Chiến lược giao dịch định lượng dựa trên chỉ báo TRSI và SUPER trend

Tổng quan

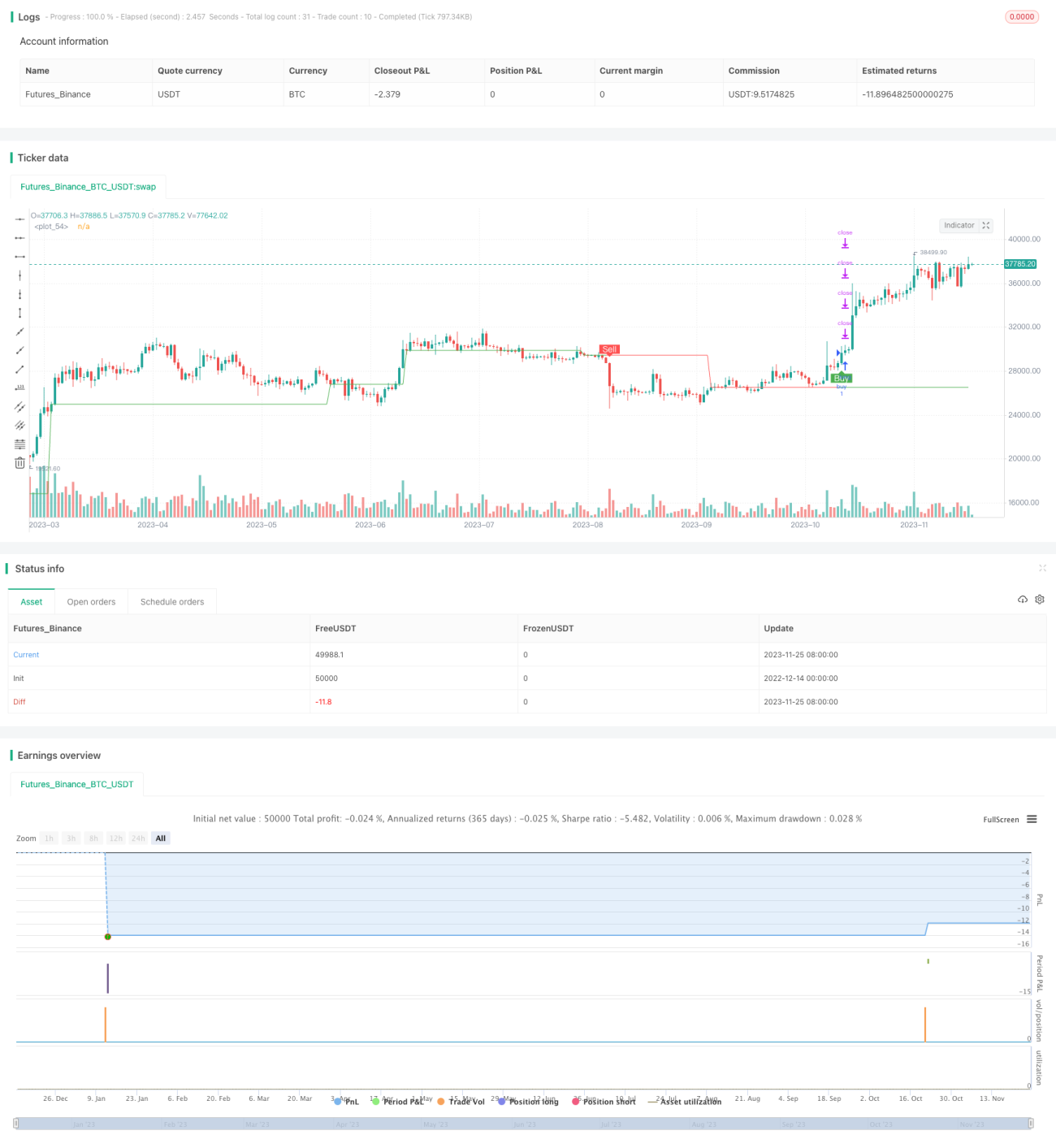

Chiến lược này kết hợp chỉ số sức mạnh tương đối (TRSI) và chỉ số Siêu Xu Hướng (SUPER Trend) để tạo thành một hệ thống giao dịch định lượng khá hoàn chỉnh. Chiến lược chủ yếu được sử dụng để bắt xu hướng trung và dài hạn, đồng thời sử dụng các chỉ báo ngắn hạn để lọc nhiễu tín hiệu giao dịch.

Nguyên lý chiến lược

- Tính toán chỉ số TRSI để đánh giá xem thị trường có đang ở trạng thái quá mua hay quá bán, từ đó đưa ra tín hiệu mua hoặc bán.

- Sử dụng chỉ số SUPER Trend để lọc nhiễu tín hiệu, xác nhận xu hướng cơ bản.

- Thiết lập các điểm dừng lỗ và chốt lời ở các giai đoạn khác nhau trong quá trình có lợi nhuận.

Cụ thể, chiến lược trước tiên tính toán chỉ số TRSI để xác định xem thị trường có xuất hiện vùng quá bán hay không, sau đó tính toán chỉ số SUPER Trend để xác định hướng đi của xu hướng lớn. Kết hợp cả hai để đưa ra tín hiệu giao dịch. Sau đó, thiết lập các điểm dừng lỗ và chốt lời, với tỷ lệ rút vốn khác nhau ở các giai đoạn lợi nhuận khác nhau.

Phân tích ưu điểm

Chiến lược này có những ưu điểm sau:

- Kết hợp nhiều chỉ báo, nâng cao độ chính xác của tín hiệu. TRSI xác định thời điểm, SUPER Trend lọc hướng đi.

- Phù hợp với giao dịch xu hướng trung và dài hạn. Tín hiệu quá mua/quá bán thường dễ tạo ra sự đảo chiều xu hướng.

- Thiết lập dừng lỗ và chốt lời hợp lý, với tỷ lệ rút vốn khác nhau ở các giai đoạn lợi nhuận khác nhau, kiểm soát rủi ro hiệu quả.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro:

- Giao dịch trung và dài hạn, không thể nắm bắt được cơ hội giao dịch ngắn hạn.

- Thông số TRSI cài đặt không phù hợp có thể bỏ lỡ vùng quá mua/quá bán.

- Thông số SUPER Trend cài đặt không phù hợp có thể đưa ra tín hiệu sai.

- Khoảng cách dừng lỗ quá lớn, không thể kiểm soát rủi ro hiệu quả.

Đối với những rủi ro này, chúng ta có thể tối ưu hóa từ các khía cạnh sau:

Hướng tối ưu hóa

- Kết hợp thêm các chỉ báo ngắn hạn để nhận diện nhiều cơ hội giao dịch hơn.

- Điều chỉnh thông số TRSI để thu hẹp khoảng sai số.

- Kiểm tra và tối ưu hóa thông số SUPER Trend.

- Thiết lập dừng lỗ động, theo dõi đường dừng lỗ theo thời gian thực.

Tổng kết

Chiến lược này sử dụng tổng hợp nhiều chỉ báo như TRSI và SUPER Trend, tạo thành một hệ thống giao dịch định lượng khá hoàn chỉnh. Có thể nhận diện hiệu quả xu hướng trung và dài hạn, đồng thời thiết lập dừng lỗ và chốt lời để kiểm soát rủi ro. Không gian tối ưu hóa của chiến lược vẫn còn rất lớn, có thể cải thiện từ việc nâng cao độ chính xác của tín hiệu, nhận diện nhiều cơ hội giao dịch hơn trong tương lai. Nhìn chung, đây là một điểm khởi đầu tốt cho chiến lược định lượng.

/*backtest

start: 2022-12-14 00:00:00

end: 2023-11-26 05:20:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title = "SuperTREX strategy", overlay = true)

strat_dir_input = input(title="Strategy Direction", defval="long", options=["long", "short", "all"])- 1