Chiến lược giao dịch điều chỉnh RSI khi Bollinger Bands cắt xuống

Tổng quan

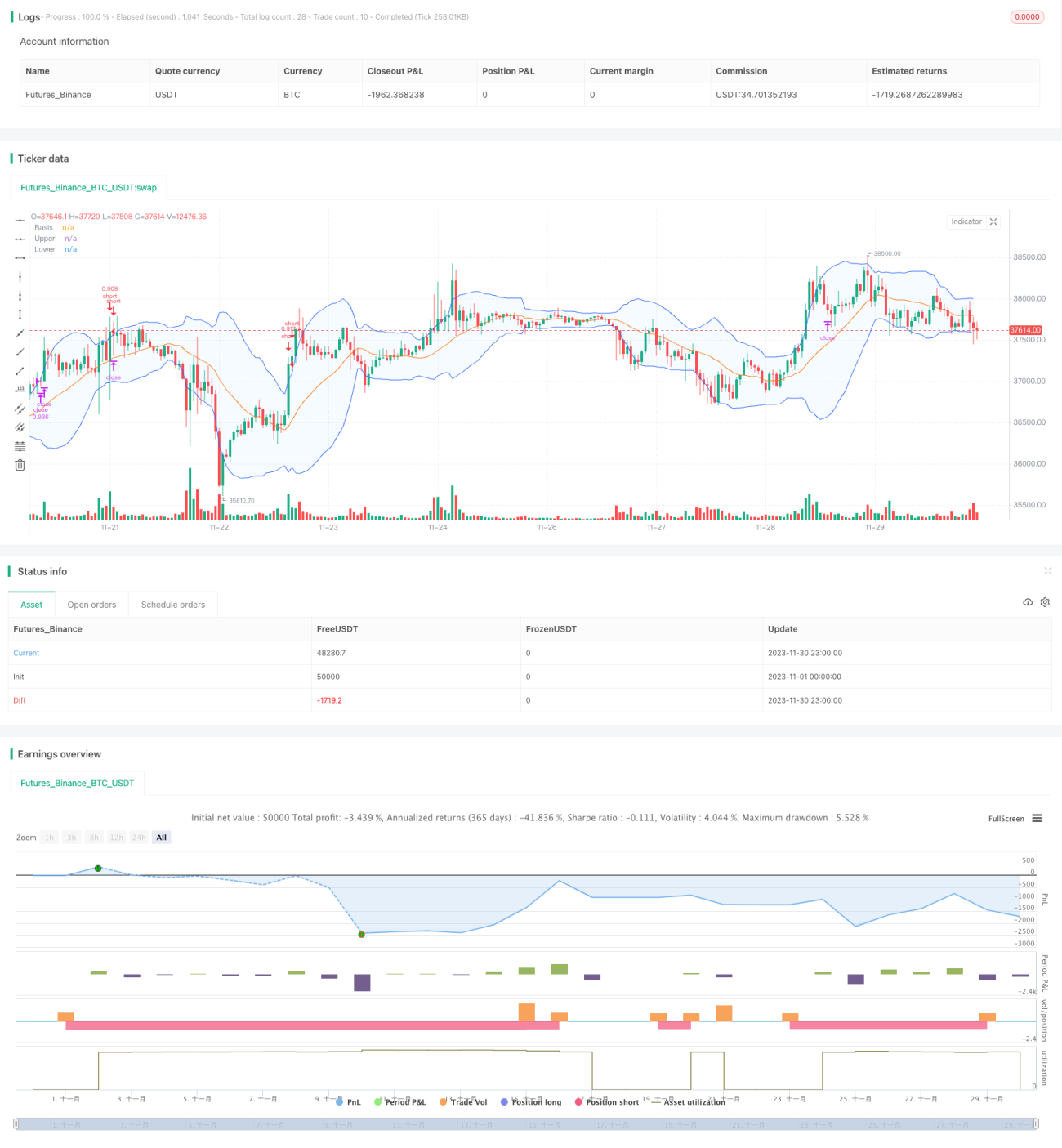

Chiến lược này sử dụng chỉ báo Bollinger Bands để xác định xem giá có đang ở vùng quá mua/quá bán hay không, kết hợp với chỉ báo RSI để xác định cơ hội điều chỉnh, bán khống khi hình thành giao cắt tử thần trong vùng quá mua, và cắt lỗ khi giá tăng vượt dải trên của Bollinger Bands.

Nguyên lý chiến lược

Chiến lược này chủ yếu dựa trên các nguyên lý sau:

- Khi giá đóng cửa vượt lên trên dải trên của Bollinger Bands, tài sản đang ở vùng quá mua, tồn tại cơ hội điều chỉnh.

- Chỉ báo RSI có thể xác định hiệu quả vùng quá mua/quá bán, RSI > 70 là vùng quá mua.

- Khi giá đóng cửa đi xuống dưới dải trên, mở vị thế bán khống.

- Khi RSI thoát khỏi vùng quá mua hoặc điểm dừng lỗ bị kích hoạt, đóng vị thế cắt lỗ.

Phân tích ưu điểm

Chiến lược này có các ưu điểm sau:

- Sử dụng Bollinger Bands để xác định vùng quá mua/quá bán, nâng cao tỷ lệ thành công của các giao dịch.

- Kết hợp chỉ báo RSI để lọc các tín hiệu phá vỡ giả, tránh các tổn thất không cần thiết.

- Tỷ lệ lợi nhuận/rủi ro cao, kiểm soát rủi ro ở mức tối đa.

Phân tích rủi ro

Chiến lược này tồn tại các rủi ro sau:

- Sau khi phá vỡ dải trên, giá tiếp tục tăng dẫn đến tổn thất mở rộng thêm.

- RSI không kịp thời giảm, tổn thất tiếp tục mở rộng.

- Nắm giữ một chiều, không thể giao dịch trong thị trường đi ngang.

Có thể giảm thiểu rủi ro bằng các phương pháp sau:

- Điều chỉnh điểm dừng lỗ phù hợp, kịp thời cắt lỗ.

- Kết hợp các chỉ báo khác để xác định tín hiệu giảm của RSI.

- Kết hợp chỉ báo đường trung bình động để xác định xem có đang trong giai đoạn đi ngang hay không.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

- Tối ưu hóa tham số Bollinger Bands để phù hợp với nhiều loại tài sản giao dịch hơn.

- Tối ưu hóa tham số RSI để nâng cao hiệu quả của chỉ báo.

- Thêm kết hợp các chỉ báo khác để xác định điểm đảo chiều xu hướng.

- Bổ sung logic giao dịch vị thế mua.

- Kết hợp chiến lược dừng lỗ, điều chỉnh điểm dừng lỗ một cách linh hoạt.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược giao dịch ngắn hạn nhanh điển hình trong vùng quá mua. Sử dụng Bollinger Bands để xác định điểm mua bán, RSI để lọc tín hiệu. Kiểm soát mức rủi ro thông qua việc dừng lỗ hợp lý. Có thể nâng cao hiệu quả thông qua tối ưu hóa tham số, kết hợp chỉ báo, tăng thêm logic mở vị thế, v.v.

- 1