Chiến lược giao dịch chỉ báo đường trung bình động

Tổng quan chiến lược

Chiến lược này dựa trên nhiều chỉ báo đường trung bình động để tạo ra tín hiệu giao dịch. Chiến lược đồng thời theo dõi các đường trung bình động ngắn hạn, trung hạn và dài hạn, dựa vào sự giao nhau của chúng để xác định hướng xu hướng và tạo tín hiệu giao dịch.

Tên chiến lược

Chiến lược giao cắt nhiều đường trung bình động (Multi Moving Average Crossover Strategy)

Nguyên lý chiến lược

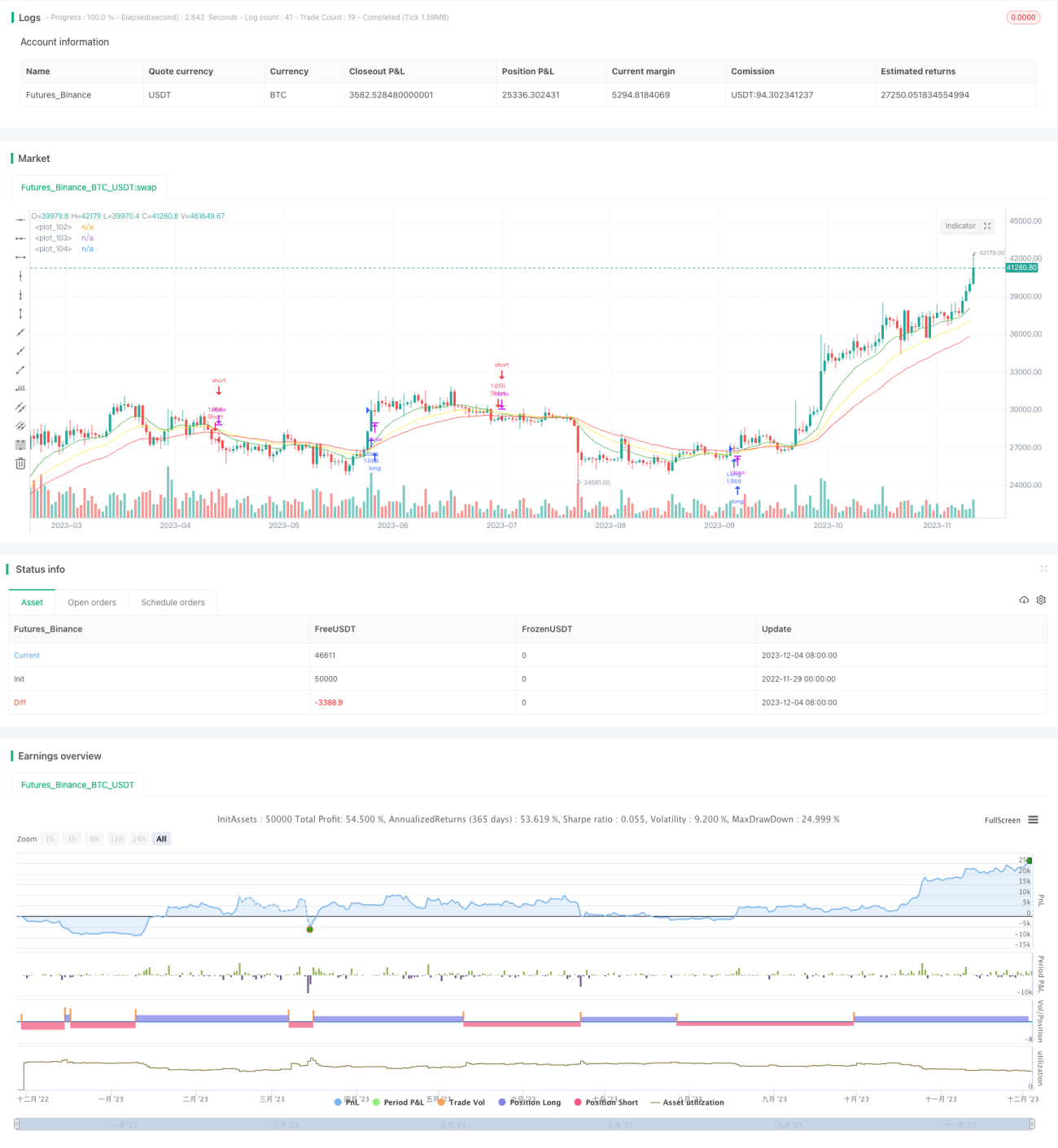

Chiến lược này sử dụng đồng thời 3 đường trung bình động với chu kỳ khác nhau, bao gồm đường 7 ngày, 13 ngày và 21 ngày. Logic giao dịch dựa trên các điểm sau:

- Khi đường trung bình động ngắn hạn 7 ngày cắt lên trên đường trung bình động trung hạn 13 ngày, và đường trung bình động dài hạn 21 ngày đang trong xu hướng tăng, sẽ tạo ra tín hiệu mua (long);

- Khi đường trung bình động ngắn hạn 7 ngày cắt xuống dưới đường trung bình động trung hạn 13 ngày, và đường trung bình động dài hạn 21 ngày đang trong xu hướng giảm, sẽ tạo ra tín hiệu bán (short).

Bằng cách kết hợp các đường trung bình động ở các khung thời gian khác nhau, có thể xác định xu hướng thị trường chính xác hơn, tránh các giao dịch sai lầm.

Ưu điểm của chiến lược

- Sử dụng nhiều nhóm đường trung bình động giúp xác định xu hướng thị trường chính xác hơn, tránh bị đánh lừa bởi các phá vỡ giả hoặc biến động ngắn hạn.

- Chỉ tạo ra tín hiệu khi xu hướng rõ ràng, giúp giảm số lần giao dịch không cần thiết, từ đó giảm chi phí giao dịch.

- Cài đặt tham số linh hoạt, có thể điều chỉnh chu kỳ của đường trung bình động theo sở thích cá nhân, thích ứng với các loại tài sản và môi trường thị trường khác nhau.

Rủi ro của chiến lược

- Trong thị trường dao động (sideway), có thể xuất hiện các tín hiệu sai liên tục.

- Đường trung bình động là chỉ báo theo xu hướng, không thể xác định chính xác điểm đảo chiều.

- Sự giao nhau của đường trung bình động chậm trễ trong việc nhận diện xu hướng, có thể bỏ lỡ một phần lợi nhuận.

- Có thể giảm rủi ro bằng cách đưa vào các chỉ báo kỹ thuật khác để xác nhận tín hiệu và tối ưu hóa tham số đường trung bình động.

Hướng tối ưu hóa chiến lược

- Cân nhắc đưa vào chỉ báo biến động (volatility) để đánh giá sức mạnh xu hướng, tránh giao dịch trong thị trường dao động.

- Thử nghiệm áp dụng các kỹ thuật định lượng như học máy để tự động tối ưu hóa tham số đường trung bình động.

- Thêm chiến lược cắt lỗ (stop loss) để kịp thời thoát lệnh khi lỗ mở rộng.

- Cân nhắc sử dụng lệnh giới hạn (limit order) khi giao cắt đường trung bình động để giảm trượt giá (slippage).

Kết luận

Chiến lược này kết hợp các đường trung bình động ngắn hạn, trung hạn và dài hạn, dựa vào mối quan hệ giao nhau của chúng để xác định xu hướng thị trường. Đây là một chiến lược theo xu hướng tương đối ổn định và hiệu quả. Bằng cách tối ưu hóa các tham số chỉ báo, cơ chế cắt lỗ và phương thức đặt lệnh, có thể cải thiện thêm tỷ lệ thắng và khả năng sinh lời của chiến lược.

- 1