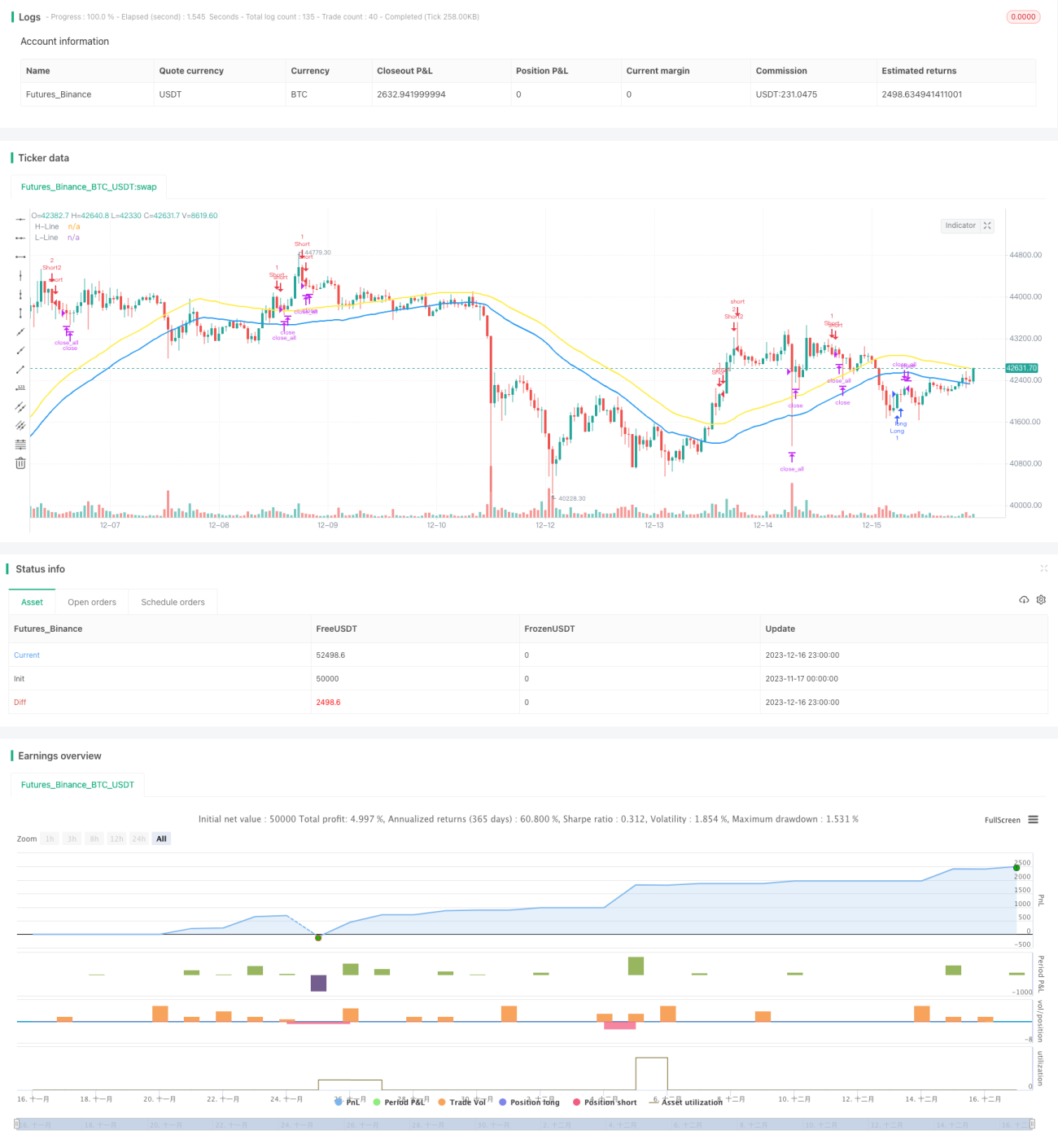

Chiến lược giao dịch theo xu hướng kết hợp Chỉ báo Stochastic cải tiến mod với SMA trên đa khung thời gian

Tổng quan

Chiến lược này sử dụng sự kết hợp cổ điển của chỉ báo Stochastic và SMA, đạt được khả năng bám xu hướng mạnh mẽ. Ý tưởng cốt lõi của chiến lược là sử dụng chỉ báo Stochastic để xác định tín hiệu hướng xu hướng, kết hợp với SMA để lọc và nâng cao chất lượng tín hiệu, sử dụng các chế độ rủi ro khác nhau để thiết lập tham số chỉ báo, thực hiện điều chỉnh động rủi ro và lợi nhuận. Ngoài ra, chiến lược còn sử dụng khung thời gian đa dạng để tối ưu hóa việc lựa chọn thời điểm vào lệnh.

Nguyên lý chiến lược

- Chiến lược sử dụng chỉ báo Stochastic cải tiến mạnh mẽ, với các tham số bao gồm chu kỳ %K, chu kỳ làm mượt %K, chu kỳ làm mượt %D, điều chỉnh độ nhạy của chỉ báo thông qua cài đặt tham số.

- Tham số SMA bao gồm SMA đỉnh cao và SMA đáy thấp, dùng để lọc tín hiệu, nâng cao chất lượng tín hiệu, tránh phá vỡ giả.

- Tùy theo khẩu vị rủi ro, chiến lược cung cấp các chế độ: rủi ro thấp, rủi ro trung bình và rủi ro cao. Chế độ rủi ro ảnh hưởng đến tham số giao cắt của chỉ báo Stochastic, từ đó thực hiện điều chỉnh động rủi ro và lợi nhuận.

- Chiến lược xác định tín hiệu Long khi chỉ báo Stochastic cắt lên trên ngưỡng và giá đóng cửa thấp hơn SMA đáy thấp; xác định tín hiệu Short khi chỉ báo Stochastic cắt xuống dưới ngưỡng và giá đóng cửa cao hơn SMA đỉnh cao.

- Chiến lược giới thiệu mô-đun đánh giá khung thời gian đa dạng, xác thực tín hiệu trong các khung thời gian khác nhau, chọn thời điểm vào lệnh tối ưu hơn nhằm kiểm soát rủi ro giao dịch.

Ưu điểm chiến lược

- Sử dụng chỉ báo Stochastic cải tiến mạnh mẽ, tăng độ nhạy của chỉ báo, có thể nhanh chóng bắt kịp biến động thị trường.

- Thêm cơ chế lọc kép SMA, có thể lọc hiệu quả các tín hiệu giả, nâng cao chất lượng tín hiệu.

- Cung cấp nhiều chế độ rủi ro để lựa chọn, người dùng có thể linh hoạt điều chỉnh tham số theo khẩu vị rủi ro của mình.

- Thêm mô-đun đánh giá khung thời gian đa dạng, tối ưu hóa việc lựa chọn thời điểm vào lệnh, giảm rủi ro giao dịch.

- Cài đặt tham số chiến lược hợp lý, sử dụng chỉ báo tự nhiên, khung tổng thể khoa học và chặt chẽ, độ ổn định tốt, khả năng thích ứng cao.

Rủi ro chiến lược

- Chiến lược tự thân không có cơ chế cắt lỗ, cần thiết lập điểm cắt lỗ thủ công để kiểm soát rủi ro thua lỗ.

- Tín hiệu chiến lược thường xuyên, dễ gây giao dịch quá mức làm tăng chi phí giao dịch.

- Chiến lược nhạy cảm với việc cài đặt tham số và chế độ rủi ro, cần kiểm tra tối ưu để tìm tham số tốt nhất.

- Mức sụt giảm của chiến lược có thể lớn, không thích hợp cho giao dịch toàn bộ vốn, cần kiểm soát quy mô vốn giao dịch.

Phương pháp khắc phục:

- Thiết lập tỷ lệ cắt lỗ hợp lý dựa trên mức độ biến động của thị trường, hạn chế tối đa thua lỗ.

- Điều chỉnh phù hợp tham số chỉ báo Stochastic, giảm tần suất tín hiệu. Hoặc đặt mức chốt lời tối thiểu, giảm các giao dịch không cần thiết.

- Khuyến nghị chọn chế độ rủi ro thấp mặc định, điều chỉnh các tham số khác dựa trên dữ liệu backtest.

- Kiểm soát quy mô vị thế, xây dựng vị thế theo từng đợt, giảm rủi ro cho mỗi giao dịch.

Hướng tối ưu hóa chiến lược

- Tiến hành kiểm tra toàn diện các tham số của chỉ báo Stochastic và SMA để tìm ra tổ hợp tham số tối ưu.

- Tăng số lượng khung thời gian đa dạng, làm phong phú cơ sở đánh giá, tối ưu hóa việc lựa chọn thời điểm vào lệnh.

- Đưa vào tổ hợp chỉ báo cắt lỗ như ATR, có thể theo dõi động điểm cắt lỗ, giảm rủi ro.

- Xây dựng cơ chế lọc và xác nhận tín hiệu chỉ báo, ví dụ thêm chỉ báo khối lượng để đánh giá, tránh bị mắc kẹt.

- Thêm mô-đun quản lý vị thế, chủ động điều chỉnh vị thế dựa trên tình hình thị trường, giảm rủi ro cho mỗi giao dịch.

Tổng kết

Chiến lược này kết hợp toàn diện ưu điểm của chỉ báo Stochastic và SMA, đạt được hiệu quả bám xu hướng mạnh mẽ. Khung chiến lược hợp lý, sử dụng chỉ báo tự nhiên, thông qua kiểm soát tham số và chế độ rủi ro đã khôi phục bản chất của chỉ báo, tối ưu hóa tính ổn định của chiến lược. Mô-đun đánh giá khung thời gian đa dạng cũng nâng cao khả năng thích ứng của chiến lược, có thể điều chỉnh theo các sản phẩm và chu kỳ khác nhau. Nhìn chung, chiến lược này có tính phổ biến tốt, đồng thời cũng có không gian tối ưu hóa lớn, đáng để nghiên cứu sâu hơn sau này.

- 1