Chiến lược động lượng đơn giản dựa trên SMA, EMA và khối lượng giao dịch

Tổng quan

Chiến lược này là một chiến lược động lượng trong ngày đơn giản, chỉ thực hiện vị thế mua (không bán khống). Nó sử dụng các chỉ báo SMA, EMA và khối lượng giao dịch để cố gắng tham gia thị trường vào thời điểm tối ưu (khi cả giá và động lượng đều tăng). Ưu điểm của nó là đơn giản trong thực hiện và có khả năng nhận biết xu hướng nhất định.

Nguyên lý chiến lược

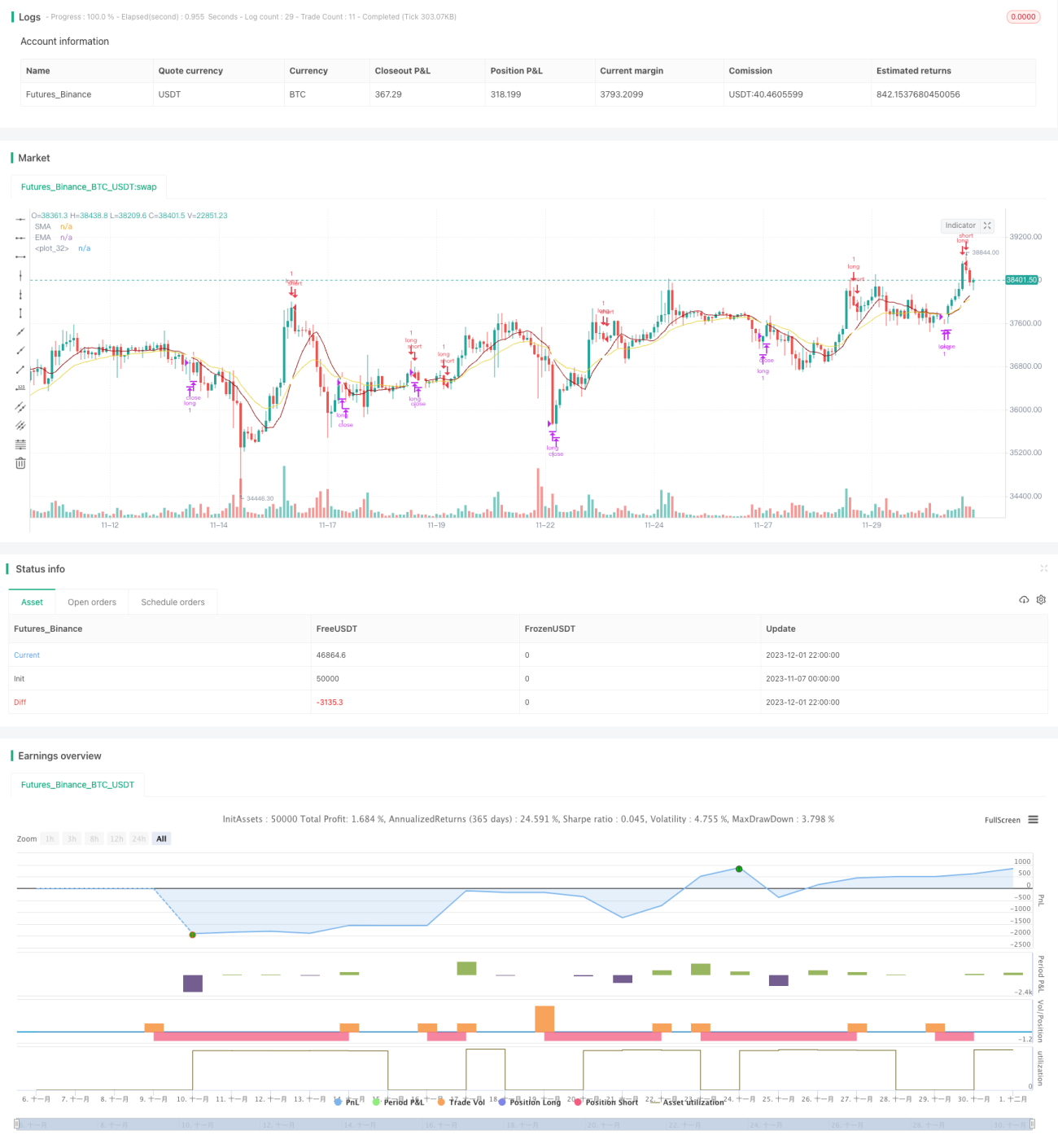

Logic tạo tín hiệu Entry của chiến lược này như sau: Khi đồng thời thỏa mãn chỉ báo SMA cao hơn chỉ báo EMA và 3 nến liên tiếp hoặc 4 nến liên tiếp hình thành xu hướng tăng, cùng với giá thấp nhất của nến ở giữa cao hơn giá mở cửa của nến bắt đầu tăng, thì sẽ phát sinh tín hiệu Entry.

Logic tạo tín hiệu Exit: Khi chỉ báo SMA cắt xuống dưới chỉ báo EMA thì phát sinh tín hiệu Exit.

Chiến lược này chỉ thực hiện vị thế mua, không bán khống. Logic Entry và Exit của nó có khả năng nhận biết nhất định đối với xu hướng tăng liên tục.

Phân tích ưu điểm

Chiến lược này có các ưu điểm sau:

- Logic chiến lược đơn giản, dễ hiểu và dễ thực hiện;

- Sử dụng các chỉ báo kỹ thuật phổ biến như SMA, EMA và khối lượng giao dịch, tham số linh hoạt trong điều chỉnh;

- Có khả năng nhận biết nhất định đối với xu hướng tăng liên tục, có thể nắm bắt một phần cơ hội trong xu hướng.

Phân tích rủi ro

Chiến lược này cũng tồn tại các rủi ro sau:

- Không thể nhận biết thị trường đi ngang hoặc giảm, có thể dẫn đến drawdown lớn;

- Không thể tận dụng cơ hội bán khống, không thể phòng ngừa xu hướng suy thoái, có thể bỏ lỡ cơ hội lợi nhuận tốt;

- Chỉ báo khối lượng giao dịch hoạt động kém hiệu quả với dữ liệu tần suất cao, cần điều chỉnh tham số;

- Có thể sử dụng cắt lỗ để kiểm soát rủi ro.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

- Bổ sung cơ hội giao dịch bán khống, thực hiện giao dịch hai chiều mua bán, tận dụng xu hướng suy thoái để arbitrage;

- Sử dụng các chỉ báo tiên tiến hơn như MACD, RSI để kết hợp chiến lược, nâng cao khả năng phán đoán xu hướng;

- Tối ưu hóa logic cắt lỗ, giảm rủi ro drawdown;

- Điều chỉnh tham số, kiểm tra dữ liệu các chu kỳ khác nhau, tìm bộ tham số tối ưu.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược bám xu hướng rất đơn giản, xác định thời điểm vào lệnh thông qua các chỉ báo SMA, EMA và khối lượng giao dịch. Ưu điểm của nó là đơn giản và dễ thực hiện, phù hợp cho người mới học, nhưng không thể nhận biết xu hướng đi ngang và giảm, tồn tại rủi ro nhất định. Có thể cải thiện bằng cách đưa vào vị thế bán khống, tối ưu hóa chỉ báo và cắt lỗ, v.v.

- 1