Chiến lược theo xu hướng dựa trên kNN

Tổng quan

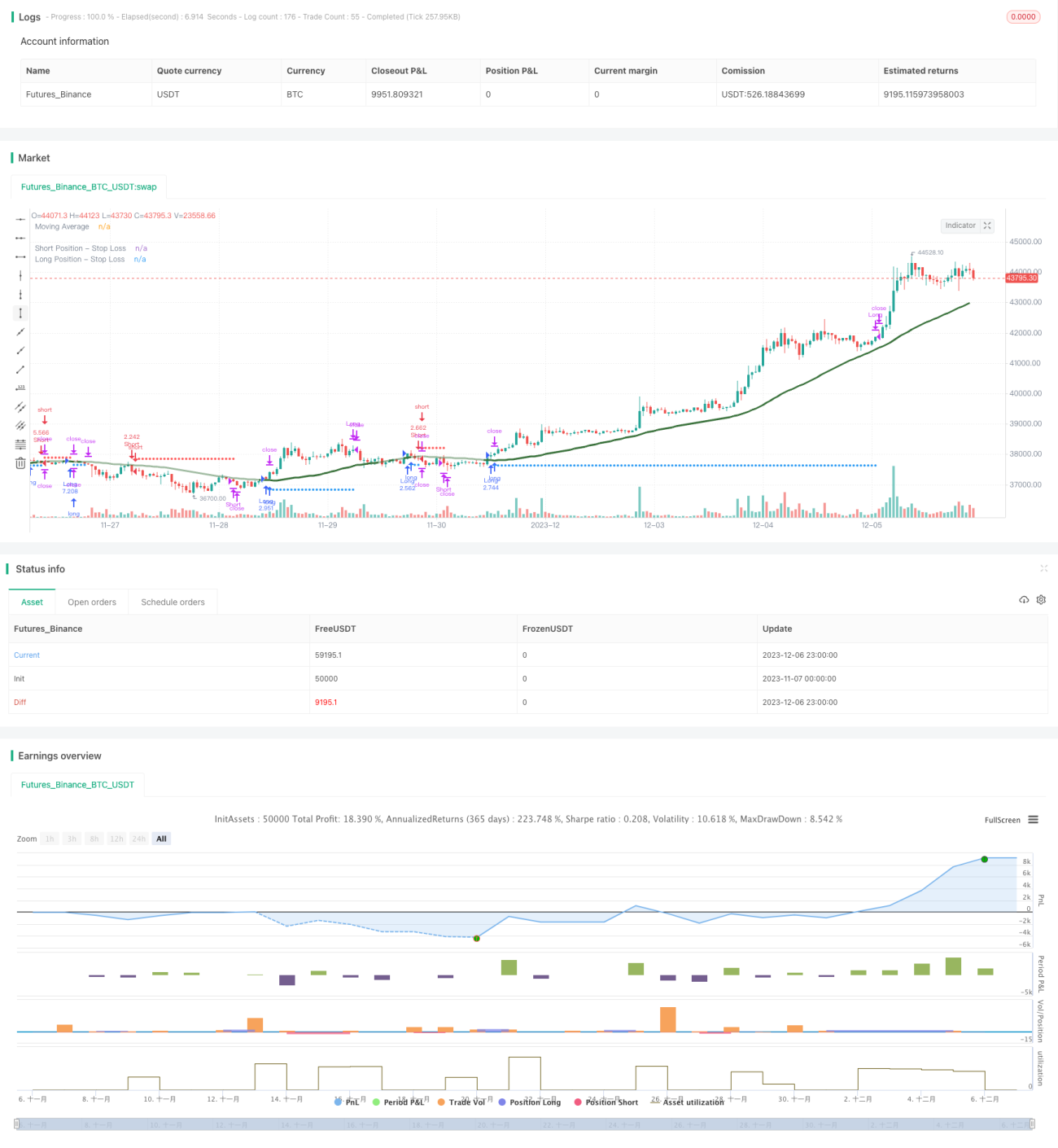

Chiến lược này sử dụng thuật toán học máy k-láng giềng gần nhất (kNN) để dự đoán xu hướng thị trường và tạo ra tín hiệu mua (long) và bán (short) dựa trên kết quả dự đoán. Chiến lược xem xét tổng hợp nhiều yếu tố như dữ liệu lịch sử, chỉ báo kỹ thuật, thông qua việc huấn luyện mô hình kNN để nắm bắt động thái thị trường một cách linh hoạt, thực hiện giao dịch theo xu hướng tự động.

Nguyên lý chiến lược

-

Thu thập dữ liệu huấn luyện: Thu thập chuỗi thời gian giá đóng cửa, khối lượng giao dịch lịch sử, cũng như các chỉ báo kỹ thuật như RSI, CCI.

-

Tiền xử lý dữ liệu: Chuẩn hóa các giá trị chỉ báo về khoảng 0-100.

-

Huấn luyện mô hình kNN: Đưa hai đặc trưng trong mô hình kNN hiện tại, tính khoảng cách Euclid giữa các vector đặc trưng này với các vector đặc trưng lịch sử, chọn k mẫu lịch sử gần nhất, thống kê phân bố nhãn (long hay short) của k mẫu này.

-

Nhận dự đoán: Dựa vào nhãn của k mẫu láng giềng gần nhất để dự đoán xu hướng thị trường hiện tại. Nếu dự đoán là long, tạo tín hiệu mua; nếu dự đoán là short, tạo tín hiệu bán.

-

Kết hợp các bộ lọc như cắt lỗ, kiểm soát vị thế, đường trung bình động để thực hiện giao dịch.

Ưu điểm của chiến lược

-

Sử dụng thuật toán học máy để tự động nhận diện các mô hình kỹ thuật, không cần can thiệp thủ công.

-

Có thể linh hoạt lựa chọn các chỉ báo kỹ thuật khác nhau làm đặc trưng cho mô hình, tối ưu hóa chiến lược theo thời gian thực.

-

Tích hợp các cơ chế quản lý rủi ro chặt chẽ như cắt lỗ, quản lý vị thế.

-

Trực quan hóa đường cắt lỗ, rõ ràng và dễ hiểu.

Rủi ro và giải pháp

-

Dự đoán từ học máy có thể xảy ra sai lệch. Có thể chọn giá trị k, vector đặc trưng, phạm vi thời gian mẫu phù hợp để tối ưu mô hình.

-

Giao dịch một chiều tiềm ẩn rủi ro. Có thể thêm cho phép giao dịch hai chiều trong mã nguồn để loại bỏ lỗi.

-

Thiết lập tham số không phù hợp có thể dẫn đến giao dịch quá mức. Cần điều chỉnh hợp lý quy mô vị thế, tần suất giao dịch và các tham số khác.

Hướng tối ưu hóa

-

Thử nghiệm các loại chỉ báo kỹ thuật khác nhau làm đặc trưng đầu vào cho kNN.

-

Thử nghiệm các phương pháp đo khoảng cách khác như khoảng cách Manhattan.

-

Sử dụng khoảng cách mẫu hoặc chất lượng phân loại để điều chỉnh quy mô vị thế.

-

Thêm phân chia tập huấn luyện, tập kiểm tra cho mô hình, thực hiện tối ưu hóa trượt (rolling optimization).

Tổng kết

Chiến lược này sử dụng thuật toán kNN kinh điển để dự đoán xu hướng thị trường và thực hiện giao dịch theo xu hướng dựa trên tín hiệu dự đoán. Chiến lược có đặc điểm tham số có thể điều chỉnh, rủi ro có thể kiểm soát, cung cấp cho người dùng giải pháp giao dịch tự động hiệu quả. Người dùng có thể cải thiện hiệu suất chiến lược bằng cách điều chỉnh tổ hợp chỉ báo kỹ thuật, tối ưu siêu tham số mô hình, v.v.

- 1