Chiến lược trung bình động trơn ngẫu nhiên động lượng

Tổng quan

Chiến lược này kết hợp Đường trung bình động hàm mũ (EMA) với Chỉ báo dao động Stochastic (Stochastic Oscillator), sử dụng phương pháp theo xu hướng và tiếp diễn, đồng thời còn có một số tính năng thú vị. Tôi đã thiết kế chiến lược này đặc biệt cho giao dịch altcoin, nhưng nó cũng áp dụng tốt cho Bitcoin và một số cặp ngoại hối.

Nguyên lý chiến lược

Chiến lược có 4 điều kiện cần thiết để mở tín hiệu giao dịch. Dưới đây là các điều kiện để mở lệnh mua (tín hiệu đóng lệnh ngược lại):

- EMA nhanh cao hơn EMA chậm

- Đường K Stochastic nằm trong vùng quá mua

- Đường K Stochastic cắt lên trên đường D Stochastic

- Giá đóng cửa nằm giữa EMA chậm và EMA nhanh

Khi tất cả các điều kiện đều đúng, lệnh sẽ được mở tại thời điểm mở cửa của nến tiếp theo.

Phân tích ưu điểm

Chiến lược này kết hợp ưu điểm của EMA và Stochastic, giúp bắt đầu và duy trì xu hướng một cách hiệu quả, phù hợp với giao dịch trung và dài hạn. Đồng thời, chiến lược cung cấp nhiều tham số có thể tùy chỉnh, người dùng có thể điều chỉnh theo phong cách giao dịch và đặc điểm thị trường của mình.

Cụ thể, ưu điểm của chiến lược bao gồm:

- EMA giao cắt xác định hướng xu hướng, tăng cường độ ổn định và độ tin cậy của tín hiệu

- Chỉ báo Stochastic xác định vùng quá mua/quá bán, tìm kiếm cơ hội đảo chiều

- Kết hợp hai chỉ báo, vừa theo xu hướng vừa giao dịch ngược xu hướng

- ATR tự động tính toán khoảng cách cắt lỗ, cắt lỗ điều chỉnh theo biến động thị trường

- Có thể tùy chỉnh tỷ lệ lợi nhuận/rủi ro, đáp ứng nhu cầu của nhiều người dùng

- Cung cấp nhiều tham số có thể tùy chỉnh, người dùng có thể điều chỉnh theo thị trường

Phân tích rủi ro

Các rủi ro chính của chiến lược này bao gồm:

- Tín hiệu từ giao cắt EMA có thể bị phá vỡ giả, dẫn đến tín hiệu sai

- Bản thân chỉ báo Stochastic có độ trễ, có thể bỏ lỡ thời điểm tốt nhất của sự đảo chiều giá

- Một chiến lược đơn lẻ không thể hoàn toàn thích ứng với môi trường thị trường đa dạng

Để giảm thiểu các rủi ro trên, có thể áp dụng các biện pháp sau:

- Điều chỉnh tham số chu kỳ EMA phù hợp, tránh tạo ra quá nhiều tín hiệu giả

- Kết hợp thêm nhiều chỉ báo để xác định xu hướng và vùng hỗ trợ, đảm bảo độ tin cậy của tín hiệu giao dịch

- Xây dựng chiến lược quản lý vốn rõ ràng, kiểm soát mức độ rủi ro của mỗi giao dịch

- Sử dụng chiến lược kết hợp, các chiến lược khác nhau có thể xác minh tín hiệu lẫn nhau, tăng độ ổn định

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa thêm từ các khía cạnh sau:

- Thêm mô-đun điều chỉnh vị thế dựa trên biến động. Khi thị trường biến động mạnh, giảm quy mô vị thế phù hợp; khi biến động yếu, có thể tăng quy mô vị thế.

- Thêm đánh giá xu hướng cấp độ lớn, tránh giao dịch ngược xu hướng. Ví dụ, kết hợp nến hàng ngày hoặc hàng tuần để xác định hướng xu hướng.

- Thêm mô hình học máy để xác định tín hiệu mua bán. Có thể huấn luyện mô hình phân loại dựa trên dữ liệu lịch sử để hỗ trợ tạo tín hiệu giao dịch.

- Tối ưu hóa mô-đun chiến lược quản lý vốn, làm cho cắt lỗ và quy mô vị thế thông minh hơn.

Kết luận

Chiến lược này tích hợp ưu điểm của giao dịch theo xu hướng và giao dịch đảo chiều, vừa xem xét môi trường thị trường cấp độ lớn, vừa chú ý đến hành vi giá hiện tại. Đây là một chiến lược hiệu quả đáng để theo dõi giao dịch thực tế dài hạn. Bằng cách liên tục tối ưu hóa cài đặt tham số, thêm các mô-đun đánh giá xu hướng, hiệu suất của chiến lược vẫn còn nhiều dư địa cải thiện, xứng đáng đầu tư thêm nỗ lực nghiên cứu và phát triển.

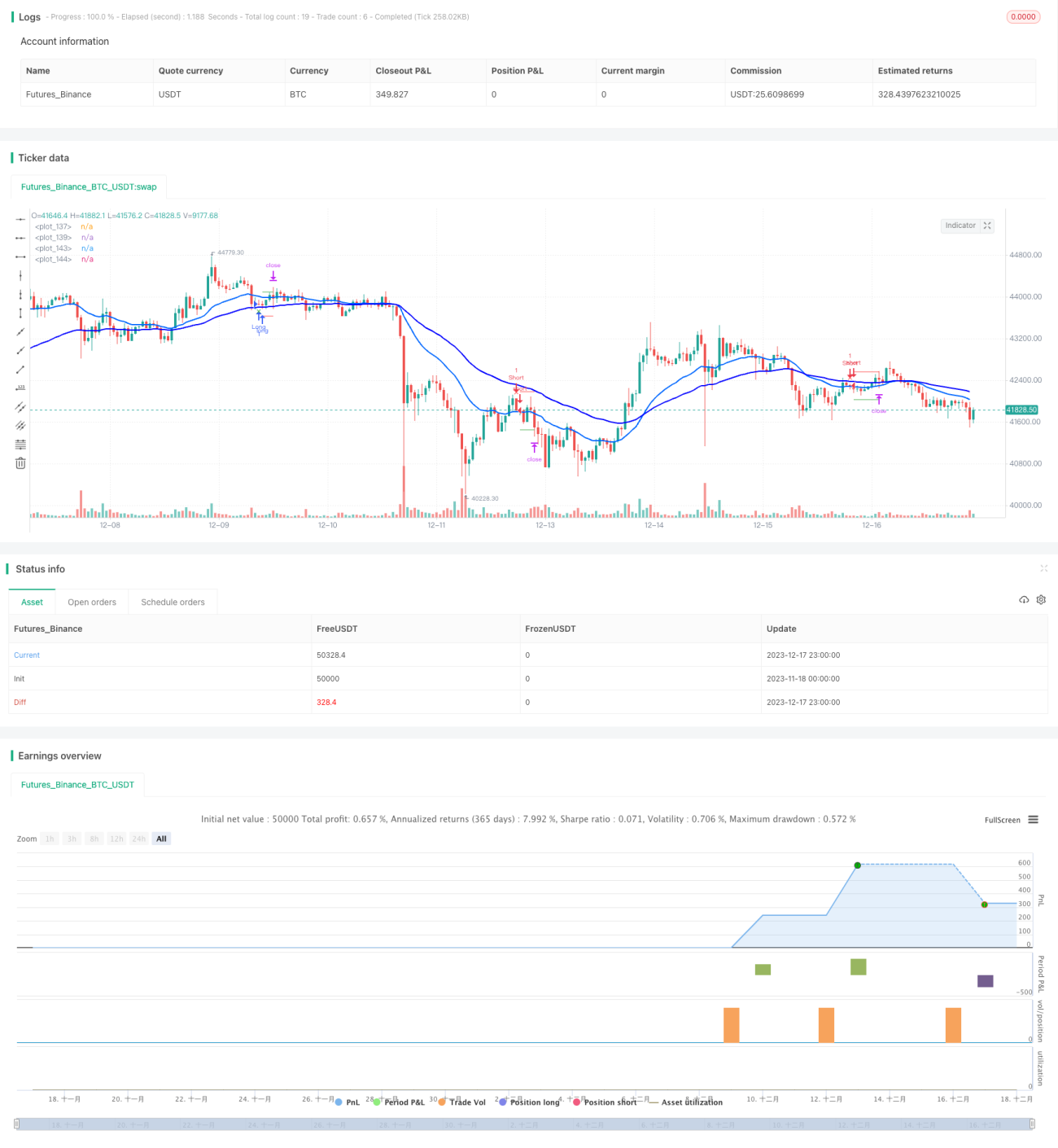

/*backtest

start: 2023-11-18 00:00:00

end: 2023-12-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LucasVivien

// Since this Strategy may have its stop loss hit within the opening candle, consider turning on 'Recalculate : After Order is filled' in the strategy settings, in the "Properties" tabs- 1