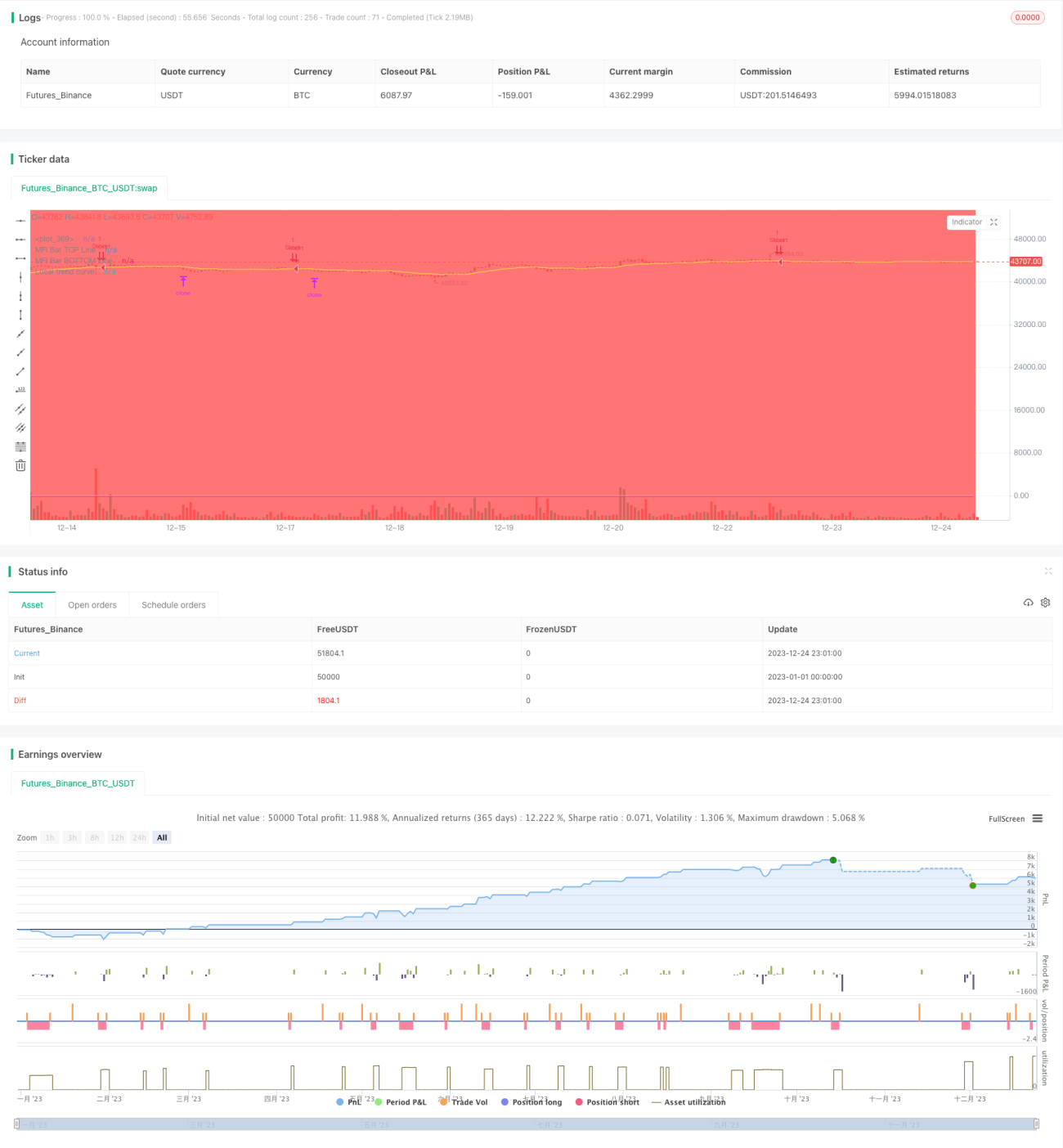

Chiến lược giao dịch định lượng dựa trên bộ lọc xu hướng kép

Tổng quan

Đây là một chiến lược giao dịch định lượng sử dụng bộ lọc xu hướng kép. Chiến lược này kết hợp đồng thời bộ lọc xu hướng toàn cục và bộ lọc xu hướng cục bộ, đảm bảo chỉ mở lệnh khi hướng xu hướng chính xác. Ngoài ra, chiến lược còn thiết lập nhiều điều kiện lọc khác như bộ lọc RSI, bộ lọc giá, bộ lọc độ dốc, v.v., nhằm nâng cao hơn nữa độ tin cậy của tín hiệu giao dịch. Về mặt thoát lệnh, chiến lược đã cài đặt sẵn các mức dừng lỗ và chốt lời. Nhìn chung, đây là một chiến lược giao dịch định lượng ổn định và chính xác.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược này dựa trên bộ lọc xu hướng kép. Bộ lọc xu hướng toàn cục dựa trên EMA chu kỳ cao để xác định xu hướng tổng thể của thị trường, bộ lọc xu hướng cục bộ dựa trên EMA chu kỳ thấp để xác định xu hướng cục bộ. Chỉ khi cả hai xác định xu hướng đồng nhất thì mới mở lệnh.

Cụ thể, chiến lược tính toán đường EMA của BTCUSDT để xác định thị trường tổng thể đang ở xu hướng tăng hay giảm, đó là bộ lọc xu hướng toàn cục. Đồng thời, chiến lược tính toán đường EMA của hợp đồng hiện tại để xác định xu hướng thị trường cục bộ, đó là bộ lọc xu hướng cục bộ. Khi cả hai xác định xu hướng đồng nhất, kết hợp với nhiều bộ lọc phụ trợ khác, chiến lược sẽ tạo ra tín hiệu giao dịch và cài đặt sẵn giá chốt lời/dừng lỗ để mở lệnh.

Sau khi xác định tín hiệu giao dịch, chiến lược sẽ ngay lập tức đặt lệnh mở vị thế. Đồng thời, chiến lược cài đặt sẵn giá chốt lời và giá dừng lỗ. Khi giá chạm đến mức chốt lời hoặc dừng lỗ, chiến lược sẽ tự động chốt lời hoặc dừng lỗ.

Phân tích ưu điểm

Đây là một chiến lược giao dịch định lượng ổn định và đáng tin cậy, với những ưu điểm chính:

-

Sử dụng cơ chế lọc xu hướng kép, có thể lọc bỏ hầu hết các tín hiệu giả, làm cho tín hiệu giao dịch đáng tin cậy và chính xác hơn.

-

Kết hợp nhiều bộ lọc phụ trợ, như bộ lọc RSI, bộ lọc giá, v.v., giúp nâng cao hơn nữa chất lượng tín hiệu.

-

Tự động tính toán mức chốt lời và dừng lỗ, không cần giám sát thủ công, giảm rủi ro giao dịch.

-

Các tham số chiến lược có thể tùy chỉnh, thích ứng với nhiều loại sản phẩm giao dịch, có tính thích ứng cao.

-

Tư duy chiến lược rõ ràng, dễ hiểu, thuận tiện cho việc tối ưu hóa và cải tiến, có không gian mở rộng lớn.

Phân tích rủi ro

Mặc dù chiến lược này có nhiều ưu điểm, nhưng vẫn tồn tại một số rủi ro giao dịch nhất định, tập trung chủ yếu vào:

-

Bộ lọc xu hướng kép xác định thời điểm vào lệnh không chính xác. Có thể tối ưu bằng cách điều chỉnh tham số bộ lọc.

-

Cài đặt giá chốt lời/dừng lỗ không chính xác, có thể dẫn đến chốt lời hoặc dừng lỗ quá sớm. Có thể thử nghiệm các tổ hợp tham số khác nhau để tìm giải pháp tối ưu.

-

Lựa chọn sản phẩm giao dịch và khung thời gian không phù hợp có thể khiến chiến lược không hiệu quả. Khuyến nghị tiến hành tối ưu hóa và kiểm tra tham số riêng cho từng sản phẩm.

-

Có rủi ro quá khớp nhất định. Cần backtest trong nhiều môi trường thị trường hơn để đảm bảo tính ổn định của chiến lược.

Hướng tối ưu hóa

Chiến lược này chủ yếu có thể được tối ưu hóa theo các hướng sau:

-

Điều chỉnh tham số của bộ lọc kép để tìm tổ hợp tham số tối ưu;

-

Thử nghiệm và lựa chọn bộ lọc phụ trợ tốt nhất;

-

Tối ưu hóa thuật toán chốt lời/dừng lỗ để trở nên thông minh hơn;

-

Thử nghiệm đưa vào các phương pháp như học máy để thực hiện điều chỉnh tham số động của chiến lược;

-

Backtest trên nhiều sản phẩm giao dịch hơn và trong khung thời gian dài hơn để nâng cao tính ổn định của chiến lược.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược giao dịch định lượng ổn định, chính xác và dễ tối ưu hóa. Nó sử dụng bộ lọc xu hướng kép kết hợp nhiều bộ lọc phụ trợ để tạo ra tín hiệu giao dịch, có thể lọc bỏ hầu hết nhiễu, giúp tín hiệu chính xác và đáng tin cậy hơn. Đồng thời, chiến lược tích hợp sẵn thiết lập chốt lời/dừng lỗ, có thể giảm rủi ro giao dịch. Đây là một chiến lược có giá trị thực chiến cao, sau khi tối ưu hóa và xác minh, có thể đưa vào sử dụng trực tiếp trong giao dịch thực tế. Nó cũng có tiềm năng mở rộng rất lớn, là một chiến lược định lượng đáng để nghiên cứu sâu.

- 1