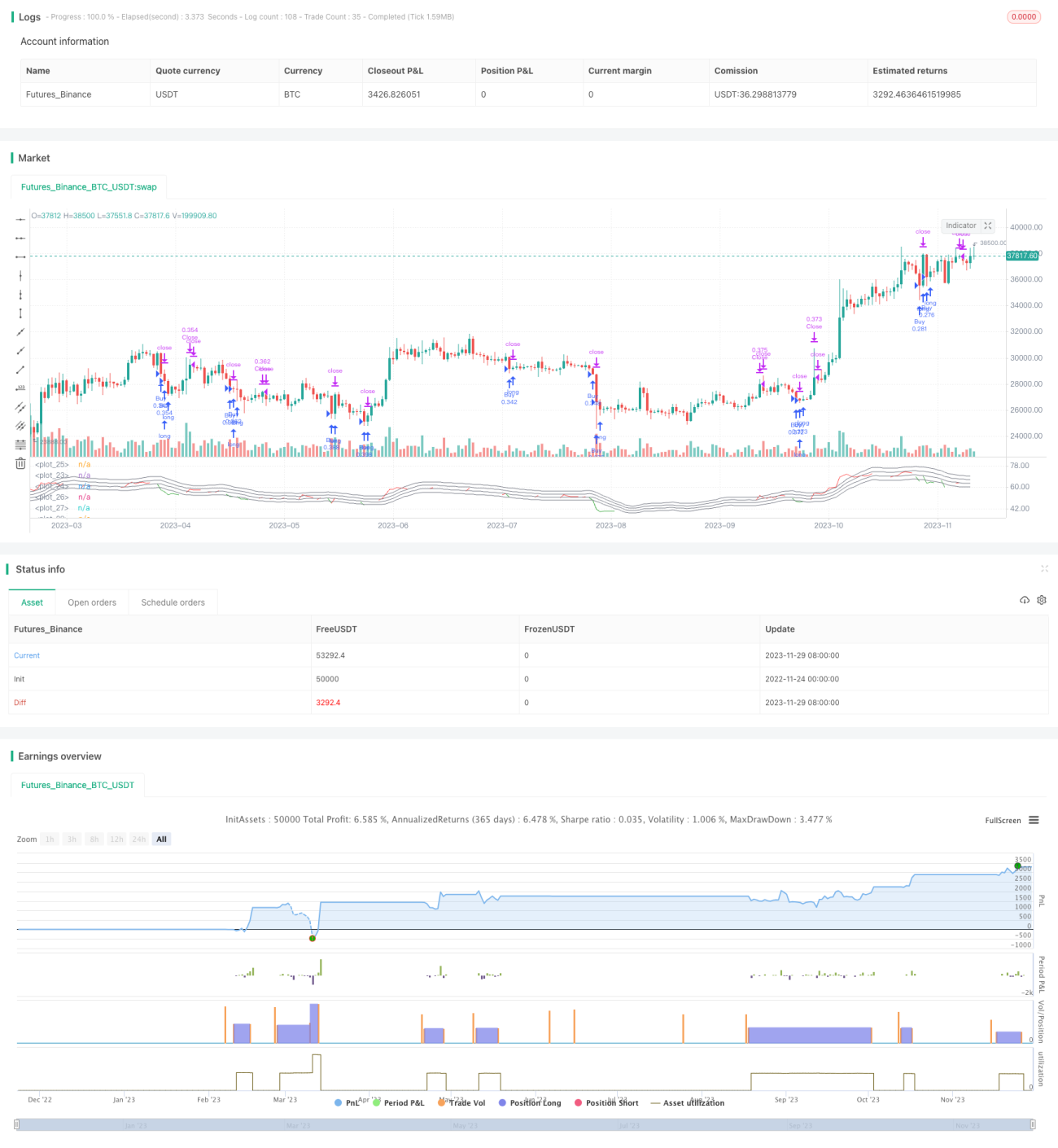

Chiến lược giao dịch định lượng ngắn hạn mua thấp bán cao dựa trên đường trung bình động RSI

Tổng quan

Chiến lược này xác định điểm mua bán dựa trên sự giao nhau giữa chỉ báo RSI và đường trung bình động của nó, thuộc chiến lược giao dịch ngắn hạn. Chiến lược sẽ mua khi chỉ báo RSI thấp hơn đường trung bình động của nó và bán khi cao hơn, đây là chiến lược mua thấp bán cao điển hình.

Nguyên lý chiến lược

- Tính giá trị chỉ báo RSI, với chu kỳ 40 nến

- Tính đường trung bình động MA của chỉ báo RSI, với chu kỳ 10 nến

- Khi RSI thấp hơn đường trung bình động nhân với hệ số (1 - khoảng cách mua bán/100) thì phát tín hiệu mua

- Khi RSI cao hơn đường trung bình động nhân với hệ số (1 + khoảng cách mua bán/100) thì phát tín hiệu bán

- Khoảng cách mua bán mặc định là 5, nghĩa là tín hiệu được tạo ra khi cách đường trung bình động ±5%

- Điều kiện đóng vị thế là khi RSI cao hơn đường trung bình động và cao hơn mức 50

Phân tích ưu điểm

Đây là chiến lược đảo chiều xu hướng điển hình, sử dụng đặc tính quá mua quá bán của chỉ báo RSI để xác định thời điểm mua bán. Chiến lược này có những ưu điểm sau:

- Sử dụng chỉ báo RSI để đánh giá cấu trúc thị trường, bản thân chỉ báo có độ tin cậy khá cao

- Bộ lọc đường trung bình động giúp tránh các giao dịch không cần thiết, tăng cường độ ổn định

- Tham số khoảng cách mua bán có thể điều chỉnh tần suất giao dịch

- Mã nguồn đơn giản dễ hiểu, logic rõ ràng

Nhìn chung, đây là một chiến lược giao dịch ngắn hạn đơn giản và thiết thực.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro cần lưu ý:

- Khả năng chỉ báo RSI phát tín hiệu sai, cần chú ý đến hình thái đường chỉ báo

- Thiết lập khoảng cách mua bán không phù hợp có thể dẫn đến quá nhiều giao dịch hoặc bỏ lỡ cơ hội

- Tần suất giao dịch khá cao, cần xem xét tác động của chi phí giao dịch

- Chỉ dựa trên một chỉ báo duy nhất, dễ bị ảnh hưởng bởi các bất thường của thị trường

Những rủi ro này có thể được giảm thiểu thông qua tối ưu hóa tham số, thêm bộ lọc, v.v.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

- Thêm nhiều chỉ báo lọc hơn, ví dụ chỉ báo khối lượng giao dịch, để đảm bảo tín hiệu chỉ xuất hiện tại các điểm đảo chiều xu hướng

- Thêm chiến lược cắt lỗ, kiểm soát thua lỗ từng lệnh

- Tối ưu hóa khoảng cách mua bán, cân bằng giữa tần suất giao dịch và tỷ lệ lợi nhuận

- Sử dụng thuật toán học máy để tự động tìm kiếm tổ hợp tham số tối ưu

- Thêm mô hình tổng hợp, kết hợp kết quả của nhiều chiến lược con

Thông qua kết hợp nhiều chỉ báo, quản lý cắt lỗ, tối ưu hóa tham số, v.v., có thể cải thiện đáng kể hiệu suất chiến lược.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược giao dịch ngắn hạn rất điển hình và thiết thực. Nó sử dụng trạng thái quá mua quá bán của chỉ báo RSI để xác định thời điểm mua bán, kết hợp với bộ lọc đường trung bình động. Logic chiến lược đơn giản rõ ràng, tham số linh hoạt, dễ triển khai. Tồn tại một số rủi ro thị trường nhất định, nhưng có thể được kiểm soát thông qua hoàn thiện cơ chế vào lệnh và thoát lệnh, tối ưu hóa tham số, v.v. Nếu kết hợp thêm nhiều chỉ báo kỹ thuật và biện pháp quản lý rủi ro, chiến lược này có thể trở thành một chiến lược ngắn hạn mang lại lợi nhuận tương đối ổn định.

- 1